From Exuberant Youth to Sustainable Maturity - DTI Home

From Exuberant Youth to Sustainable Maturity - DTI Home

From Exuberant Youth to Sustainable Maturity - DTI Home

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

DETAILED UK SUB-SECTOR REVIEW<br />

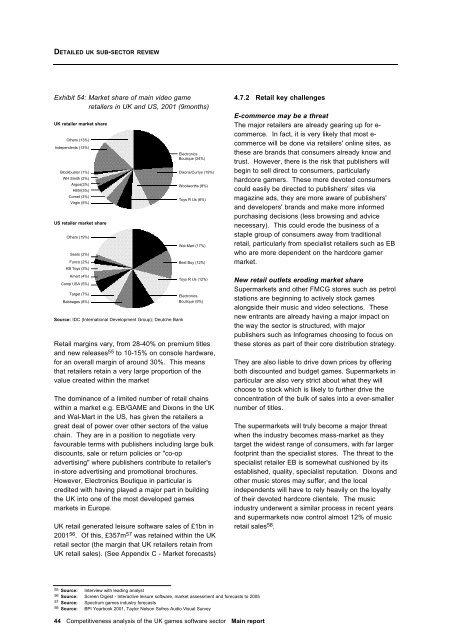

Exhibit 54: Market share of main video game<br />

retailers in UK and US, 2001 (9months)<br />

UK retailer market share<br />

Others (13%)<br />

Independents (13%)<br />

Blockbuster (1%)<br />

WH Smith (2%)<br />

Argos(3%)<br />

HMV(3%)<br />

Comet (3%)<br />

Virgin (5%)<br />

US retailer market share<br />

Others (19%)<br />

Sears (2%)<br />

Funco (2%)<br />

KB Toys (3%)<br />

Kmart (4%)<br />

Comp USA (5%)<br />

Target (7%)<br />

Babbages (8%)<br />

Source: IDC (International Development Group); Deutche Bank<br />

Electronics<br />

Boutique (24%)<br />

Dixons/Currys (19%)<br />

Woolworths (8%)<br />

Toys R Us (6%)<br />

Wal-Mart (17%)<br />

Best Buy (12%)<br />

Toys R Us (12%)<br />

Electronics<br />

Boutique (9%)<br />

Retail margins vary, from 28-40% on premium titles<br />

and new releases 55 <strong>to</strong> 10-15% on console hardware,<br />

for an overall margin of around 30%. This means<br />

that retailers retain a very large proportion of the<br />

value created within the market<br />

The dominance of a limited number of retail chains<br />

within a market e.g. EB/GAME and Dixons in the UK<br />

and Wal-Mart in the US, has given the retailers a<br />

great deal of power over other sec<strong>to</strong>rs of the value<br />

chain. They are in a position <strong>to</strong> negotiate very<br />

favourable terms with publishers including large bulk<br />

discounts, sale or return policies or "co-op<br />

advertising" where publishers contribute <strong>to</strong> retailer's<br />

in-s<strong>to</strong>re advertising and promotional brochures.<br />

However, Electronics Boutique in particular is<br />

credited with having played a major part in building<br />

the UK in<strong>to</strong> one of the most developed games<br />

markets in Europe.<br />

UK retail generated leisure software sales of £1bn in<br />

2001 56 . Of this, £357m 57 was retained within the UK<br />

retail sec<strong>to</strong>r (the margin that UK retailers retain from<br />

UK retail sales). (See Appendix C - Market forecasts)<br />

55 Source: Interview with leading analyst<br />

56 Source: Screen Digest - Interactive leisure software, market assessment and forecasts <strong>to</strong> 2005<br />

57 Source: Spectrum games industry forecasts<br />

58 Source: BPI Yearbook 2001, Taylor Nelson Sofres Audio Visual Survey<br />

44 Competitiveness analysis of the UK games software sec<strong>to</strong>r Main report<br />

4.7.2 Retail key challenges<br />

E-commerce may be a threat<br />

The major retailers are already gearing up for ecommerce.<br />

In fact, it is very likely that most ecommerce<br />

will be done via retailers' online sites, as<br />

these are brands that consumers already know and<br />

trust. However, there is the risk that publishers will<br />

begin <strong>to</strong> sell direct <strong>to</strong> consumers, particularly<br />

hardcore gamers. These more devoted consumers<br />

could easily be directed <strong>to</strong> publishers' sites via<br />

magazine ads, they are more aware of publishers'<br />

and developers' brands and make more informed<br />

purchasing decisions (less browsing and advice<br />

necessary). This could erode the business of a<br />

staple group of consumers away from traditional<br />

retail, particularly from specialist retailers such as EB<br />

who are more dependent on the hardcore gamer<br />

market.<br />

New retail outlets eroding market share<br />

Supermarkets and other FMCG s<strong>to</strong>res such as petrol<br />

stations are beginning <strong>to</strong> actively s<strong>to</strong>ck games<br />

alongside their music and video selections. These<br />

new entrants are already having a major impact on<br />

the way the sec<strong>to</strong>r is structured, with major<br />

publishers such as Infogrames choosing <strong>to</strong> focus on<br />

these s<strong>to</strong>res as part of their core distribution strategy.<br />

They are also liable <strong>to</strong> drive down prices by offering<br />

both discounted and budget games. Supermarkets in<br />

particular are also very strict about what they will<br />

choose <strong>to</strong> s<strong>to</strong>ck which is likely <strong>to</strong> further drive the<br />

concentration of the bulk of sales in<strong>to</strong> a ever-smaller<br />

number of titles.<br />

The supermarkets will truly become a major threat<br />

when the industry becomes mass-market as they<br />

target the widest range of consumers, with far larger<br />

footprint than the specialist s<strong>to</strong>res. The threat <strong>to</strong> the<br />

specialist retailer EB is somewhat cushioned by its<br />

established, quality, specialist reputation. Dixons and<br />

other music s<strong>to</strong>res may suffer, and the local<br />

independents will have <strong>to</strong> rely heavily on the loyalty<br />

of their devoted hardcore clientele. The music<br />

industry underwent a similar process in recent years<br />

and supermarkets now control almost 12% of music<br />

retail sales 58 .