European Court of Justice VAT cases 2006-3 - empcom.gov.in

European Court of Justice VAT cases 2006-3 - empcom.gov.in

European Court of Justice VAT cases 2006-3 - empcom.gov.in

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

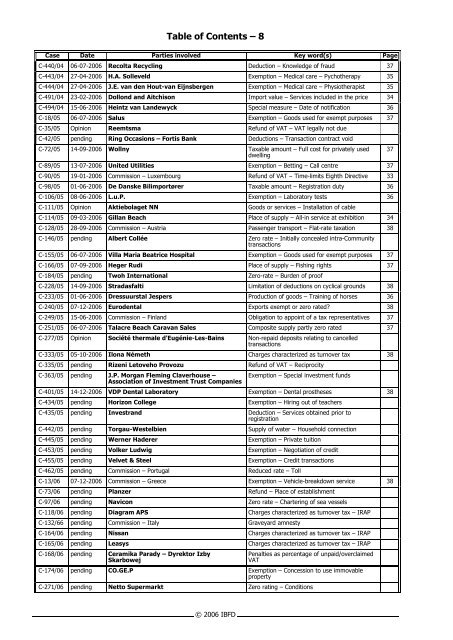

Table <strong>of</strong> Contents – 8<br />

Case Date Parties <strong>in</strong>volved Key word(s) Page<br />

C-440/04 06-07-<strong>2006</strong> Recolta Recycl<strong>in</strong>g Deduction – Knowledge <strong>of</strong> fraud 37<br />

C-443/04 27-04-<strong>2006</strong> H.A. Solleveld Exemption – Medical care – Pychotherapy 35<br />

C-444/04 27-04-<strong>2006</strong> J.E. van den Hout-van Eijnsbergen Exemption – Medical care – Physiotherapist 35<br />

C-491/04 23-02-<strong>2006</strong> Dollond and Aitchison Import value – Services <strong>in</strong>cluded <strong>in</strong> the price 34<br />

C-494/04 15-06-<strong>2006</strong> He<strong>in</strong>tz van Landewyck Special measure – Date <strong>of</strong> notification 36<br />

C-18/05 06-07-<strong>2006</strong> Salus Exemption – Goods used for exempt purposes 37<br />

C-35/05 Op<strong>in</strong>ion Reemtsma Refund <strong>of</strong> <strong>VAT</strong> – <strong>VAT</strong> legally not due<br />

C-42/05 pend<strong>in</strong>g R<strong>in</strong>g Occasions – Fortis Bank Deductions – Transaction contract void<br />

C-72/05 14-09-<strong>2006</strong> Wollny Taxable amount – Full cost for privately used<br />

dwell<strong>in</strong>g<br />

C-89/05 13-07-<strong>2006</strong> United Utilities Exemption – Bett<strong>in</strong>g – Call centre 37<br />

C-90/05 19-01-<strong>2006</strong> Commission – Luxembourg Refund <strong>of</strong> <strong>VAT</strong> S Time-limits Eighth Directive 33<br />

C-98/05 01-06-<strong>2006</strong> De Danske Bilimportører Taxable amount – Registration duty 36<br />

C-106/05 08-06-<strong>2006</strong> L.u.P. Exemption – Laboratory tests 36<br />

C-111/05 Op<strong>in</strong>ion Aktiebolaget NN Goods or services – Installation <strong>of</strong> cable<br />

C-114/05 09-03-<strong>2006</strong> Gillan Beach Place <strong>of</strong> supply – All-<strong>in</strong> service at exhibition 34<br />

C-128/05 28-09-<strong>2006</strong> Commission – Austria Passenger transport – Flat-rate taxation 38<br />

C-146/05 pend<strong>in</strong>g Albert Collée Zero rate – Initially concealed <strong>in</strong>tra-Community<br />

transactions<br />

C-155/05 06-07-<strong>2006</strong> Villa Maria Beatrice Hospital Exemption – Goods used for exempt purposes 37<br />

C-166/05 07-09-<strong>2006</strong> Heger Rudi Place <strong>of</strong> supply – Fish<strong>in</strong>g rights 37<br />

C-184/05 pend<strong>in</strong>g Twoh International Zero-rate – Burden <strong>of</strong> pro<strong>of</strong><br />

C-228/05 14-09-<strong>2006</strong> Stradasfalti Limitation <strong>of</strong> deductions on cyclical grounds 38<br />

C-233/05 01-06-<strong>2006</strong> Dressuurstal Jespers Production <strong>of</strong> goods – Tra<strong>in</strong><strong>in</strong>g <strong>of</strong> horses 36<br />

C-240/05 07-12-<strong>2006</strong> Eurodental Exports exempt or zero rated? 38<br />

C-249/05 15-06-<strong>2006</strong> Commission – F<strong>in</strong>land Obligation to appo<strong>in</strong>t <strong>of</strong> a tax representatives 37<br />

C-251/05 06-07-<strong>2006</strong> Talacre Beach Caravan Sales Composite supply partly zero rated 37<br />

C-277/05 Op<strong>in</strong>ion Société thermale d'Eugénie-Les-Ba<strong>in</strong>s Non-repaid deposits relat<strong>in</strong>g to cancelled<br />

transactions<br />

C-333/05 05-10-<strong>2006</strong> Ilona Németh Charges characterized as turnover tax 38<br />

C-335/05 pend<strong>in</strong>g Rizeni Letoveho Provozu Refund <strong>of</strong> <strong>VAT</strong> – Reciprocity<br />

C-363/05 pend<strong>in</strong>g J.P. Morgan Flem<strong>in</strong>g Claverhouse –<br />

Association <strong>of</strong> Investment Trust Companies<br />

© <strong>2006</strong> IBFD<br />

Exemption – Special <strong>in</strong>vestment funds<br />

C-401/05 14-12-<strong>2006</strong> VDP Dental Laboratory Exemption – Dental prostheses 38<br />

C-434/05 pend<strong>in</strong>g Horizon College Exemption – Hir<strong>in</strong>g out <strong>of</strong> teachers<br />

C-435/05 pend<strong>in</strong>g Investrand Deduction – Services obta<strong>in</strong>ed prior to<br />

registration<br />

C-442/05 pend<strong>in</strong>g Torgau-Westelbien Supply <strong>of</strong> water – Household connection<br />

C-445/05 pend<strong>in</strong>g Werner Haderer Exemption – Private tuition<br />

C-453/05 pend<strong>in</strong>g Volker Ludwig Exemption – Negotiation <strong>of</strong> credit<br />

C-455/05 pend<strong>in</strong>g Velvet & Steel Exemption – Credit transactions<br />

C-462/05 pend<strong>in</strong>g Commission – Portugal Reduced rate – Toll<br />

C-13/06 07-12-<strong>2006</strong> Commission – Greece Exemption – Vehicle-breakdown service 38<br />

C-73/06 pend<strong>in</strong>g Planzer Refund – Place <strong>of</strong> establishment<br />

C-97/06 pend<strong>in</strong>g Navicon Zero rate – Charter<strong>in</strong>g <strong>of</strong> sea vessels<br />

C-118/06 pend<strong>in</strong>g Diagram APS Charges characterized as turnover tax – IRAP<br />

C-132/66 pend<strong>in</strong>g Commission – Italy Graveyard amnesty<br />

C-164/06 pend<strong>in</strong>g Nissan Charges characterized as turnover tax – IRAP<br />

C-165/06 pend<strong>in</strong>g Leasys Charges characterized as turnover tax – IRAP<br />

C-168/06 pend<strong>in</strong>g Ceramika Parady – Dyrektor Izby<br />

Skarbowej<br />

Penalties as percentage <strong>of</strong> unpaid/overclaimed<br />

<strong>VAT</strong><br />

C-174/06 pend<strong>in</strong>g CO.GE.P Exemption – Concession to use immovable<br />

property<br />

C-271/06 pend<strong>in</strong>g Netto Supermarkt Zero rat<strong>in</strong>g – Conditions<br />

37