Stock Valuation

Stock Valuation

Stock Valuation

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

284 PART 2 Important Financial Concepts<br />

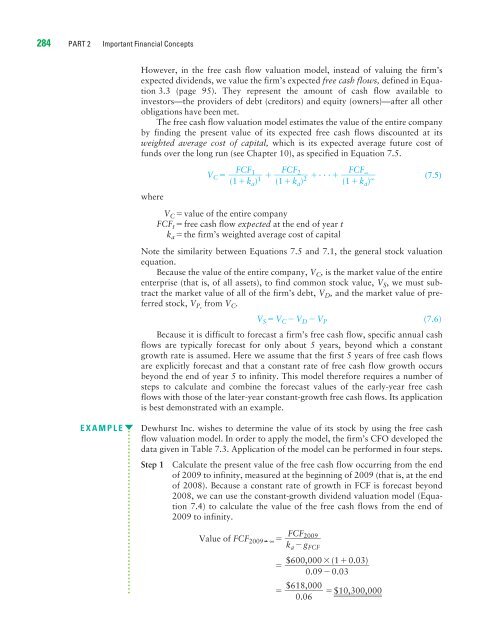

However, in the free cash flow valuation model, instead of valuing the firm’s<br />

expected dividends, we value the firm’s expected free cash flows, defined in Equation<br />

3.3 (page 95). They represent the amount of cash flow available to<br />

investors—the providers of debt (creditors) and equity (owners)—after all other<br />

obligations have been met.<br />

The free cash flow valuation model estimates the value of the entire company<br />

by finding the present value of its expected free cash flows discounted at its<br />

weighted average cost of capital, which is its expected average future cost of<br />

funds over the long run (see Chapter 10), as specified in Equation 7.5.<br />

VC . . . FCF∞ (7.5)<br />

(1 ka) ∞<br />

FCF2 <br />

(1 ka) 2<br />

FCF1 <br />

(1 ka) 1<br />

where<br />

V Cvalue of the entire company<br />

FCF tfree cash flow expected at the end of year t<br />

k athe firm’s weighted average cost of capital<br />

Note the similarity between Equations 7.5 and 7.1, the general stock valuation<br />

equation.<br />

Because the value of the entire company, VC, is the market value of the entire<br />

enterprise (that is, of all assets), to find common stock value, VS, we must subtract<br />

the market value of all of the firm’s debt, VD, and the market value of preferred<br />

stock, VP, from VC. VSV CV DV P<br />

(7.6)<br />

Because it is difficult to forecast a firm’s free cash flow, specific annual cash<br />

flows are typically forecast for only about 5 years, beyond which a constant<br />

growth rate is assumed. Here we assume that the first 5 years of free cash flows<br />

are explicitly forecast and that a constant rate of free cash flow growth occurs<br />

beyond the end of year 5 to infinity. This model therefore requires a number of<br />

steps to calculate and combine the forecast values of the early-year free cash<br />

flows with those of the later-year constant-growth free cash flows. Its application<br />

is best demonstrated with an example.<br />

EXAMPLE Dewhurst Inc. wishes to determine the value of its stock by using the free cash<br />

flow valuation model. In order to apply the model, the firm’s CFO developed the<br />

data given in Table 7.3. Application of the model can be performed in four steps.<br />

Step 1 Calculate the present value of the free cash flow occurring from the end<br />

of 2009 to infinity, measured at the beginning of 2009 (that is, at the end<br />

of 2008). Because a constant rate of growth in FCF is forecast beyond<br />

2008, we can use the constant-growth dividend valuation model (Equation<br />

7.4) to calculate the value of the free cash flows from the end of<br />

2009 to infinity.<br />

Value of FCF2009 ∞<br />

<br />

$<br />

1 0 , 3 0 0 , 0 0 0 FCF2009 <br />

kag FCF<br />

$600,000(1 0.03)<br />

<br />

0.09 0.03<br />

$618,000<br />

<br />

0.06