OES Annual Report 2012 - Ocean Energy Systems

OES Annual Report 2012 - Ocean Energy Systems

OES Annual Report 2012 - Ocean Energy Systems

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

128<br />

WAVE<br />

TIDAL<br />

Operations &<br />

maintenance<br />

Operations &<br />

maintenance<br />

Structure<br />

Structure<br />

Grid<br />

connection<br />

Station keeping<br />

Grid<br />

connection<br />

Station keeping<br />

Power take-off<br />

Installation<br />

Power take-off<br />

Installation<br />

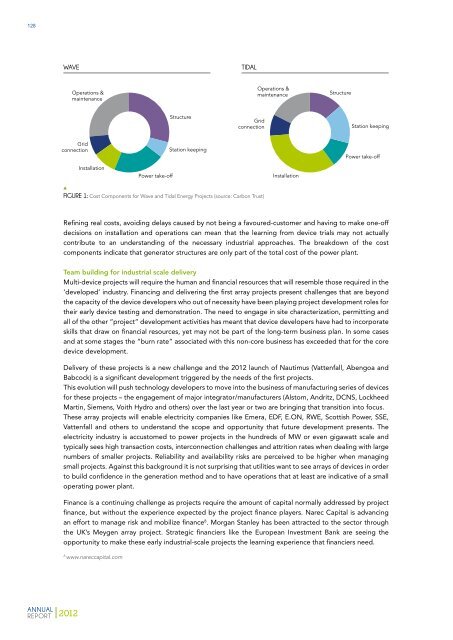

FIGURE 1: Cost Components for Wave and Tidal <strong>Energy</strong> Projects (source: Carbon Trust)<br />

Refining real costs, avoiding delays caused by not being a favoured-customer and having to make one-off<br />

decisions on installation and operations can mean that the learning from device trials may not actually<br />

contribute to an understanding of the necessary industrial approaches. The breakdown of the cost<br />

components indicate that generator structures are only part of the total cost of the power plant.<br />

Team building for industrial scale delivery<br />

Multi-device projects will require the human and financial resources that will resemble those required in the<br />

‘developed’ industry. Financing and delivering the first array projects present challenges that are beyond<br />

the capacity of the device developers who out of necessity have been playing project development roles for<br />

their early device testing and demonstration. The need to engage in site characterization, permitting and<br />

all of the other “project” development activities has meant that device developers have had to incorporate<br />

skills that draw on financial resources, yet may not be part of the long-term business plan. In some cases<br />

and at some stages the “burn rate” associated with this non-core business has exceeded that for the core<br />

device development.<br />

Delivery of these projects is a new challenge and the <strong>2012</strong> launch of Nautimus (Vattenfall, Abengoa and<br />

Babcock) is a significant development triggered by the needs of the first projects.<br />

This evolution will push technology developers to move into the business of manufacturing series of devices<br />

for these projects – the engagement of major integrator/manufacturers (Alstom, Andritz, DCNS, Lockheed<br />

Martin, Siemens, Voith Hydro and others) over the last year or two are bringing that transition into focus.<br />

These array projects will enable electricity companies like Emera, EDF, E.ON, RWE, Scottish Power, SSE,<br />

Vattenfall and others to understand the scope and opportunity that future development presents. The<br />

electricity industry is accustomed to power projects in the hundreds of MW or even gigawatt scale and<br />

typically sees high transaction costs, interconnection challenges and attrition rates when dealing with large<br />

numbers of smaller projects. Reliability and availability risks are perceived to be higher when managing<br />

small projects. Against this background it is not surprising that utilities want to see arrays of devices in order<br />

to build confidence in the generation method and to have operations that at least are indicative of a small<br />

operating power plant.<br />

Finance is a continuing challenge as projects require the amount of capital normally addressed by project<br />

finance, but without the experience expected by the project finance players. Narec Capital is advancing<br />

an effort to manage risk and mobilize finance 8 . Morgan Stanley has been attracted to the sector through<br />

the UK’s Meygen array project. Strategic financiers like the European Investment Bank are seeing the<br />

opportunity to make these early industrial-scale projects the learning experience that financiers need.<br />

8<br />

www.nareccapital.com<br />

ANNUAL<br />

REPORT <strong>2012</strong>