STENA METALL AB - Stena Metall Group

STENA METALL AB - Stena Metall Group

STENA METALL AB - Stena Metall Group

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

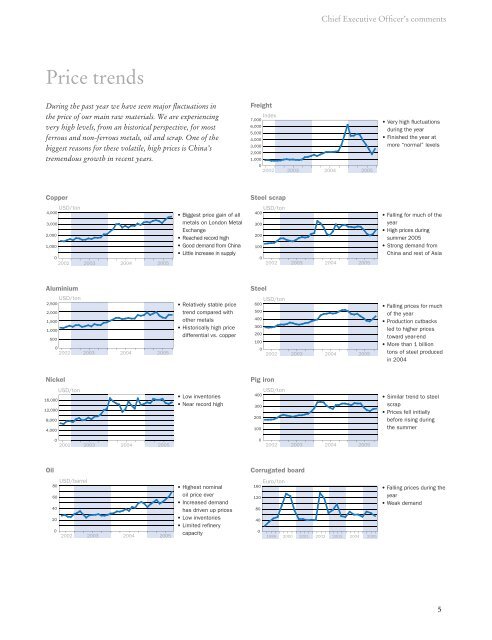

Chief Executive Officer’s comments<br />

Price trends<br />

During the past year we have seen major fluctuations in<br />

the price of our main raw materials. We are experiencing<br />

very high levels, from an historical perspective, for most<br />

ferrous and non-ferrous metals, oil and scrap. One of the<br />

biggest reasons for these volatile, high prices is China’s<br />

tremendous growth in recent years.<br />

Freight<br />

Index<br />

7,000<br />

6,000<br />

5,000<br />

4,000<br />

3,000<br />

2,000<br />

1,000<br />

0<br />

2002 2003<br />

2004 2005<br />

• Very high fl uctuations<br />

during the year<br />

• Finished the year at<br />

more “normal” levels<br />

Copper<br />

Steel scrap<br />

USD/ton<br />

4,000<br />

3,000<br />

2,000<br />

1,000<br />

0<br />

2002 2003<br />

2004 2005<br />

• Biggest price gain of all<br />

metals on London Metal<br />

Exchange<br />

• Reached record high<br />

• Good demand from China<br />

• Little increase in supply<br />

USD/ton<br />

400<br />

300<br />

200<br />

100<br />

0<br />

2002<br />

2003<br />

2004 2005<br />

• Falling for much of the<br />

year<br />

• High prices during<br />

summer 2005<br />

• Strong demand from<br />

China and rest of Asia<br />

Aluminium<br />

Steel<br />

USD/ton<br />

2,500<br />

2,000<br />

1,500<br />

1,000<br />

500<br />

0<br />

2002 2003<br />

2004 2005<br />

• Relatively stable price<br />

trend compared with<br />

other metals<br />

• Historically high price<br />

differential vs. copper<br />

USD/ton<br />

600<br />

500<br />

400<br />

300<br />

200<br />

100<br />

0<br />

2002<br />

2003<br />

2004 2005<br />

• Falling prices for much<br />

of the year<br />

• Production cutbacks<br />

led to higher prices<br />

toward year-end<br />

• More than 1 billion<br />

tons of steel produced<br />

in 2004<br />

Nickel<br />

Pig iron<br />

USD/ton<br />

16,000<br />

12,000<br />

8,000<br />

4,000<br />

• Low inventories<br />

• Near record high<br />

USD/ton<br />

400<br />

300<br />

200<br />

100<br />

• Similar trend to steel<br />

scrap<br />

• Prices fell initially<br />

before rising during<br />

the summer<br />

0<br />

2002 2003<br />

2004 2005<br />

0<br />

2002<br />

2003<br />

2004 2005<br />

Oil<br />

Corrugated board<br />

USD/barrel<br />

80<br />

60<br />

40<br />

20<br />

0<br />

2002 2003<br />

2004 2005<br />

• Highest nominal<br />

oil price ever<br />

• Increased demand<br />

has driven up prices<br />

• Low inventories<br />

• Limited refi nery<br />

capacity<br />

Euro/ton<br />

160<br />

120<br />

80<br />

40<br />

0<br />

1999<br />

2000<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

• Falling prices during the<br />

year<br />

• Weak demand<br />

5