City and County of Denver Municipal Airport System ANNUAL ...

City and County of Denver Municipal Airport System ANNUAL ...

City and County of Denver Municipal Airport System ANNUAL ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>City</strong> <strong>and</strong> <strong>County</strong> <strong>of</strong> <strong>Denver</strong><br />

<strong>Municipal</strong> <strong>Airport</strong> <strong>System</strong><br />

NOTES TO FINANCIAL STATEMENTS<br />

December 31, 2010 <strong>and</strong> 2009<br />

for three month deposits <strong>of</strong> U.S. dollars payable by Loop Financial Products I LLC. The <strong>City</strong> received $22,100,000<br />

from Loop Financial Products I LLC to assist in paying the settlement amount <strong>of</strong> $22,213,550 due to Lehman Brothers<br />

Special Financing. As a result <strong>of</strong> receiving $22,100,000 from Loop Financial Product I LLC, the fixed rate to be paid<br />

by the <strong>City</strong> to Loop Financial Products I LLC will take into account such payments <strong>and</strong> will be above the market rate.<br />

The net effect <strong>of</strong> the 2008B Swap Agreement, when considered together with the variable rate Series 2008C1 bonds, is<br />

that the <strong>Airport</strong> <strong>System</strong> will effectively pay a fixed rate on $100 million, plus or minus the difference between the<br />

actual rate on $92.6 million <strong>of</strong> the Series 2008C1 Bonds <strong>and</strong> 70% <strong>of</strong> three month LIBOR on $100 million notional<br />

amount <strong>of</strong> swaps.<br />

The <strong>Airport</strong> <strong>System</strong> is exposed to basis risk under the 2008B Swap Agreement, due to the differences between the<br />

variable interest rate it pays on the associated debt <strong>and</strong> 70% <strong>of</strong> three month LIBOR received under the 2008B Swap<br />

Agreement. The fixed rate payable by the <strong>Airport</strong> <strong>System</strong> under the 2008B Swap Agreement is 4.76%. The 2008B<br />

Swap Agreement became effective on January 8, 2009 <strong>and</strong> payments under this Agreement commenced on<br />

February 1, 2009.<br />

The 2009A Swap Agreement – On January 12, 2010, the <strong>Airport</strong> <strong>System</strong> terminated the 1999 <strong>and</strong> 2002 Swap<br />

Agreements with RFPC, Ltd. Due to the deterioration in the credit ratings <strong>of</strong> AMBAC, the credit support provider for<br />

the swap. The <strong>Airport</strong> <strong>System</strong> simultaneously entered into an interest rate swap agreement (“the 2009A Swap<br />

Agreement”) with Loop Financial Products I LLC. The fixed rate payable <strong>and</strong> variable rate index receivable on the<br />

2009A Swap is identical to the terminated 1999 Swap. Because the fixed rate was higher than current market<br />

conditions; however, the <strong>Airport</strong> <strong>System</strong> received $10,570,000 from Loop Financial Products I LLC for the <strong>of</strong>f-market<br />

portion <strong>of</strong> the swap. These proceeds were used to pay a portion <strong>of</strong> the settlement amount <strong>of</strong> $11,460,000 due to RFPC,<br />

Ltd. As a result <strong>of</strong> receiving proceeds <strong>of</strong> $10,570,000 from Loop Financial Products I LLC, this transaction is booked<br />

as a loan, including interest imputed at an implied rate <strong>of</strong> 5.667%, which will be paid through the fixed rate to be paid<br />

by the <strong>Airport</strong> <strong>System</strong> to Loop Financial Products I LLC.<br />

The 2009A Swap Agreement has a notional amount <strong>of</strong> $50 million <strong>and</strong> provide for certain payments to or from the<br />

financial institution equal to the difference between a fixed rate payable by the <strong>Airport</strong> <strong>System</strong> under the Agreement<br />

<strong>and</strong> the SIFMA Index payable by the respective financial institution.<br />

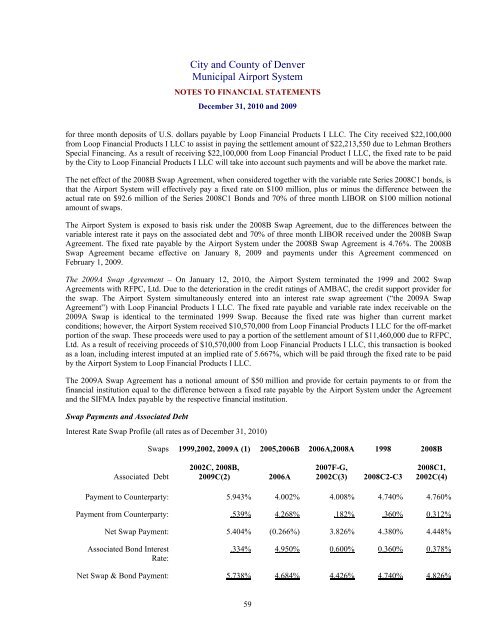

Swap Payments <strong>and</strong> Associated Debt<br />

Interest Rate Swap Pr<strong>of</strong>ile (all rates as <strong>of</strong> December 31, 2010)<br />

Swaps<br />

1999,2002, 2009A (1)<br />

2005,2006B<br />

2006A,2008A<br />

1998<br />

2008B<br />

Associated Debt<br />

2002C, 2008B,<br />

2009C(2)<br />

2006A<br />

2007F-G,<br />

2002C(3)<br />

2008C2-C3<br />

2008C1,<br />

2002C(4)<br />

Payment to Counterparty: 5.943% 4.002% 4.008% 4.740% 4.760%<br />

Payment from Counterparty: .539% 4.268% .182% .360% 0.312%<br />

Net Swap Payment: 5.404% (0.266%) 3.826% 4.380% 4.448%<br />

Associated Bond Interest<br />

Rate:<br />

.334% 4.950% 0.600% 0.360% 0.378%<br />

Net Swap & Bond Payment: 5.738% 4.684% 4.426% 4.740% 4.826%<br />

59