Vol. 2010, No. 11 (06/01/2010) PDF - Administrative Rules - Utah.gov

Vol. 2010, No. 11 (06/01/2010) PDF - Administrative Rules - Utah.gov

Vol. 2010, No. 11 (06/01/2010) PDF - Administrative Rules - Utah.gov

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

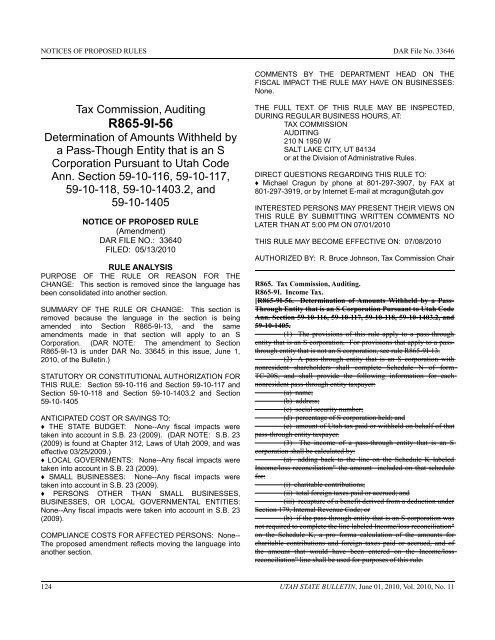

NOTICES OF PROPOSED RULES DAR File <strong>No</strong>. 33646<br />

33640<br />

Tax Commission, Auditing<br />

R865-9I-56<br />

Determination of Amounts Withheld by<br />

a Pass-Though Entity that is an S<br />

Corporation Pursuant to <strong>Utah</strong> Code<br />

Ann. Section 59-10-<strong>11</strong>6, 59-10-<strong>11</strong>7,<br />

59-10-<strong>11</strong>8, 59-10-1403.2, and<br />

59-10-1405<br />

NOTICE OF PROPOSED RULE<br />

(Amendment)<br />

DAR FILE NO.: 33640<br />

FILED: 05/13/<strong>2<strong>01</strong>0</strong><br />

RULE ANALYSIS<br />

PURPOSE OF THE RULE OR REASON FOR THE<br />

CHANGE: This section is removed since the language has<br />

been consolidated into another section.<br />

SUMMARY OF THE RULE OR CHANGE: This section is<br />

removed because the language in the section is being<br />

amended into Section R865-9I-13, and the same<br />

amendments made in that section will apply to an S<br />

Corporation. (DAR NOTE: The amendment to Section<br />

R865-9I-13 is under DAR <strong>No</strong>. 33645 in this issue, June 1,<br />

<strong>2<strong>01</strong>0</strong>, of the Bulletin.)<br />

STATUTORY OR CONSTITUTIONAL AUTHORIZATION FOR<br />

THIS RULE: Section 59-10-<strong>11</strong>6 and Section 59-10-<strong>11</strong>7 and<br />

Section 59-10-<strong>11</strong>8 and Section 59-10-1403.2 and Section<br />

59-10-1405<br />

ANTICIPATED COST OR SAVINGS TO:<br />

♦ THE STATE BUDGET: <strong>No</strong>ne--Any fiscal impacts were<br />

taken into account in S.B. 23 (2009). (DAR NOTE: S.B. 23<br />

(2009) is found at Chapter 312, Laws of <strong>Utah</strong> 2009, and was<br />

effective 03/25/2009.)<br />

♦ LOCAL GOVERNMENTS: <strong>No</strong>ne--Any fiscal impacts were<br />

taken into account in S.B. 23 (2009).<br />

♦ SMALL BUSINESSES: <strong>No</strong>ne--Any fiscal impacts were<br />

taken into account in S.B. 23 (2009).<br />

♦ PERSONS OTHER THAN SMALL BUSINESSES,<br />

BUSINESSES, OR LOCAL GOVERNMENTAL ENTITIES:<br />

<strong>No</strong>ne--Any fiscal impacts were taken into account in S.B. 23<br />

(2009).<br />

COMPLIANCE COSTS FOR AFFECTED PERSONS: <strong>No</strong>ne--<br />

The proposed amendment reflects moving the language into<br />

another section.<br />

COMMENTS BY THE DEPARTMENT HEAD ON THE<br />

FISCAL IMPACT THE RULE MAY HAVE ON BUSINESSES:<br />

<strong>No</strong>ne.<br />

THE FULL TEXT OF THIS RULE MAY BE INSPECTED,<br />

DURING REGULAR BUSINESS HOURS, AT:<br />

TAX COMMISSION<br />

AUDITING<br />

210 N 1950 W<br />

SALT LAKE CITY, UT 84134<br />

or at the Division of <strong>Administrative</strong> <strong>Rules</strong>.<br />

DIRECT QUESTIONS REGARDING THIS RULE TO:<br />

♦ Michael Cragun by phone at 8<strong>01</strong>-297-3907, by FAX at<br />

8<strong>01</strong>-297-3919, or by Internet E-mail at mcragun@utah.<strong>gov</strong><br />

INTERESTED PERSONS MAY PRESENT THEIR VIEWS ON<br />

THIS RULE BY SUBMITTING WRITTEN COMMENTS NO<br />

LATER THAN AT 5:00 PM ON 07/<strong>01</strong>/<strong>2<strong>01</strong>0</strong><br />

THIS RULE MAY BECOME EFFECTIVE ON: 07/08/<strong>2<strong>01</strong>0</strong><br />

AUTHORIZED BY: R. Bruce Johnson, Tax Commission Chair<br />

R865. Tax Commission, Auditing.<br />

R865-9I. Income Tax.<br />

[R865-9I-56. Determination of Amounts Withheld by a Pass-<br />

Through Entity that is an S Corporation Pursuant to <strong>Utah</strong> Code<br />

Ann. Section 59-10-<strong>11</strong>6, 59-10-<strong>11</strong>7, 59-10-<strong>11</strong>8, 59-10-1403.2, and<br />

59-10-1405.<br />

(1) The provisions of this rule apply to a pass-through<br />

entity that is an S corporation. For provisions that apply to a passthrough<br />

entity that is not an S corporation, see rule R865-9I-13.<br />

(2) A pass-through entity that is an S corporation with<br />

nonresident shareholders shall complete Schedule N of form<br />

TC-20S, and shall provide the following information for each<br />

nonresident pass-through entity taxpayer:<br />

(a) name;<br />

(b) address;<br />

(c) social security number;<br />

(d) percentage of S corporation held; and<br />

(e) amount of <strong>Utah</strong> tax paid or withheld on behalf of that<br />

pass-through entity taxpayer.<br />

(3) The income of a pass-through entity that is an S<br />

corporation shall be calculated by:<br />

(a) adding back to the line on the Schedule K labeled<br />

Income/loss reconciliation" the amount included on that schedule<br />

for:<br />

(i) charitable contributions;<br />

(ii) total foreign taxes paid or accrued; and<br />

(iii) recapture of a benefit derived from a deduction under<br />

Section 179, Internal Revenue Code; or<br />

(b) if the pass-through entity that is an S corporation was<br />

not required to complete the line labeled Income/loss reconciliation"<br />

on the Schedule K, a pro forma calculation of the amounts for<br />

charitable contributions and foreign taxes paid or accrued, and of<br />

the amount that would have been entered on the Income/loss<br />

reconciliation" line shall be used for purposes of this rule.<br />

124 UTAH STATE BULLETIN, June <strong>01</strong>, <strong>2<strong>01</strong>0</strong>, <strong>Vol</strong>. <strong>2<strong>01</strong>0</strong>, <strong>No</strong>. <strong>11</strong>

![Lynx avoidance [PDF] - Wisconsin Department of Natural Resources](https://img.yumpu.com/41279089/1/159x260/lynx-avoidance-pdf-wisconsin-department-of-natural-resources.jpg?quality=85)