DownloadAsset?assetId=F14FC0EBB1C24FAC93A09302BE386549&filename=moe_vsb_review_report_june_2015

DownloadAsset?assetId=F14FC0EBB1C24FAC93A09302BE386549&filename=moe_vsb_review_report_june_2015

DownloadAsset?assetId=F14FC0EBB1C24FAC93A09302BE386549&filename=moe_vsb_review_report_june_2015

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

3. Budget development and forecasting<br />

3.1 Introduction<br />

3.1.1 Purpose of a budget/budgeting in the education sector<br />

A budget is a summary plan of the expected revenues and intended use of the revenues of an<br />

organization. It also serves as a planning and business performance monitoring tool. A budget is a<br />

composition of assumptions that results in a cohesive financial framework for current and future time<br />

periods. These assumptions include:<br />

1) Probable assumptions – assumptions that:<br />

a) Management believes reflect the more likely set of economic conditions and planned<br />

courses of action, suitably supported and that are consistent with Management’s<br />

operating plans; and<br />

b) Provide a reasonable basis of the budget’s use.<br />

2) Hypothetical assumptions – assumptions about a set of economic conditions or courses of<br />

action that are not necessarily the most probable in Management’s judgment, but are<br />

consistent with the purpose of the budget and future directions of the enterprise.<br />

VBE’s annual budgets are the financial outlines of the District’s educational program. Both the Board<br />

and VBE regard the budgeting process as an important function/critical element of the management<br />

and operation of the school district. The budgeting process serves as a means to improve<br />

communications and goal-setting involving both the District and its stakeholders.<br />

VBE submits its budgets to MEd in the Excel template prescribed by the Ministry. All school districts are<br />

required to use the same format and template, enabling comparability of budgets and financial results<br />

between the districts.<br />

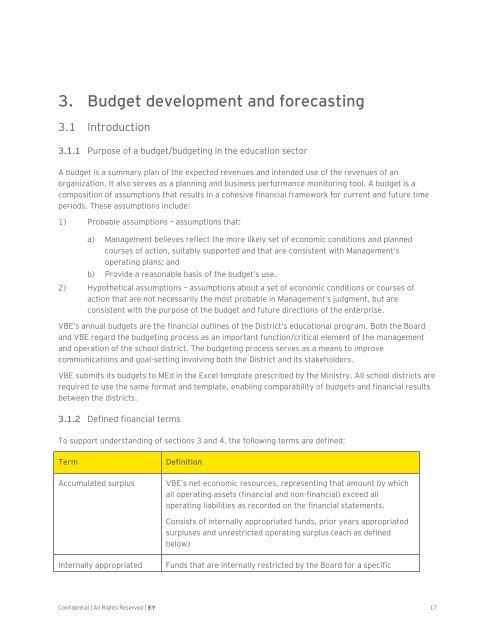

3.1.2 Defined financial terms<br />

To support understanding of sections 3 and 4, the following terms are defined:<br />

Term<br />

Accumulated surplus<br />

Definition<br />

VBE’s net economic resources, representing that amount by which<br />

all operating assets (financial and non-financial) exceed all<br />

operating liabilities as recorded on the financial statements.<br />

Consists of internally appropriated funds, prior years appropriated<br />

surpluses and unrestricted operating surplus (each as defined<br />

below)<br />

Internally appropriated<br />

Funds that are internally restricted by the Board for a specific<br />

Confidential | All Rights Reserved | EY 17