DownloadAsset?assetId=F14FC0EBB1C24FAC93A09302BE386549&filename=moe_vsb_review_report_june_2015

DownloadAsset?assetId=F14FC0EBB1C24FAC93A09302BE386549&filename=moe_vsb_review_report_june_2015

DownloadAsset?assetId=F14FC0EBB1C24FAC93A09302BE386549&filename=moe_vsb_review_report_june_2015

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

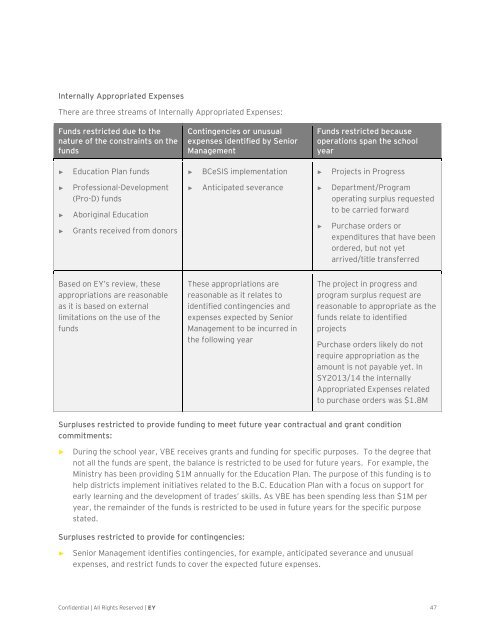

Internally Appropriated Expenses<br />

There are three streams of Internally Appropriated Expenses:<br />

Funds restricted due to the<br />

nature of the constraints on the<br />

funds<br />

Contingencies or unusual<br />

expenses identified by Senior<br />

Management<br />

Funds restricted because<br />

operations span the school<br />

year<br />

►<br />

Education Plan funds<br />

►<br />

BCeSIS implementation<br />

►<br />

Projects in Progress<br />

►<br />

►<br />

►<br />

Professional-Development<br />

(Pro-D) funds<br />

Aboriginal Education<br />

Grants received from donors<br />

►<br />

Anticipated severance<br />

►<br />

►<br />

Department/Program<br />

operating surplus requested<br />

to be carried forward<br />

Purchase orders or<br />

expenditures that have been<br />

ordered, but not yet<br />

arrived/title transferred<br />

Based on EY’s <strong>review</strong>, these<br />

appropriations are reasonable<br />

as it is based on external<br />

limitations on the use of the<br />

funds<br />

These appropriations are<br />

reasonable as it relates to<br />

identified contingencies and<br />

expenses expected by Senior<br />

Management to be incurred in<br />

the following year<br />

The project in progress and<br />

program surplus request are<br />

reasonable to appropriate as the<br />

funds relate to identified<br />

projects<br />

Purchase orders likely do not<br />

require appropriation as the<br />

amount is not payable yet. In<br />

SY2013/14 the internally<br />

Appropriated Expenses related<br />

to purchase orders was $1.8M<br />

Surpluses restricted to provide funding to meet future year contractual and grant condition<br />

commitments:<br />

►<br />

During the school year, VBE receives grants and funding for specific purposes. To the degree that<br />

not all the funds are spent, the balance is restricted to be used for future years. For example, the<br />

Ministry has been providing $1M annually for the Education Plan. The purpose of this funding is to<br />

help districts implement initiatives related to the B.C. Education Plan with a focus on support for<br />

early learning and the development of trades’ skills. As VBE has been spending less than $1M per<br />

year, the remainder of the funds is restricted to be used in future years for the specific purpose<br />

stated.<br />

Surpluses restricted to provide for contingencies:<br />

►<br />

Senior Management identifies contingencies, for example, anticipated severance and unusual<br />

expenses, and restrict funds to cover the expected future expenses.<br />

Confidential | All Rights Reserved | EY 47