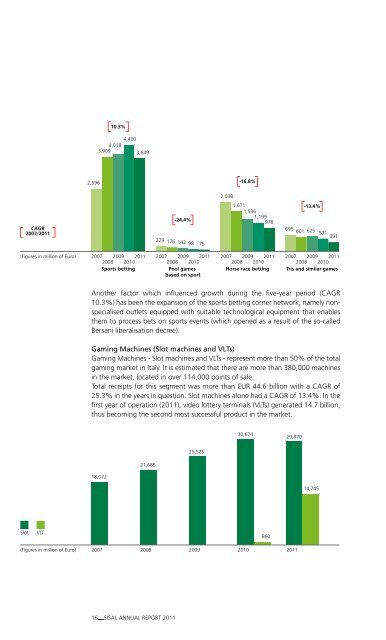

Segment analysisLotteriesAs stated above, the lottery segment recorded an overall growth rate of 4.9%.National co-totalisator number games (known as NTNG games: SuperEnalotto, Vinciper lon-ne is the sole concessionaire, recorded a CAGR of 5.4% with total receipts inla vita - Win for Life and Si Vince Tutto SuperEnalotto), of which the <strong>Sisal</strong> GroupS.p.A.<strong>2011</strong>, 23.5% higher than in 2007 and indicative of the growth of this segmentachieved over the years by the Group’s management. GNTN recorded a positiveperformance even net of uncontrollable external variables, such as the extremelyhigh jackpots in 2009 and 2010 which led to record receipts.The <strong>2011</strong> Lotto gaming includes traditional Lotto and the new 10eLOTTO. TheCAGR during the period from 2007 to <strong>2011</strong> was 2.5% and, especially thanks tothe contribution made by the new game, Lotto started to grow again in <strong>2011</strong>(+30%) after several years of decline; the instant lotteries (the so-called Scratchand Win) helped the lottery segment to take second place in terms of the totalreceipts in the gaming market (third, if we consider the new video lotteries separatelyfrom the other gaming machines) with a CAGR of more than 6% during theperiod from 2007 to <strong>2011</strong>.6.4%9,2749,435 9,36710,230112.5%7,9516,7956,1505,8525,6335,2315.4%3,7773,524CAGR2007/<strong>2011</strong>2,5091,9402,396(Figures in million of Euro)200720082009 2010Lotto<strong>2011</strong>20072008 2009 2010Scratchcard<strong>2011</strong>20072008 2009 2010 <strong>2011</strong>National TotalisatorNumbers GamesBettingThe betting sector showed essentially negative values for each of the segmentsanalyzed, with the exception of Sports Betting. The horse racing segment and thetraditional Totocalcio segment (referred to here as pool games) have undergone acrisis which started several years ago, while in the case of sports betting, the reasonsfor the trend over the last years are, to a greater extent, linked to the structureof the product itself.In fact, sports betting volumes are materially influenced by the payout and in 2009and 2010, thanks to payout percentages around 90%, betting receipts were noticeablyhigher, while the payout value was 77% in <strong>2011</strong> and even lower in 2007(76%) and 2008 (75.8%).15 DIRECTORS’ REPORT ON operations

ne10.3%4,4004,0183,9093,8492,596-16.8%2,038CAGR2007/<strong>2011</strong>-24.4%229 176 143 98751,6711,5361,199978-13.4%695601 625531391(Figures in million of Euro)Slot VLT(Figures in million of Euro)2007 2009 <strong>2011</strong>2008 2010Sports bettingcolonneAnother factor which influenced growth during the five-year period (CAGR10.3%) has been the expansion of the sports betting corner network, namely nonspecialisedoutlets equipped with suitable technological equipment that enablesthem to process bets on sports events (which opened as a result of the so-calledBersani liberalisation decree).Gaming Machines (Slot machines and VLTs)Gaming Machines - Slot machines and VLTs - represent more than 50% of the totalgaming market in Italy. It is estimated that there are more than 380,000 machinesin the market, located in over 114,000 points of sale.Total receipts for this segment was more than EUR 44.6 billion with a CAGR of25.3% in the years in question. Slot machines alone had a CAGR of 13.4%. In thefirst year of operation (<strong>2011</strong>), video lottery terminals (VLTs) generated 14.7 billion,thus becoming the second most successful product in the market.18,07221,6852007 2009 <strong>2011</strong>2008 2010Pool gamesbased on sport25,5252007 2009 <strong>2011</strong>2008 2010Horse race betting30,6742007 2008 2009 20108602007 2009 <strong>2011</strong>2008 2010Tris and similar games29,870<strong>2011</strong>14,7453500030000250002000015000100005000016 <strong>Sisal</strong> ANNUAL REPORT <strong>2011</strong>