- Page 1: ANNUAL REPORT 2009-10ANNUAL REPORT2

- Page 4 and 5: ANNUAL REPORT 2009-10PART IIISTATUT

- Page 6 and 7: ANNUAL REPORT 2009-1027. Net Incurr

- Page 8 and 9: ANNUAL REPORT 2009-1046. Underwriti

- Page 10 and 11: ANNUAL REPORT 2009-10TEAM AT IRDAJ.

- Page 12 and 13: ANNUAL REPORT 2009-10Prabodh Chande

- Page 14 and 15: ANNUAL REPORT 2009-10NAMEMahesh Aga

- Page 16 and 17: ANNUAL REPORT 2009-10Randip Singh J

- Page 18 and 19: ANNUAL REPORT 2009-10in financial s

- Page 20 and 21: ANNUAL REPORT 2009-10during the yea

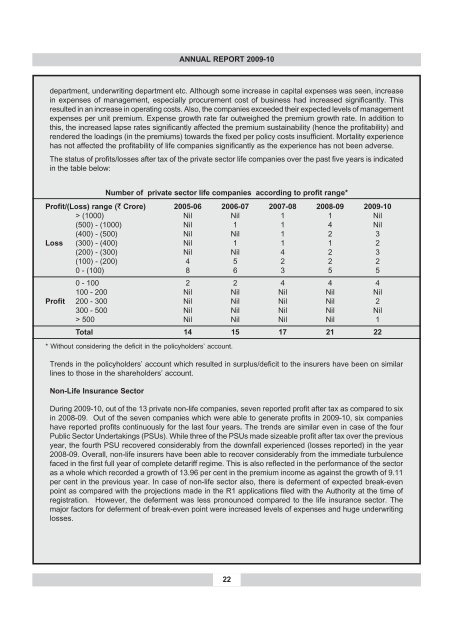

- Page 22 and 23: ANNUAL REPORT 2009-10Corporate Gove

- Page 24 and 25: ANNUAL REPORT 2009-108

- Page 26 and 27: ANNUAL REPORT 2009-10during 2009-10

- Page 28 and 29: ANNUAL REPORT 2009-10Insurance pene

- Page 30 and 31: ANNUAL REPORT 2009-103. APPRAISAL O

- Page 32 and 33: ANNUAL REPORT 2009-10Market ShareI.

- Page 34 and 35: ANNUAL REPORT 2009-10I.3.16 The ope

- Page 36 and 37: that companies in the life sector t

- Page 40 and 41: ANNUAL REPORT 2009-10declined in ca

- Page 42 and 43: ANNUAL REPORT 2009-10TABLE 23PAID U

- Page 44 and 45: ANNUAL REPORT 2009-10TABLE 28INCURR

- Page 46 and 47: ANNUAL REPORT 2009-10Star Health an

- Page 48 and 49: ANNUAL REPORT 2009-10prevailing as

- Page 50 and 51: ANNUAL REPORT 2009-104.2 MAINTENANC

- Page 52 and 53: ANNUAL REPORT 2009-10I.4.3.3 The Re

- Page 54 and 55: ANNUAL REPORT 2009-10I.4.4.1 During

- Page 56 and 57: ANNUAL REPORT 2009-10TABLE 38DEVELO

- Page 58 and 59: I.4.5.5 Based on a further segregat

- Page 60 and 61: ANNUAL REPORT 2009-10I.4.6.5 The re

- Page 62 and 63: ANNUAL REPORT 2009-10In the days to

- Page 64 and 65: ANNUAL REPORT 2009-10I.4.6.13 The A

- Page 66 and 67: ANNUAL REPORT 2009-10into account w

- Page 68 and 69: ANNUAL REPORT 2009-10actually make

- Page 70 and 71: ANNUAL REPORT 2009-10was a quantum

- Page 72 and 73: ANNUAL REPORT 2009-10TABLE 51GROUP

- Page 74 and 75: ANNUAL REPORT 2009-1058

- Page 76 and 77: ANNUAL REPORT 2009-10II.2.2 The tur

- Page 78 and 79: ANNUAL REPORT 2009-10TABLE 58GROUP

- Page 80 and 81: ANNUAL REPORT 2009-10II.2.12 During

- Page 82 and 83: ANNUAL REPORT 2009-10Since no relie

- Page 84 and 85: ANNUAL REPORT 2009-10II.5.2 During

- Page 86 and 87: ANNUAL REPORT 2009-10TABLE 69STATUS

- Page 88 and 89:

ANNUAL REPORT 2009-10GENERAL INSURA

- Page 90 and 91:

ANNUAL REPORT 2009-10• Disseminat

- Page 92 and 93:

ANNUAL REPORT 2009-102. Protection

- Page 94 and 95:

ANNUAL REPORT 2009-107. Levying fee

- Page 96 and 97:

ANNUAL REPORT 2009-10III.11.4 Also,

- Page 98 and 99:

ANNUAL REPORT 2009-10(b)Social Sect

- Page 100 and 101:

ANNUAL REPORT 2009-10issues on the

- Page 102 and 103:

ANNUAL REPORT 2009-10IV.6.13 The pr

- Page 104 and 105:

ANNUAL REPORT 2009-1088

- Page 106 and 107:

ANNUAL REPORT 2009-10INTERNATIONAL

- Page 108 and 109:

ANNUAL REPORT 2009-10TOTAL LIFE INS

- Page 110 and 111:

ANNUAL REPORT 2009-10INDIVIDUAL NEW

- Page 112 and 113:

ANNUAL REPORT 2009-10GROUP NEW BUSI

- Page 114 and 115:

ANNUAL REPORT 2009-10STATE WISE IND

- Page 116 and 117:

ANNUAL REPORT 2009-10INDIVIDUAL BUS

- Page 118 and 119:

ANNUAL REPORT 2009-10LINKED AND NON

- Page 120 and 121:

ANNUAL REPORT 2009-10LINKED AND NON

- Page 122 and 123:

ANNUAL REPORT 2009-10INDIVIDUAL DEA

- Page 124 and 125:

ANNUAL REPORT 2009-10GROUP DEATH CL

- Page 126 and 127:

ANNUAL REPORT 2009-10DURATION WISE

- Page 128 and 129:

ANNUAL REPORT 2009-10ASSETS UNDER M

- Page 130 and 131:

ANNUAL REPORT 2009-10EQUITY SHARE C

- Page 132 and 133:

ANNUAL REPORT 2009-10LIFE INSURERS

- Page 134 and 135:

ANNUAL REPORT 2009-10LIFE INSURERS

- Page 136 and 137:

ANNUAL REPORT 2009-10LIFE INSURERS

- Page 138 and 139:

ANNUAL REPORT 2009-10LIFE INSURERS

- Page 140 and 141:

ANNUAL REPORT 2009-10LIFE INSURERS

- Page 142 and 143:

ANNUAL REPORT 2009-10LIFE INSURANCE

- Page 144 and 145:

ANNUAL REPORT 2009-10INDIVIDUAL BUS

- Page 146 and 147:

ANNUAL REPORT 2009-10STATEMENT 27DE

- Page 148 and 149:

ANNUAL REPORT 2009-10REGION WISE DI

- Page 150 and 151:

ANNUAL REPORT 2009-10STATEMENT 31NE

- Page 152 and 153:

ANNUAL REPORT 2009-10Cont’d... ST

- Page 154 and 155:

ANNUAL REPORT 2009-10DEATH CLAIMS U

- Page 156 and 157:

ANNUAL REPORT 2009-10STATEMENT 35DU

- Page 158 and 159:

ANNUAL REPORT 2009-10LIST OF MICRO

- Page 160 and 161:

ANNUAL REPORT 2009-10SEGMENT WISE G

- Page 162 and 163:

ANNUAL REPORT 2009-10CHANNEL WISE G

- Page 164 and 165:

ANNUAL REPORT 2009-10STATEMENT 43NE

- Page 166 and 167:

ANNUAL REPORT 2009-10INCURRED CLAIM

- Page 168 and 169:

ANNUAL REPORT 2009-10UNDERWRITING E

- Page 170 and 171:

ANNUAL REPORT 2009-10ASSETS UNDER M

- Page 172 and 173:

ANNUAL REPORT 2009-10SOLVENCY RATIO

- Page 174 and 175:

ANNUAL REPORT 2009-10PUBLIC SECTOR

- Page 176 and 177:

ANNUAL REPORT 2009-10PUBLIC SECTOR

- Page 178 and 179:

ANNUAL REPORT 2009-10PRIVATE SECTOR

- Page 180 and 181:

ANNUAL REPORT 2009-10PRIVATE SECTOR

- Page 182 and 183:

ANNUAL REPORT 2009-10PRIVATE SECTOR

- Page 184 and 185:

ANNUAL REPORT 2009-10PRIVATE SECTOR

- Page 186 and 187:

ANNUAL REPORT 2009-10HEALTH INSURER

- Page 188 and 189:

ANNUAL REPORT 2009-10HEALTH INSURER

- Page 190 and 191:

ANNUAL REPORT 2009-10EXPORT CREDIT

- Page 192 and 193:

ANNUAL REPORT 2009-10AGRICULTURE IN

- Page 194 and 195:

ANNUAL REPORT 2009-10STATEMENT 65AG

- Page 196 and 197:

ANNUAL REPORT 2009-10STATEMENT 67GE

- Page 198 and 199:

ANNUAL REPORT 2009-10STATE-WISE NUM

- Page 200 and 201:

ANNUAL REPORT 2009-10STATEMENT 70TH

- Page 202 and 203:

ANNUAL REPORT 2009-10STATUS OF GRIE

- Page 204 and 205:

ANNUAL REPORT 2009-10STATUS OF GRIE

- Page 206 and 207:

ANNUAL REPORT 2009-10PERFORMANCE OF

- Page 208 and 209:

ANNUAL REPORT 2009-10PERFORMANCE OF

- Page 210 and 211:

ANNUAL REPORT 2009-10194

- Page 212 and 213:

ANNUAL REPORT 2009-10Cont’d... AN

- Page 214 and 215:

ANNUAL REPORT 2009-10INDIAN ASSURED

- Page 216 and 217:

ANNUAL REPORT 2009-10ANNEX 4LIFE IN

- Page 218 and 219:

ANNUAL REPORT 2009-10Cont’d... AN

- Page 220 and 221:

ANNUAL REPORT 2009-10Cont’d... AN

- Page 222 and 223:

ANNUAL REPORT 2009-10LIFE INSURANCE

- Page 224 and 225:

ANNUAL REPORT 2009-10NON-LIFE INSUR

- Page 226 and 227:

ANNUAL REPORT 2009-10NON-LIFE INSUR

- Page 228 and 229:

ANNUAL REPORT 2009-10STATE-WISE NUM

- Page 230 and 231:

ANNUAL REPORT 2009-10Cont’d... AN

- Page 232 and 233:

ANNUAL REPORT 2009-10Cont’d... AN

- Page 234 and 235:

ANNUAL REPORT 2009-10218

- Page 236 and 237:

ANNUAL REPORT 2009-10220

- Page 238 and 239:

ANNUAL REPORT 2009-10Authority (IRD

- Page 240 and 241:

1. Adequacy of Internal Audit Syste

- Page 242 and 243:

ANNUAL REPORT 2009-10INSURANCE REGU

- Page 244 and 245:

ANNUAL REPORT 2009-10INSURANCE REGU

- Page 246 and 247:

ANNUAL REPORT 2009-10INSURANCE REGU

- Page 248 and 249:

ANNUAL REPORT 2009-10INSURANCE REGU

- Page 250 and 251:

ANNUAL REPORT 2009-10INSURANCE REGU

- Page 252 and 253:

ANNUAL REPORT 2009-10INSURANCE REGU

- Page 254 and 255:

ANNUAL REPORT 2009-10INSURANCE REGU

- Page 256 and 257:

ANNUAL REPORT 2009-10INSURANCE REGU

- Page 258 and 259:

ANNUAL REPORT 2009-10ANNEXURE VIINS

- Page 260 and 261:

ANNUAL REPORT 2009-10ANNEXURE VIIII

- Page 262 and 263:

ANNUAL REPORT 2009-10(ii)License Fe

- Page 264 and 265:

dm{f©H$ [anmoQ>© 2009-10dm{f©H$

- Page 266 and 267:

dm{f©H$ [anmoQ>© 2009-10bú` H$WZ

- Page 268 and 269:

dm{f©H$ [anmoQ>© 2009-10^mJ-IVg§

- Page 270 and 271:

dm{f©H$ [anmoQ>© 2009-10{ddaUm| H

- Page 272 and 273:

dm{f©H$ [anmoQ>© 2009-10bú` H$WZ

- Page 274 and 275:

dm{f©H$ [anmoQ>© 2009-10A§e H$m{

- Page 276 and 277:

dm{f©H$ [anmoQ>© 2009-10g§`wº$

- Page 278 and 279:

dm{f©H$ [anmoQ>© 2009-10ñdmñÏ`

- Page 280 and 281:

Yeejleer³e DeLe&J³eJemLee:1. Yeej

- Page 282 and 283:

dm{f©H$ [anmoQ>© 2009-10hegve&yee

- Page 284 and 285:

dm{f©H$ [anmoQ>© 2009-10men³eesi

- Page 286 and 287:

dm{f©H$ [anmoQ>© 2009-10keÀe mec

- Page 288 and 289:

1. mççcççv³ç DçççÆLç&kç

- Page 290 and 291:

1.2.4 60 ÒççÆlçMçlç oíMçç

- Page 292 and 293:

dm{f©H$ [anmoQ>© 2009-10lçççÆ

- Page 294 and 295:

dm{f©H$ [anmoQ>© 2009-10Jç

- Page 296 and 297:

dm{f©H$ [anmoQ>© 2009-10lçççÆ

- Page 298 and 299:

1.3.22: çÆvçpççÇpççÇJçvç

- Page 300 and 301:

dm{f©H$ [anmoQ>© 2009-101.3.33: c

- Page 302 and 303:

dm{f©H$ [anmoQ>© 2009-10kçÀj Y

- Page 304 and 305:

dm{f©H$ [anmoQ>© 2009-10Yççjlç

- Page 306 and 307:

dm{f©H$ [anmoQ>© 2009-101.3.46 :

- Page 308 and 309:

dm{f©H$ [anmoQ>© 2009-10pçyçç

- Page 310 and 311:

dm{f©H$ [anmoQ>© 2009-10³çÓç

- Page 312 and 313:

dm{f©H$ [anmoQ>© 2009-10HçççÆ

- Page 314 and 315:

dm{f©H$ [anmoQ>© 2009-104.3 Hçá

- Page 316 and 317:

dm{f©H$ [anmoQ>© 2009-101.4.3.8 J

- Page 318 and 319:

dm{f©H$ [anmoQ>© 2009-10SkçÀ k

- Page 320 and 321:

dm{f©H$ [anmoQ>© 2009-10pççÇJ

- Page 322 and 323:

dm{f©H$ [anmoQ>© 2009-101.4.5.8 J

- Page 324 and 325:

dm{f©H$ [anmoQ>© 2009-10GHçjçí

- Page 326 and 327:

dm{f©H$ [anmoQ>© 2009-10lçççÆ

- Page 328 and 329:

Jç

- Page 330 and 331:

dm{f©H$ [anmoQ>© 2009-10pççíj

- Page 332 and 333:

dm{f©H$ [anmoQ>© 2009-104.9 YZ {d

- Page 334 and 335:

dm{f©H$ [anmoQ>© 2009-10çÆpçm

- Page 336 and 337:

dm{f©H$ [anmoQ>© 2009-10lçççÆ

- Page 338 and 339:

1. yççÇcçç DççÌj Hçávçy

- Page 340 and 341:

dm{f©H$ [anmoQ>© 2009-10lçççÆ

- Page 342 and 343:

dm{f©H$ [anmoQ>© 2009-10lçççÆ

- Page 344 and 345:

dm{f©H$ [anmoQ>© 2009-10II.3.2 y

- Page 346 and 347:

dm{f©H$ [anmoQ>© 2009-10³çn Dç

- Page 348 and 349:

II.5.3. yççÇcçç DççF&Dççj[

- Page 350 and 351:

dm{f©H$ [anmoQ>© 2009-10II.6.7. p

- Page 352 and 353:

dm{f©H$ [anmoQ>© 2009-10nÌ ScçD

- Page 354 and 355:

yççÇcçç çÆJççÆvç³ççc

- Page 356 and 357:

dm{f©H$ [anmoQ>© 2009-10DççF&D

- Page 358 and 359:

dm{f©H$ [anmoQ>© 2009-10{ZJ{_V em

- Page 360 and 361:

dm{f©H$ [anmoQ>© 2009-10Fmç cç

- Page 362 and 363:

dm{f©H$ [anmoQ>© 2009-10Yççiç

- Page 364 and 365:

dm{f©H$ [anmoQ>© 2009-10IV.6.7 ç

- Page 366 and 367:

dm{f©H$ [anmoQ>© 2009-10{ddaU87

- Page 368 and 369:

dm{f©H$ [anmoQ>© 2009-10~r_m nhþ

- Page 370 and 371:

{ddaU 3(`. H$amo‹S> _|)~r_mH$Vm©

- Page 372 and 373:

{ddaU 5OrdZ ~r_mH$Vm©Am| Ho$ ì`{

- Page 374 and 375:

{ddaU 6OrdZ ~r_mH$mVm©Am| H$m df©

- Page 376 and 377:

{ddaU 7(n«r{_`_ H$amoS> ` _|)amÁ`

- Page 378 and 379:

Omar {ddaU 7(n«r{_`_ H$amoS> ` _|)

- Page 380 and 381:

{ddaU 9(` H$amo‹S> _|)~r_mH$Vm©

- Page 382 and 383:

Omar {ddaU 10(n«r{_`_ H$amoS> ` _o

- Page 384 and 385:

{ddaU 12(bm^ am{e ` H$amo‹S> _|)O

- Page 386 and 387:

{ddaU 13(bm^ am{e ` H$amo‹S> _|)O

- Page 388 and 389:

{ddaU 14(bm^ am{e ` H$amo‹S> _|)O

- Page 390 and 391:

{ddaU 16(` H$amo‹S> _|)~r_mH$Vm©

- Page 392 and 393:

~r_mH$Vm© `y{ZQ> qbŠS> \§$S>AZw_

- Page 394 and 395:

dm{f©H$ [anmoQ>© 2009-10OrdZ ~r_m

- Page 396 and 397:

Omar {ddaU 19(` bmI _|)dm{f©H$ [an

- Page 398 and 399:

{ddaU 20(` bmIm| _|){ddaU {~abm gZ

- Page 400 and 401:

Omar {ddaU 20(` bmIm| _|){ddaU â`y

- Page 402 and 403:

Omar {ddaU 21(` bmIm| _o){ddaU ~OmO

- Page 404 and 405:

dm{f©H$ [anmoQ>© 2009-10^maVr` Or

- Page 406 and 407:

{Z{Y`m| Ho$ ómoVeò a ny§Ordm{f©

- Page 408 and 409:

dm{f©H$ [anmoQ>© 2009-10OrdZ ~r_m

- Page 410 and 411:

amÁ`/ EJmoZ A{ddm ~OmO ^maVr {~abm

- Page 412 and 413:

{ddaU 30amÁ`/ EJmoZ A{ddm ~OmO ^ma

- Page 414 and 415:

{ddaU 32(bm^ am{e ` H$amoS> _o)OrdZ

- Page 416 and 417:

{ddaU 33(bm^ am{e ` H$amoS> _o)OrdZ

- Page 418 and 419:

2009-10 Ho$ {b`o Ad{YAZwgma gyú_ ~

- Page 420 and 421:

dm{f©H$ [anmoQ>© 2009-10~r_mH$Vm

- Page 422 and 423:

J¡aOrdZ ~r_mH$Vm©Am| H$m gH$b à

- Page 424 and 425:

[ddaU 40(` bmIm| _|)~r_mH$Vm© A{¾

- Page 426 and 427:

ddaU 42(` bmIm| _o)amÁ`/Ho$ÝÐ A{

- Page 428 and 429:

A{¾ g_w{Ð _moQ>a ñdmñÏ` AÝ` 2

- Page 430 and 431:

[ddaU 46(` bmIm| _o){ddaU Ý`y B§{

- Page 432 and 433:

EMS>rE\$Or BaJmo â`yMa OZabr `w{Zd

- Page 434 and 435:

dm{f©H$ [anmoQ>© 2009-10J¡a OrdZ

- Page 436 and 437:

[ddaU 51(` bmIm| _o)Ý`y BpÊS>`m A

- Page 438 and 439:

{ddaU 52(` bmIm| _o){ddaU Ý`y B{Ý

- Page 440 and 441:

{ddaU am`b gwÝXa_ ~OmO Abm`§O Q>m

- Page 442 and 443:

Omar... {ddaU 54(` bmIm| _o){ddaU M

- Page 444 and 445:

{ddaU ahoOm Š`y~rB© Hw$bA{¾ g_w

- Page 446 and 447:

Omar... {ddaU 55(` bmIm| _|){ddaU E

- Page 448 and 449:

Omar.... {ddaU 56(` bmIm| _o){ddaU

- Page 450 and 451:

dm{f©H$ [anmoQ>© 2009-10ñdmñÏ`

- Page 452 and 453:

dm{f©H$ [anmoQ>© 2009-10^maVr` {Z

- Page 454 and 455:

dm{f©H$ [anmoQ>© 2009-10^maVr` {Z

- Page 456 and 457:

dm{f©H$ [anmoQ>© 2009-10^maVr` H

- Page 458 and 459:

{ddaU 66(` bmIm| _o)2009-10 2008-09

- Page 460 and 461:

dm{f©H$ [anmoQ>© 2009-10^maVr` gm

- Page 462 and 463:

J¡a OrdZ ~r_mH$VmAm| Ho$ amÁ`mZwg

- Page 464 and 465:

dm{f©H$ [anmoQ>© 2009-10Vrgam nj

- Page 466 and 467:

dm{f©H$ [anmoQ>© 2009-10{eH$m`Vm|

- Page 468 and 469:

dm{f©H$ [anmoQ>© 2009-10{eH$m`Vm|

- Page 470 and 471:

dm{f©H$ [anmoQ>© 2009-10{d{^Þ Ho

- Page 472 and 473:

dm{f©H$ [anmoQ>© 2009-10g§b½ZH$

- Page 474 and 475:

dm{f©H$ [anmoQ>© 2009-10^maV _o H

- Page 476 and 477:

dm{f©H$ [anmoQ>© 2009-10~r_m§H$V

- Page 478 and 479:

dm{f©H$ [anmoQ>© 2009-10^maVr` Or

- Page 480 and 481:

dm{f©H$ [anmoQ>© 2009-10{dÎm df

- Page 482 and 483:

dm{f©H$ [anmoQ>© 2009-10{dÎm df

- Page 484 and 485:

dm{f©H$ [anmoQ>© 2009-10{dÎm df

- Page 486 and 487:

dm{f©H$ [anmoQ>© 2009-10{dÎm df

- Page 488 and 489:

dm{f©H$ [anmoQ>© 2009-10{dÎm df

- Page 490 and 491:

g§b¾H$ 6dm{f©H$ [anmoQ>© 2009-1

- Page 492 and 493:

peejer... mebueivekeÀ 8DeÒewue 20

- Page 494 and 495:

peejer... mebueivekeÀ 8DeÒewue 20

- Page 496 and 497:

dm{f©H$ [anmoQ>© 2009-10H«$.g§.

- Page 498 and 499:

dm{f©H$ [anmoQ>© 2009-10g§b½ZH$

- Page 500 and 501:

dm{f©H$ [anmoQ>© 2009-1031 ¨ÉÉ

- Page 502 and 503:

dm{f©H$ [anmoQ>© 2009-10iÉnù{É

- Page 504 and 505:

nyd© df© Ho$ {bE AmH§$S>| Xm{`Ë

- Page 506 and 507:

- ã`mO (ZmoQ 3> XoI|) 2,752,030 gd

- Page 508 and 509:

Omar... ànÌ (gr)H«$.g§ àm{á`m

- Page 510 and 511:

~¢H$ àma§{^H$ E\$S>rAma O_m ã`m

- Page 512 and 513:

Omar... g§b¾H$ IIdm{f©H$ [anmoQ>

- Page 514 and 515:

dm{f©H$ [anmoQ>© 2009-10235~r_m {

- Page 516 and 517:

dm{f©H$ [anmoQ>© 2009-10237~r_m {

- Page 518 and 519:

dm{f©H$ [anmoQ>© 2009-10239~r_m {

- Page 520 and 521:

dm{f©H$ [anmoQ>© 2009-10~r_m {d{Z

- Page 522 and 523:

dm{f©H$ [anmoQ>© 2009-10~r_m {d{Z

- Page 524 and 525:

dm{f©H$ [anmoQ>© 2009-10g§b¾H$

- Page 526:

dm{f©H$ [anmoQ>© 2009-105) Yeejle