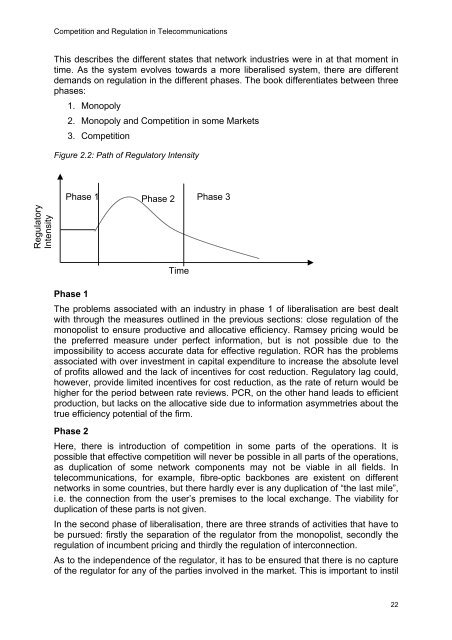

<strong>Competition</strong> <strong>and</strong> <strong>Regulation</strong> <strong>in</strong> <strong>Telecommunications</strong>This describes <strong>the</strong> different states that network <strong>in</strong>dustries were <strong>in</strong> at that moment <strong>in</strong>time. As <strong>the</strong> system evolves towards a more liberalised system, <strong>the</strong>re are differentdem<strong>and</strong>s on regulation <strong>in</strong> <strong>the</strong> different phases. The book differentiates between threephases:1. Monopoly2. Monopoly <strong>and</strong> <strong>Competition</strong> <strong>in</strong> some Markets3. <strong>Competition</strong>Figure 2.2: Path of Regulatory IntensityPhase 1 Phase 2 Phase 3RegulatoryIntensityPhase 1The problems associated with an <strong>in</strong>dustry <strong>in</strong> phase 1 of liberalisation are best dealtwith through <strong>the</strong> measures outl<strong>in</strong>ed <strong>in</strong> <strong>the</strong> previous sections: close regulation of <strong>the</strong>monopolist to ensure productive <strong>and</strong> allocative efficiency. Ramsey pric<strong>in</strong>g would be<strong>the</strong> preferred measure under perfect <strong>in</strong>formation, but is not possible due to <strong>the</strong>impossibility to access accurate data for effective regulation. ROR has <strong>the</strong> problemsassociated with over <strong>in</strong>vestment <strong>in</strong> capital expenditure to <strong>in</strong>crease <strong>the</strong> absolute levelof profits allowed <strong>and</strong> <strong>the</strong> lack of <strong>in</strong>centives for cost reduction. Regulatory lag could,however, provide limited <strong>in</strong>centives for cost reduction, as <strong>the</strong> rate of return would behigher for <strong>the</strong> period between rate reviews. PCR, on <strong>the</strong> o<strong>the</strong>r h<strong>and</strong> leads to efficientproduction, but lacks on <strong>the</strong> allocative side due to <strong>in</strong>formation asymmetries about <strong>the</strong>true efficiency potential of <strong>the</strong> firm.Phase 2TimeHere, <strong>the</strong>re is <strong>in</strong>troduction of competition <strong>in</strong> some parts of <strong>the</strong> operations. It ispossible that effective competition will never be possible <strong>in</strong> all parts of <strong>the</strong> operations,as duplication of some network components may not be viable <strong>in</strong> all fields. Intelecommunications, for example, fibre-optic backbones are existent on differentnetworks <strong>in</strong> some countries, but <strong>the</strong>re hardly ever is any duplication of “<strong>the</strong> last mile”,i.e. <strong>the</strong> connection from <strong>the</strong> user’s premises to <strong>the</strong> local exchange. The viability forduplication of <strong>the</strong>se parts is not given.In <strong>the</strong> second phase of liberalisation, <strong>the</strong>re are three str<strong>and</strong>s of activities that have tobe pursued: firstly <strong>the</strong> separation of <strong>the</strong> regulator from <strong>the</strong> monopolist, secondly <strong>the</strong>regulation of <strong>in</strong>cumbent pric<strong>in</strong>g <strong>and</strong> thirdly <strong>the</strong> regulation of <strong>in</strong>terconnection.As to <strong>the</strong> <strong>in</strong>dependence of <strong>the</strong> regulator, it has to be ensured that <strong>the</strong>re is no captureof <strong>the</strong> regulator for any of <strong>the</strong> parties <strong>in</strong>volved <strong>in</strong> <strong>the</strong> market. This is important to <strong>in</strong>stil22

<strong>Competition</strong> <strong>and</strong> <strong>Regulation</strong> <strong>in</strong> <strong>Telecommunications</strong>confidence <strong>in</strong> any companies wish<strong>in</strong>g to enter <strong>the</strong> market, provid<strong>in</strong>g <strong>the</strong>m with <strong>the</strong>certa<strong>in</strong>ty that <strong>the</strong>y will have a level play<strong>in</strong>g field.On <strong>the</strong> front of price regulation, <strong>the</strong> monopolist has <strong>the</strong> possibility to use rents frommonopoly markets to subsidise activities <strong>in</strong> <strong>the</strong> competitive markets <strong>and</strong> thus ga<strong>in</strong> anunfair advantage. The importance <strong>the</strong>refore lies <strong>in</strong> analys<strong>in</strong>g <strong>the</strong> level <strong>and</strong> structureof prices set by <strong>the</strong> monopolist.Network <strong>in</strong>dustries have a large part of <strong>the</strong>ir cost <strong>in</strong> fixed components, mak<strong>in</strong>g <strong>the</strong>allocation of costs to services very difficult <strong>and</strong> arbitrary. Considerable effort thus hasto be expended towards <strong>the</strong> analysis of <strong>the</strong> cost structure <strong>and</strong> to <strong>the</strong> development ofa “fair” level of prices to be set by <strong>the</strong> <strong>in</strong>cumbent <strong>in</strong> <strong>the</strong> competitive market.Deviations <strong>in</strong> both directions are potentially damag<strong>in</strong>g: sett<strong>in</strong>g prices too low willdiscourage entry by firms even it <strong>the</strong>y were more efficient than <strong>the</strong> <strong>in</strong>cumbent. Shouldprices be set too high, <strong>the</strong>n entrants will be able to enter even if <strong>the</strong>y are less efficientthan <strong>the</strong> <strong>in</strong>cumbent. Fur<strong>the</strong>rmore, it will jeopardise <strong>the</strong> profitability of <strong>the</strong> company<strong>and</strong> thus <strong>the</strong> cross subsidies to unprofitable market segments necessary for universalservice obligations.Even <strong>in</strong> <strong>the</strong> most competitive telecomm markets, such as Germany 4 , not all aspectsof <strong>the</strong> network have been subjected to competition, such as <strong>the</strong> last mile. There isstrong controversy about <strong>the</strong> correct level of <strong>in</strong>terconnection pric<strong>in</strong>g between <strong>the</strong>network components of Deutsche Telekom <strong>and</strong> its competitors. Once aga<strong>in</strong>, <strong>the</strong><strong>in</strong>centives of <strong>the</strong> <strong>in</strong>cumbent <strong>and</strong> competitors are opposed. If <strong>in</strong>terconnection pricesare set too high, <strong>the</strong> monopolist will receive an overly high amount for <strong>the</strong><strong>in</strong>terconnection services <strong>and</strong> thus deter entry by efficient companies. Should <strong>the</strong>prices be set too low, however, this will also attract <strong>in</strong>efficient entry. Fur<strong>the</strong>rmore, itwill discourage <strong>in</strong>vestment by <strong>the</strong> <strong>in</strong>cumbent <strong>in</strong>to new technologies, as entrantsconsequently do not carry a “fair” share of costs <strong>and</strong> risks of <strong>the</strong> <strong>in</strong>vestments <strong>and</strong>benefit disproportionately from <strong>the</strong> <strong>in</strong>cumbent’s <strong>in</strong>vestments.When <strong>in</strong>terconnect<strong>in</strong>g networks, <strong>the</strong>re are different possibilities to design accessprices:• Efficient Component Pric<strong>in</strong>g Rule (ECPR): this mechanism warrants entry aslong as <strong>the</strong> entrant is at least as efficient as <strong>the</strong> <strong>in</strong>cumbent. It is assumed thatretail prices are fixed, i.e. that allow<strong>in</strong>g <strong>the</strong> entrant access does not have aneffect on <strong>the</strong> <strong>in</strong>cumbent’s price. The cost structure is def<strong>in</strong>ed by <strong>the</strong> average<strong>in</strong>cremental cost of access, b, <strong>the</strong> average <strong>in</strong>cremental cost of provid<strong>in</strong>g <strong>the</strong>competitive part of <strong>the</strong> service, c, <strong>and</strong> <strong>the</strong> retail price of <strong>the</strong> service, p. Theoptimal access price is thus def<strong>in</strong>ed as: a = b + [ p - (b + c)]. In <strong>the</strong> context of along-distance telephone context, b would be <strong>the</strong> cost of connect<strong>in</strong>g <strong>the</strong>customer from her home to <strong>the</strong> local exchange <strong>and</strong> c <strong>the</strong> cost of rout<strong>in</strong>g <strong>the</strong>call on backbone <strong>in</strong>frastructure. The problem associated with <strong>the</strong> ECPR is <strong>the</strong>fact that allocative effects are be<strong>in</strong>g ignored, due to <strong>the</strong> assumptions of ahomogenous fixed product, a fixed coefficient of technology <strong>and</strong> <strong>the</strong> <strong>in</strong>ability ofcompetitors to bypass <strong>the</strong> <strong>in</strong>cumbent.• Ramsey access pric<strong>in</strong>g: <strong>in</strong> <strong>the</strong> spirit of optimal pric<strong>in</strong>g for society, Ramseyaccess pric<strong>in</strong>g also takes some allocative effects <strong>in</strong>to account. The formula for<strong>the</strong> calculation of <strong>the</strong> access price changes to: a = b + σ(p – (b + c)). σ is what4 Purton (2000), SURVEY - FT TELECOMMS: Former monopoly loses significant market share23