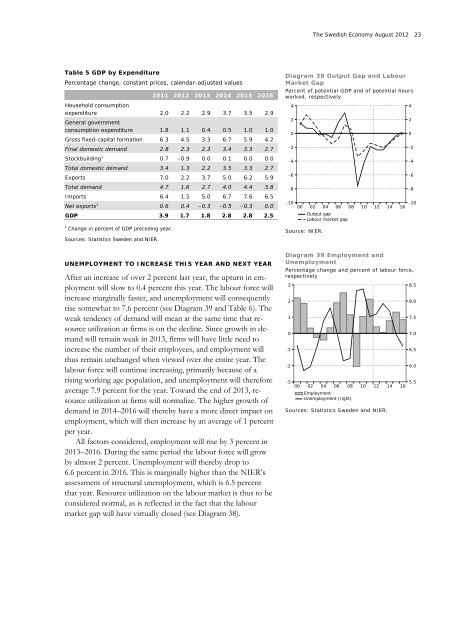

22 Macroeconomic Development and Economic Policy <strong>2012</strong>–2016Diagram 35 Household Consumptionper capitaPercentage change6420-2-4-680848892960004Sources: Statistics Sweden and NIER.Diagram 36 Gross Fixed-capitalFormationPercentage change, calendar-adjusted values105008126420-2-4-6161050consumption per capita was increasing by an average of2.0 percent per year. At the same time, however, general governmentconsumption per capita will be increasing marginallyduring the period <strong>2012</strong>–2016. This may be compared to theperiod 1995–2011, when general government consumption percapita rose by an annual average of 0.5 percent per year.In connection with the financial crisis of 2008–2009, grossfixed-capital formation dropped from 20.0 to 18.0 percent ofGDP. After a cyclical recovery in 2010 and 2011, growth in investmentwill recede to 4.5 percent this year and further to3.3 percent in 2013 (see Diagram 36). A decrease in housinginvestment will contribute to the fall-off this year. Also underlyingthe downward shift, however, are the uncertain prospects forthe economy in other countries and low capacity utilization inthe <strong>Swedish</strong> business sector. At the same time, the appreciationof the krona is contributing to downward pressure on profits inmanufacturing, another factor that is holding back investment,though with a certain time lag. In 2014 the need for capacityenhancinginvestment will nevertheless be increasing, andgrowth in investment will go up. On average, gross fixed capitalformation will increase by roughly 5.5 percent per year in 2014–2016. Its share of GDP will reach 20.0 percent in 2016, a proportionthat in the NIER’s opinion should be considered normalin a long-term perspective.-5-5-10-10-15-15-20-2000 02 04 06 08 10 12 14 16Sources: Statistics Sweden and NIER.Diagram 37 GDPPercentage change, calendar-adjusted values66442200STRONGER KRONA STIMULATING IMPORTSImports will rise modestly in <strong>2012</strong> because of the weak tendencyof demand. In 2013 growth in demand will recover. At the sametime, a stronger krona will continue to curb the development ofprices of imports. In total, this means that imports will grow by5 percent next year. In 2014–2016 growth in imports will berising further as demand accelerates. Imports will then be increasingby an average of about 7 percent per year.Net exports will be somewhat higher this year as a share ofGDP, but next year the downward trend that began in 2007 willresume (see Diagram 33). <strong>The</strong> decline will continue in 2014–2016, and in 2016 net exports will be slightly less than 5 percentas a share of GDP. Sweden’s net lending in relation to othercountries will thus continue to drop. In light of the demographictrend, with a decreasing proportion of the population in agegroups with a higher frequency of gainful employment, there isnothing remarkable about this downward trend.-2-4-600 02 04 06 08 10 12 14Sources: Statistics Sweden and NIER.16-2-4-6RECESSION NOT OVER UNTIL 2016All aspects considered, GDP growth will remain subdued in2013 at 1.8 percent (see Diagram 37 and Table 5). Growth willpick up in 2014–2016 and reach 2.5–2.8 percent per year. Eventhough recovery will then be more evident, it cannot be consideredto be very rapid, and the output gap will not close until2016 (see Diagram 38).

<strong>The</strong> <strong>Swedish</strong> <strong>Economy</strong> <strong>August</strong> <strong>2012</strong> 23Table 5 GDP by ExpenditurePercentage change, constant prices, calendar-adjusted values2011 <strong>2012</strong> 2013 2014 2015 2016Household consumptionexpenditure 2.0 2.2 2.9 3.7 3.5 2.9General governmentconsumption expenditure 1.8 1.1 0.4 0.5 1.0 1.0Gross fixed-capital formation 6.3 4.5 3.3 6.7 5.9 4.2Final domestic demand 2.8 2.3 2.3 3.4 3.3 2.7Stockbuilding 1 0.7 –0.9 0.0 0.1 0.0 0.0Total domestic demand 3.4 1.3 2.2 3.5 3.3 2.7Exports 7.0 2.2 3.7 5.0 6.2 5.9Total demand 4.7 1.6 2.7 4.0 4.4 3.8Imports 6.4 1.5 5.0 6.7 7.6 6.5Net exports 1 0.6 0.4 –0.3 –0.5 –0.3 0.0GDP 3.9 1.7 1.8 2.8 2.8 2.51Change in percent of GDP preceding year.Sources: Statistics Sweden and NIER.Diagram 38 Output Gap and LabourMarket GapPercent of potential GDP and of potential hoursworked, respectively420-2-4-6-8-100002Source: NIER.0406Output gapLabour market gap0810121416420-2-4-6-8-10UNEMPLOYMENT TO INCREASE THIS YEAR AND NEXT YEARAfter an increase of over 2 percent last year, the upturn in employmentwill slow to 0.4 percent this year. <strong>The</strong> labour force willincrease marginally faster, and unemployment will consequentlyrise somewhat to 7.6 percent (see Diagram 39 and Table 6). <strong>The</strong>weak tendency of demand will mean at the same time that resourceutilization at firms is on the decline. Since growth in demandwill remain weak in 2013, firms will have little need toincrease the number of their employees, and employment willthus remain unchanged when viewed over the entire year. <strong>The</strong>labour force will continue increasing, primarily because of arising working age population, and unemployment will thereforeaverage 7.9 percent for the year. Toward the end of 2013, resourceutilization at firms will normalize. <strong>The</strong> higher growth ofdemand in 2014–2016 will thereby have a more direct impact onemployment, which will then increase by an average of 1 percentper year.All factors considered, employment will rise by 3 percent in2013–2016. During the same period the labour force will growby almost 2 percent. Unemployment will thereby drop to6.6 percent in 2016. This is marginally higher than the NIER’sassessment of structural unemployment, which is 6.5 percentthat year. Resource utilization on the labour market is thus to beconsidered normal, as is reflected in the fact that the labourmarket gap will have virtually closed (see Diagram 38).Diagram 39 Employment andUnemploymentPercentage change and percent of labour force,respectively3210-1-2-30002040608EmploymentUnemployment (right)1012Sources: Statistics Sweden and NIER.14168.58.07.57.06.56.05.5