priced, but not delivered. When the volume in our inventories deviates from the normal position, both above and below, wehave used and will seek to use derivatives to restore the volume that is exposed to price fluctuations. These strategies aredesigned to minimize, on a short-term basis, our exposure to the risk of fluctuations in crude oil prices and refined productmargins. This hedging activity is closely managed and subject to internally established risk standards. The results of thesehedging activities are recognized in our financial statements as adjustments to cost of goods sold.Fluctuations in the price of crude oil were significant during 2008. Based on data from Platts, the price of DatedBrent crude oil was approximately $97 per barrel at the start of the year and ended at approximately $37 per barrel. In 2008,the price of Dated Brent crude oil increased significantly in the first and second quarters, peaking at approximately $144 perbarrel in the beginning of the third quarter. However, the price of Dated Brent crude oil declined significantly during thethird and fourth quarters of 2008, reaching a low of approximately $34 per barrel and ending the year at approximately $37per barrel. As of December 31, 2009, Dated Brent crude oil prices increased to approximately $78 per barrel. Dated Brentcrude oil prices increased to approximately $93 per barrel as of December 31, 2010 and further increased to $111.51 perbarrel as of June 30, 2011 as a result of outages from Libya and mounting unrest in the MENA region offset a seasonal dropin refinery runs.Our revenues and cash flows, as well as estimates of future cash flows are sensitive to changes in oil prices. Majorshifts in the cost of crude oil and the price of refined products can result in significant changes in the operating margin fromrefining operations. The prices also determine the value of our inventory.We enter into commodity derivative contracts from time to time to manage our price exposure to our inventorypositions and our purchases of crude oil in the refining process, and to fix margins on certain future production. Thecommodity derivative contracts may take the form of futures contracts or price swaps and are entered into with reputablecounter-parties. Derivative contracts are marked to market with gains and losses, realized and unrealized, recognized in costof goods sold.Hedging Activities/Hedge of InventoryWe enter into certain derivatives transactions in order to keep price risk exposure and volume exposures withinlimits set out in our risk policy, including a value-at-risk limit on total exposure of $5 million. See “—Trading Activities.”For example, if we have a long physical exposure (i.e., we have more volume priced oil than the normal position) we canoffset most of the price risk of this long physical exposure by going equally short on derivative contracts with the same (orsimilar) underlying commodity.As of December 31, 2010, we had a net long derivative position on crude oil and refined products derivativecontracts of 91,000 cubic meters (approximately 0.6 million barrels) off-setting a short physical position. The unrealizedprofit on these contracts was SEK 116.5 million as of December 31, 2010. As of December 31, 2009, we had a net shortderivative position on crude oil (excluding the extraordinary hedge of the normal inventory on crude oil) and refined productsderivative contracts of 192,000 cubic meters (approximately 1.2 million barrels), off-setting a long physical position. Theunrealized profit on these contracts as of December 31, 2009 was SEK 20.2 million. As of December 31, 2008, we had a netshort derivative position on crude oil and refined products derivative contracts of 338,000 cubic meters (approximately 2million barrels) off-setting a long physical position. The unrealized loss on these contracts was SEK 149 million as ofDecember 31, 2008.As of June 30, 2011, we had a net long position on crude oil (excluding the extraordinary hedge of the normalinventory on crude oil) and refined products derivative contracts of 64,000 cubic meters (approximately 0.4 million barrels).The unrealized profit of these contracts as of June 30, 2011 was SEK 44.9 million.Trading ActivitiesWe also enter into derivative transactions which are unrelated to physical exposure and are therefore classified as“speculative.” These transactions are monitored against profit and loss limits set out in our risk policy which do not permittrading risk greater than $0.5 million per trade. The risk amount limit for the total exposure (based on volumetric deviationfrom the normal position distributions) is set at $5 million. To measure the risk amount on our total exposure, we use a valueat-riskmodel that is updated on a daily basis. As of June 30, 2011, the total position was near zero as all positions wereclosed out but they were not yet realized.Foreign Currency RiskFrom time to time, we use forward exchange contracts and, to a lesser extent, currency options and currency swaps30

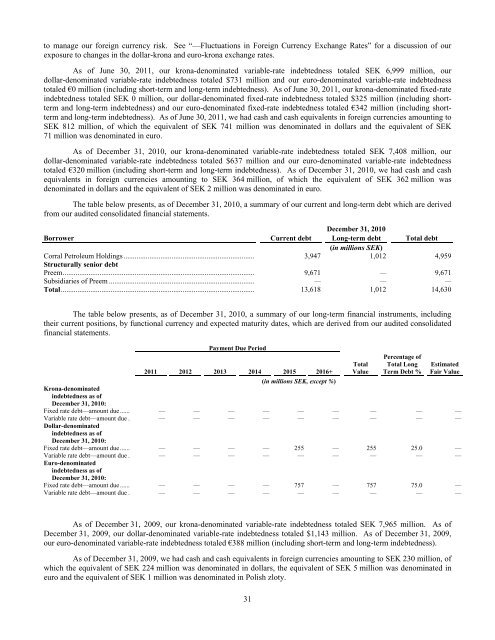

to manage our foreign currency risk. See “—Fluctuations in Foreign Currency Exchange Rates” for a discussion of ourexposure to changes in the dollar-krona and euro-krona exchange rates.As of June 30, 2011, our krona-denominated variable-rate indebtedness totaled SEK 6,999 million, ourdollar-denominated variable-rate indebtedness totaled $731 million and our euro-denominated variable-rate indebtednesstotaled €0 million (including short-term and long-term indebtedness). As of June 30, 2011, our krona-denominated fixed-rateindebtedness totaled SEK 0 million, our dollar-denominated fixed-rate indebtedness totaled $325 million (including shorttermand long-term indebtedness) and our euro-denominated fixed-rate indebtedness totaled €342 million (including shorttermand long-term indebtedness). As of June 30, 2011, we had cash and cash equivalents in foreign currencies amounting toSEK 812 million, of which the equivalent of SEK 741 million was denominated in dollars and the equivalent of SEK71 million was denominated in euro.As of December 31, 2010, our krona-denominated variable-rate indebtedness totaled SEK 7,408 million, ourdollar-denominated variable-rate indebtedness totaled $637 million and our euro-denominated variable-rate indebtednesstotaled €320 million (including short-term and long-term indebtedness). As of December 31, 2010, we had cash and cashequivalents in foreign currencies amounting to SEK 364 million, of which the equivalent of SEK 362 million wasdenominated in dollars and the equivalent of SEK 2 million was denominated in euro.The table below presents, as of December 31, 2010, a summary of our current and long-term debt which are derivedfrom our audited consolidated financial statements.December 31, 2010Borrower Current debt Long-term debt Total debt(in millions SEK)<strong>Corral</strong> <strong>Petroleum</strong> <strong>Holdings</strong> ....................................................................... 3,947 1,012 4,959Structurally senior debt<strong>Preem</strong>........................................................................................................ 9,671 — 9,671Subsidiaries of <strong>Preem</strong> ............................................................................... — — —Total......................................................................................................... 13,618 1,012 14,630The table below presents, as of December 31, 2010, a summary of our long-term financial instruments, includingtheir current positions, by functional currency and expected maturity dates, which are derived from our audited consolidatedfinancial statements.Payment Due PeriodTotalValuePercentage ofTotal LongTerm Debt %EstimatedFair Value2011 2012 2013 2014 2015 2016+(in millions SEK, except %)Krona-denominatedindebtedness as ofDecember 31, 2010:Fixed rate debt—amount due ...... — — — — — — — — —Variable rate debt—amount due . — — — — — — — — —Dollar-denominatedindebtedness as ofDecember 31, 2010:Fixed rate debt—amount due ...... — — — — 255 — 255 25.0 —Variable rate debt—amount due . — — — — — — — — —Euro-denominatedindebtedness as ofDecember 31, 2010:Fixed rate debt—amount due ...... — — — — 757 — 757 75.0 —Variable rate debt—amount due . — — — — — — — — —As of December 31, 2009, our krona-denominated variable-rate indebtedness totaled SEK 7,965 million. As ofDecember 31, 2009, our dollar-denominated variable-rate indebtedness totaled $1,143 million. As of December 31, 2009,our euro-denominated variable-rate indebtedness totaled €388 million (including short-term and long-term indebtedness).As of December 31, 2009, we had cash and cash equivalents in foreign currencies amounting to SEK 230 million, ofwhich the equivalent of SEK 224 million was denominated in dollars, the equivalent of SEK 5 million was denominated ineuro and the equivalent of SEK 1 million was denominated in Polish zloty.31