156 Toll Road Study and Appendices - Transportation Agency for ...

156 Toll Road Study and Appendices - Transportation Agency for ...

156 Toll Road Study and Appendices - Transportation Agency for ...

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

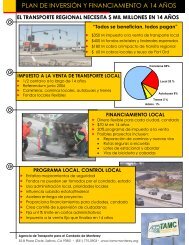

Highway <strong>156</strong> Financial Feasbility AnalysisPage 8 of 10May 10, 2013As noted in the assumptions above, the senior lien toll revenue bond financings have beenstructured with the goal of maintaining an annual debt service coverage ratio of at least 2.0x. That isto say, on an annual basis, <strong>for</strong> every dollar of senior lien bond debt service (i.e., principal <strong>and</strong>interest) that is due, there should be at least two dollars of net revenues available to pay that debtservice. This 2.0x coverage ratio is required by investors <strong>and</strong> rating agencies on toll facilities whererevenue generation is uncertain year-to-year. The US DOT is more flexible on coverage ratios <strong>and</strong>may negotiate a lower annual coverage requirement <strong>for</strong> a subordinate TIFIA loan.Presented below are the resulting coverage statistics. For each four scenarios, Phase 1 maintainshealthy debt service coverage ratios <strong>for</strong> the senior lien bonds over <strong>and</strong> above 2.0x. When the TIFIAloan debt service is factored in, the aggregate debt service coverage is maintained above 1.9x <strong>for</strong>Phase 1 in each scenario. Based upon these coverage statistics, Phase 1 is deemed financiallyfeasible.Under Scenarios B <strong>and</strong> D, when additional bond proceeds are issued <strong>for</strong> Phase 2 in 2025 <strong>and</strong> theassociated debt service is factored into the pro <strong>for</strong>ma, the coverage ratios drop below 2.0x. As maybe seen in the detailed cash flows attached, these low coverage years occur in the first five to sevenyears of after the bonds are issued. It may be the case that a portion of that debt service will beoffset with capitalized interest which will improve the senior lien coverage ratios. Further, perhaps aportion of that capacity may be issued as a TIFIA loan in 2025, which would reduce the senior lienbond requirements <strong>and</strong> improve coverage. That said, the additional bonding capacity shown <strong>for</strong>Phase 2 should be viewed as maximum capacity <strong>and</strong> subject to change based on structure <strong>and</strong>revised assumptions.Financing ResultsDebt Service Coverage StatisticsScenario: A BCDPhase: 1 1 2 1 1 2CoverageMin. Bond Coverage Ratio 3.28x 3.41x 1.57x 4.15x 4.18x 1.64xMin. Aggregate Coverage Ratio 1.92x 1.28x 2.41x 1.38xAvg. Bond Coverage Ratio 4.00x 4.90x 2.06x 5.09x 5.81x 2.10xAve. Aggregate Coverage Ratio 2.93x 2.82x 4.38x 2.48xAfter O&M costs <strong>and</strong> debt service on bonds <strong>and</strong> the TIFIA loan, there are anticipated revenuesremaining, based upon the revenue <strong>for</strong>ecasts. At this “sketch-level”, we have not funded an ongoingO&M reserve or a renewal <strong>and</strong> replacement (R&R) reserve. Also, no R&R costs are included at thistime. With subsequent analysis some of the residual revenues may be placed in reserves or used <strong>for</strong>R&R costs, as appropriate. In that context, remaining revenues after O&M costs <strong>and</strong> debt serviceare summarized below.