Do the right thing, Adviser's and creditors experience of best practice ...

Do the right thing, Adviser's and creditors experience of best practice ...

Do the right thing, Adviser's and creditors experience of best practice ...

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

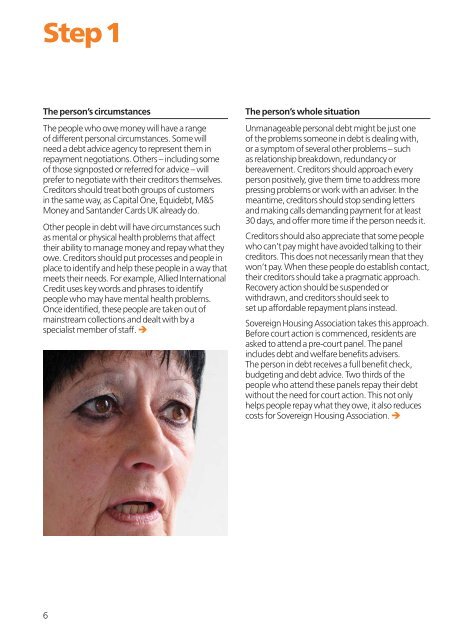

Step 1The person’s circumstancesThe people who owe money will have a range<strong>of</strong> different personal circumstances. Some willneed a debt advice agency to represent <strong>the</strong>m inrepayment negotiations. O<strong>the</strong>rs – including some<strong>of</strong> those signposted or referred for advice – willprefer to negotiate with <strong>the</strong>ir <strong>creditors</strong> <strong>the</strong>mselves.Creditors should treat both groups <strong>of</strong> customersin <strong>the</strong> same way, as Capital One, Equidebt, M&SMoney <strong>and</strong> Sant<strong>and</strong>er Cards UK already do.O<strong>the</strong>r people in debt will have circumstances suchas mental or physical health problems that affect<strong>the</strong>ir ability to manage money <strong>and</strong> repay what <strong>the</strong>yowe. Creditors should put processes <strong>and</strong> people inplace to identify <strong>and</strong> help <strong>the</strong>se people in a way thatmeets <strong>the</strong>ir needs. For example, Allied InternationalCredit uses key words <strong>and</strong> phrases to identifypeople who may have mental health problems.Once identified, <strong>the</strong>se people are taken out <strong>of</strong>mainstream collections <strong>and</strong> dealt with by aspecialist member <strong>of</strong> staff. The person’s whole situationUnmanageable personal debt might be just one<strong>of</strong> <strong>the</strong> problems someone in debt is dealing with,or a symptom <strong>of</strong> several o<strong>the</strong>r problems – suchas relationship breakdown, redundancy orbereavement. Creditors should approach everyperson positively, give <strong>the</strong>m time to address morepressing problems or work with an adviser. In <strong>the</strong>meantime, <strong>creditors</strong> should stop sending letters<strong>and</strong> making calls dem<strong>and</strong>ing payment for at least30 days, <strong>and</strong> <strong>of</strong>fer more time if <strong>the</strong> person needs it.Creditors should also appreciate that some peoplewho can’t pay might have avoided talking to <strong>the</strong>ir<strong>creditors</strong>. This does not necessarily mean that <strong>the</strong>ywon’t pay. When <strong>the</strong>se people do establish contact,<strong>the</strong>ir <strong>creditors</strong> should take a pragmatic approach.Recovery action should be suspended orwithdrawn, <strong>and</strong> <strong>creditors</strong> should seek toset up affordable repayment plans instead.Sovereign Housing Association takes this approach.Before court action is commenced, residents areasked to attend a pre-court panel. The panelincludes debt <strong>and</strong> welfare benefits advisers.The person in debt receives a full benefit check,budgeting <strong>and</strong> debt advice. Two thirds <strong>of</strong> <strong>the</strong>people who attend <strong>the</strong>se panels repay <strong>the</strong>ir debtwithout <strong>the</strong> need for court action. This not onlyhelps people repay what <strong>the</strong>y owe, it also reducescosts for Sovereign Housing Association. 6

![Annual review [ 1.4 MB] - Citizens Advice](https://img.yumpu.com/50679529/1/190x135/annual-review-14-mb-citizens-advice.jpg?quality=85)

![Help for helping your residents [ 2.4 MB] - Citizens Advice](https://img.yumpu.com/48848542/1/185x260/help-for-helping-your-residents-24-mb-citizens-advice.jpg?quality=85)