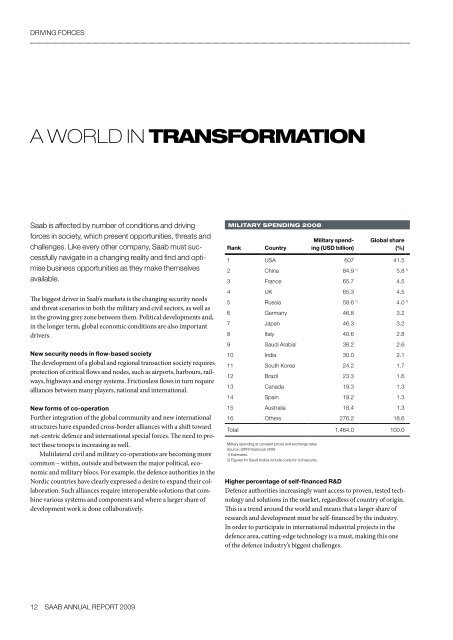

DRIVING FORCESA world in transformation<strong>Saab</strong> is affected by number of conditions and drivingforces in society, which present opportunities, threats andchallenges. Like every other company, <strong>Saab</strong> must successfullynavigate in a changing reality and find and optimisebusiness opportunities as they make themselvesavailable.The biggest driver in <strong>Saab</strong>’s markets is the changing security needsand threat scenarios in both the military and civil sectors, as well asin the growing grey zone between them. Political developments and,in the longer term, global economic conditions are also importantdrivers.New security needs in flow-based societyThe development of a global and regional transaction society requiresprotection of critical flows and nodes, such as airports, harbours, railways,highways and energy systems. Frictionless flows in turn requirealliances between many players, national and international.New forms of co-operationFurther integration of the global community and new internationalstructures have expanded cross-border alliances with a shift towardnet-centric defence and international special forces. The need to protectthese troops is increasing as well.Multilateral civil and military co-operations are becoming morecommon – within, outside and between the major political, economicand military blocs. For example, the defence authorities in theNordic countries have clearly expressed a desire to expand their collaboration.Such alliances require interoperable solutions that combinevarious systems and components and where a larger share ofdevelopment work is done collaboratively.MILITARY SPENDING 2008RankCountryMilitary spending(USD billion)Global share(%)1 USA 607 41.52 China 84.9 1) 5.8 1)3 France 65.7 4.54 UK 65.3 4.55 Russia 58.6 1) 4.0 1)6 Germany 46.8 3.27 Japan 46.3 3.28 Italy 40.6 2.89 Saudi Arabia ) 38.2 2.610 India 30.0 2.111 South Korea 24.2 1.712 Brazil 23.3 1.613 Canada 19.3 1.314 Spain 19.2 1.315 Australia 18.4 1.316 Others 276.2 18.6Total 1,464.0 100.0Military spending at constant prices and exchange ratesSource: SIPRI Yearbook <strong>2009</strong>1) Estimates.2) Figures for Saudi Arabia include costs for civil security.Higher percentage of self-financed R&DDefence authorities increasingly want access to proven, tested technologyand solutions in the market, regardless of country of origin.This is a trend around the world and means that a larger share ofresearch and development must be self-financed by the industry.In order to participate in international industrial projects in thedefence area, cutting-edge technology is a must, making this oneof the defence industry’s biggest challenges.12 saab <strong>ANNUAL</strong> <strong>REPORT</strong> <strong>2009</strong>

Partnerships between public and private playersIt is becoming more common for development projects in both themilitary and civil sectors to be carried out by so-called public-privatepartnerships (PPP). Armed forces are increasingly outsourcing theirentire training, operational and support operations. This also leadsto higher demand for training, support and maintenance. For example,<strong>Saab</strong> has a long-term contract with the Swedish Defence MaterialAdministration on an overall support commitment for the SK 60aircraft system, where as principal supplier we are responsible for theoperations, maintenance and airworthiness of its entire SK 60 fleet.Need for broad, deep, long-term solutionsAnother consequence of the continued integration is that customersin both sectors increasingly demand broad-based, integrated solutionsoften with a greater service content. A fighter like Gripen, forexample, is part of an entire air combat system that must be interoperable,i.e., work with other combat systems in the air, at sea – aboveand below the surface and on land. The trend is shifting toward fulloperational and functional commitments covering the entire lifecycle,where solutions are evaluated not only based on performance,but also in terms of the cost to own and operate the systems.Local presence can be decisiveDespite the trend toward international alliances, the need for astrong local presence is crucial to success in both the military andcivil markets. Customers want integrated solutions from companiesthat understand local conditions. This significantly increases thechances of becoming the customer’s preferred supplier and, importantly,having a portion of development costs shared by them.for years. At the same time, there is a long-term trend towardstronger alliances for peacekeeping and economic developmentpurposes, which is driving security-oriented demand.listening inIn connection with its strategic revisions in <strong>2009</strong>, <strong>Saab</strong> conducted a surveyof nearly 800 Swedish and international customers. Two-thirds of respondentsprocured from <strong>Saab</strong>.Among the most important indications in the survey were:• International customers are generally more positive about <strong>Saab</strong> – 64 percent very positive, 24 per cent fairly positive – than Swedish customers,where 11 per cent were very positive and 70 per cent fairly positive.• International customers consider <strong>Saab</strong> a modern, international companythat offers useful products and high-quality services. Swedish customersare more interested in the fact that <strong>Saab</strong> is well-known and international.• Swedish and international customers both consider <strong>Saab</strong> to be a hightechcompany with a high level of expertise. International customers alsoappreciate that <strong>Saab</strong> is honest, customer-focused, trustworthy and reliable.• The main qualities that customers are looking for in a supplier are the abilityto listen to their needs, keep their promises and deliver on time, andthat they offer value for the money.The conclusion of the survey is that <strong>Saab</strong> has the potential for improvementin many areas in order to achieve its goals, and that the there are two sidesto <strong>Saab</strong>’s image: one in Sweden and one internationally. It is clear that goingforward <strong>Saab</strong> will have to continue to focus globally on improving its productsand solutions and ensuring that they are tailored to customer needs, aswell as deliver on time, be receptive and maintain a local presence.Macroeconomic impactThe economy and its fluctuations affect the size of transaction volumesand the overall flow of goods, capital and data in the world–and thus demand for security solutions. The civil aviation market isstrongly dependent on economic development. The military market,on the other hand, has little co-variation with the global economy inthe short term. In the longer term, however, it is affected throughreduced defence budgets and delayed investments in major systems.Instead, political developments are the decisive factor globally,regionally and locally. Many of the world’s conflicts have persistedsaab <strong>ANNUAL</strong> <strong>REPORT</strong> <strong>2009</strong> 13

![Proposal long-term incentive programs [pdf] - Saab](https://img.yumpu.com/50411723/1/190x245/proposal-long-term-incentive-programs-pdf-saab.jpg?quality=85)