AUTHORISATION

U1hB302Xjd2

U1hB302Xjd2

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

SECTION I<br />

FUNDAMENTALS OF THE UBI MARKET<br />

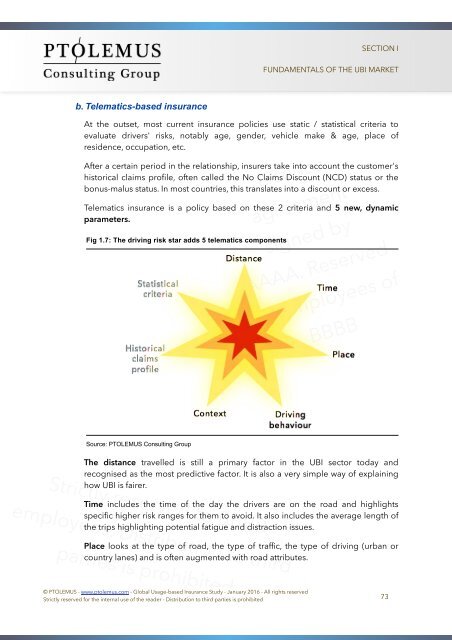

b. Telematics-based insurance<br />

At the outset, most current insurance policies use static / statistical criteria to<br />

evaluate drivers' risks, notably age, gender, vehicle make & age, place of<br />

residence, occupation, etc.<br />

After a certain period in the relationship, insurers take into account the customer's<br />

historical claims profile, often called the No Claims Discount (NCD) status or the<br />

bonus-malus status. In most countries, this translates into a discount or excess.<br />

Licence<br />

Telematics insurance is a policy based on these 2 criteria and 5 new, dynamic<br />

parameters.<br />

Fig 1.7: The driving risk star adds 5 telematics components<br />

agreement<br />

signed by<br />

AAAA. Reserved<br />

for employees of<br />

BBBB<br />

Source: PTOLEMUS Consulting Group<br />

Strictly reserved to BBBB<br />

employees. Distribution to third<br />

Time includes the time of the day the drivers are on the road and highlights<br />

specific higher risk ranges for them to avoid. It also includes the average length of<br />

the trips highlighting potential fatigue and distraction issues.<br />

The distance travelled is still a primary factor in the UBI sector today and<br />

recognised as the most predictive factor. It is also a very simple way of explaining<br />

how UBI is fairer.<br />

parties is prohibited<br />

Place looks at the type of road, the type of traffic, the type of driving (urban or<br />

country lanes) and is often augmented with road attributes.<br />

© PTOLEMUS - www.ptolemus.com - Global Usage-based Insurance Study - January 2016 - All rights reserved<br />

Strictly reserved for the internal use of the reader - Distribution to third parties is prohibited 73