CSR and Competitiveness European SMEs - KMU Forschung Austria

CSR and Competitiveness European SMEs - KMU Forschung Austria

CSR and Competitiveness European SMEs - KMU Forschung Austria

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

20 <strong>CSR</strong> <strong>and</strong> <strong>Competitiveness</strong> - <strong>European</strong> <strong>SMEs</strong>’ Good Practice - Consolidated <strong>European</strong> Report<br />

4.2 National Level<br />

Also at individual Member State level, a multitude of different (semi-)public actors is engaged in<br />

the field of <strong>CSR</strong>. This is to be attributed to the fact that <strong>CSR</strong> covers a transversal field of<br />

activities resulting in a shared responsibility of the government, the private sector (<strong>and</strong> its<br />

representative bodies) as well as the society/consumers. In the following, a systematic overview<br />

on the most important categories of different actors as well as their strategies/initiatives to foster<br />

<strong>SMEs</strong>’ engagement in <strong>CSR</strong> in the analysed countries is given. It is to be mentioned that this<br />

constitutes a set of illustrative examples rather than a comprehensive list of all involved entities.<br />

A schematic summary of key actors <strong>and</strong> their strategies presented in the next sections can be<br />

found below:<br />

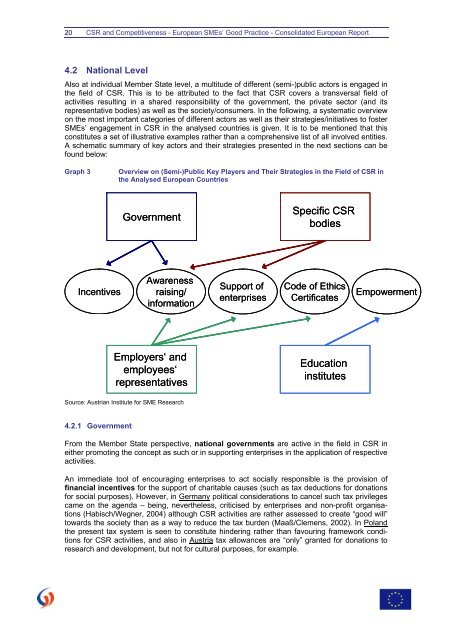

Graph 3 Overview on (Semi-)Public Key Players <strong>and</strong> Their Strategies in the Field of <strong>CSR</strong> in<br />

the Analysed <strong>European</strong> Countries<br />

Incentives<br />

Government<br />

Awareness<br />

raising/<br />

information<br />

Employers‘ <strong>and</strong><br />

employees‘<br />

representatives<br />

Source: <strong>Austria</strong>n Institute for SME Research<br />

4.2.1 Government<br />

Support of<br />

enterprises<br />

Specific <strong>CSR</strong><br />

bodies<br />

Code of Ethics<br />

Certificates<br />

Education<br />

institutes<br />

Empowerment<br />

From the Member State perspective, national governments are active in the field in <strong>CSR</strong> in<br />

either promoting the concept as such or in supporting enterprises in the application of respective<br />

activities.<br />

An immediate tool of encouraging enterprises to act socially responsible is the provision of<br />

financial incentives for the support of charitable causes (such as tax deductions for donations<br />

for social purposes). However, in Germany political considerations to cancel such tax privileges<br />

came on the agenda – being, nevertheless, criticised by enterprises <strong>and</strong> non-profit organisations<br />

(Habisch/Wegner, 2004) although <strong>CSR</strong> activities are rather assessed to create “good will”<br />

towards the society than as a way to reduce the tax burden (Maaß/Clemens, 2002). In Pol<strong>and</strong><br />

the present tax system is seen to constitute hindering rather than favouring framework conditions<br />

for <strong>CSR</strong> activities, <strong>and</strong> also in <strong>Austria</strong> tax allowances are “only” granted for donations to<br />

research <strong>and</strong> development, but not for cultural purposes, for example.