quarterly-insurtech-briefing-q4-2017

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Incumbent InsurTech Strategy<br />

(Re)insurance Innovation Survey<br />

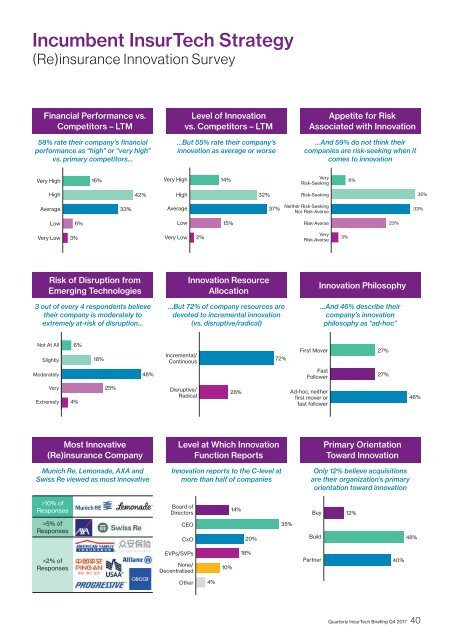

Financial Performance vs.<br />

Competitors – LTM<br />

58% rate their company’s financial<br />

performance as “high” or “very high”<br />

vs. primary competitors…<br />

Level of Innovation<br />

vs. Competitors – LTM<br />

…But 55% rate their company’s<br />

innovation as average or worse<br />

Appetite for Risk<br />

Associated with Innovation<br />

…And 59% do not think their<br />

companies are risk-seeking when it<br />

comes to innovation<br />

Very High<br />

16%<br />

Very High<br />

14%<br />

Very<br />

Risk-Seeking<br />

6%<br />

High<br />

42%<br />

High<br />

32%<br />

Risk-Seeking<br />

35%<br />

Average<br />

33%<br />

Average<br />

37%<br />

Neither Risk-Seeking<br />

Nor Risk-Averse<br />

33%<br />

Low<br />

6%<br />

Low<br />

15%<br />

Risk-Averse<br />

23%<br />

Very Low<br />

3%<br />

Very Low<br />

2%<br />

Very<br />

Risk-Averse<br />

3%<br />

Risk of Disruption from<br />

Emerging Technologies<br />

3 out of every 4 respondents believe<br />

their company is moderately to<br />

extremely at-risk of disruption…<br />

Innovation Resource<br />

Allocation<br />

…But 72% of company resources are<br />

devoted to incremental innovation<br />

(vs. disruptive/radical)<br />

Innovation Philosophy<br />

…And 46% describe their<br />

company’s innovation<br />

philosophy as “ad-hoc”<br />

Not At All<br />

Slightly<br />

6%<br />

18%<br />

Incremental/<br />

Continuous<br />

72%<br />

First Mover<br />

27%<br />

Moderately<br />

48%<br />

Fast<br />

Follower<br />

27%<br />

Very<br />

Extremely<br />

4%<br />

25%<br />

Disruptive/<br />

Radical<br />

28%<br />

Ad-hoc, neither<br />

first mover or<br />

fast follower<br />

46%<br />

Most Innovative<br />

(Re)insurance Company<br />

Munich Re, Lemonade, AXA and<br />

Swiss Re viewed as most innovative<br />

Level at Which Innovation<br />

Function Reports<br />

Innovation reports to the C-level at<br />

more than half of companies<br />

Primary Orientation<br />

Toward Innovation<br />

Only 12% believe acquisitions<br />

are their organization’s primary<br />

orientation toward innovation<br />

>10% of<br />

Responses<br />

Board of<br />

Directors<br />

14%<br />

Buy<br />

12%<br />

>5% of<br />

Responses<br />

CEO<br />

CxO<br />

20%<br />

35%<br />

Build<br />

48%<br />

>2% of<br />

Responses<br />

EVPs/SVPs<br />

None/<br />

Decentralized<br />

10%<br />

18%<br />

Partner<br />

40%<br />

Other<br />

4%<br />

Quarterly InsurTech Briefing Q4 <strong>2017</strong> 40