Jeweller - December 2020

• Survival lessons: Essential business tips learned from a year of upheaval • Full state of play: a comprehensive report into the Australian jewellery industry in 2020 • Show stoppers: standout jewellery pieces from local talents

• Survival lessons: Essential business tips learned from a year of upheaval

• Full state of play: a comprehensive report into the Australian jewellery industry in 2020

• Show stoppers: standout jewellery pieces from local talents

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

VOICE OF THE AUSTRALIAN JEWELLERY INDUSTRY DECEMBER <strong>2020</strong><br />

Survival lessons<br />

ESSENTIAL BUSINESS TIPS LEARNED<br />

FROM A YEAR OF UPHEAVAL<br />

Full state of play<br />

A COMPREHENSIVE REPORT INTO THE<br />

AUSTRALIAN JEWELLERY INDUSTRY IN <strong>2020</strong><br />

Show stoppers<br />

STANDOUT JEWELLERY PIECES<br />

FROM LOCAL TALENTS

#1<br />

FOLLOW THE<br />

LEADER<br />

Reader<br />

PUBLICATION<br />

GLOBAL<br />

RANKING<br />

TIME SPENT<br />

PER VISITOR<br />

1 JCK 80,897 1:58 USA<br />

COUNTRY<br />

There are many ways to measure #1, however; when<br />

it comes to media, there’s only one way... readership.<br />

2 <strong>Jeweller</strong> 89,405 32:07 Australia<br />

3 National <strong>Jeweller</strong> 143,232 1:58 USA<br />

4<br />

Instore Magazine 175,059 2:09 USA<br />

5 Rapaport Magazine* 193,212 1:51 USA<br />

6 Idex* 259,946 2:44 Israel<br />

7 <strong>Jeweller</strong>y Net Asia 325,766 2:33 Hong Kong<br />

8 Professional <strong>Jeweller</strong> 413,298 1:48 UK<br />

9 The Jewelry Magazine 501,729 1:09 India<br />

10 Diamond World* 629,210 1:59 India<br />

Not only is <strong>Jeweller</strong> the #1 magazine in Australia<br />

and New Zealand by far, we are now ranked #2 in<br />

the world by Alexa, the global ranking system for<br />

analysing website readership.<br />

Yes, your own <strong>Jeweller</strong> is now ranked the second<br />

most widely read industry publication in the world,<br />

just behind the US’s JCK magazine.<br />

Better still, according to Alexa, the daily time spent<br />

on jewellermagazine.com averages 30 minutes,<br />

which far exceeds all is other business-to-business<br />

titles which average between 2–3 minutes per visitor.<br />

At the same time, <strong>Jeweller</strong>’s social media presence<br />

dominates and our eMags boast 12 million reads.<br />

It’s our commitment to excellence in reporting, high<br />

quality presentation, and reader engagement that sets<br />

us apart, which is why we say: Follow the Reader!<br />

* Alexa Global Ranking statistics as at 22 November <strong>2020</strong><br />

* Denotes magazines connected to diamond trading platforms<br />

VOICE OF THE AUSTRALIAN JEWELLERY INDUSTRY

Australian Argyle pink diamonds are beyond rare and amongst the most precious diamonds in the world.<br />

Pink Kimberley jewellery is crafted from an exquisite blend of white diamonds and<br />

natural Australian pink diamonds from the Argyle Diamond Mine, located in the East<br />

Kimberley region of Western Australia. A coveted Argyle pink diamond Certificate<br />

accompanies all Pink Kimberley pieces containing pink diamonds greater than 0.08ct.<br />

PinkKimberley.com.au

Access one of the largest inventories of<br />

Argyle pink diamonds in Australia<br />

TENDER STONES | SINGLE STONES | MATCHED PAIRS | CALIBRATED MELEE LINES<br />

SAMS GROUP<br />

E pink@samsgroup.com.au W samsgroup.com.au P 02 9290 2199<br />

AUSTRALIA

Baumatic self-winding calibre, 40mm steel case<br />

baume-et-mercier.com<br />

Proudly distributed by<br />

(02) 9417 0177 | www.dgau.com.au

Discover the new Christmas Collection from 29 th October <strong>2020</strong><br />

Available in Pandora concept stores, participating stockists and pandora.net

DECEMBER <strong>2020</strong><br />

Contents<br />

This Month<br />

Industry Facets<br />

13 Editor’s Desk<br />

18 Upfront<br />

20 News<br />

32 <strong>Jeweller</strong>s Showcase<br />

24<br />

27<br />

28<br />

31<br />

64<br />

66<br />

10 YEARS AGO<br />

Time Machine: <strong>December</strong> 2010<br />

NOW & THEN<br />

Fairfax & Roberts<br />

MY STORE<br />

Rohan <strong>Jeweller</strong>s<br />

LEARN ABOUT GEMS<br />

Lapis lazuli<br />

MY BENCH<br />

Leon Raper<br />

SOAPBOX<br />

John Rose<br />

35 STATE OF THE INDUSTRY REPORT<br />

The full picture<br />

<strong>Jeweller</strong> explores the evolution of<br />

the watch and jewellery industry<br />

over the past 10 years.<br />

CHAIN STORES<br />

The demise of fashion jewellery chains<br />

Fine jewellery demonstrates unexpected resilience<br />

Mid-sized jewellery chains have mixed results<br />

<strong>2020</strong> State of the Industry Report<br />

37<br />

46<br />

52<br />

PART I: CHAIN STORES<br />

Chain reactions<br />

PART II: BRAND-ONLY STORES<br />

Brand and deliver<br />

PART III: BUYING GROUPS<br />

Strength in numbers<br />

Better Your Business<br />

BRAND-ONLY STORES<br />

Huge increase in brand-only stores over past decade<br />

International luxury groups make their mark<br />

BUYING GROUPS<br />

Shake up for the buying groups in <strong>2020</strong><br />

How will they fare in the future?<br />

58<br />

60<br />

61<br />

62<br />

63<br />

BUSINESS STRATEGY<br />

SUE BARRETT reflects on the lessons of <strong>2020</strong> for business owners.<br />

SELLING<br />

RICH KIZER and GEORGANNE BENDER share six top tips for boosting sales.<br />

MANAGEMENT<br />

It’s time to organise your thinking for 2021, writes DAVID BROWN.<br />

MARKETING & PR<br />

WILLIAM COMCOWICH advises on how to determine your campaign’s success.<br />

LOGGED ON<br />

Instagram Stories require preparation and planning, writes SIMON DELL.<br />

31 LEARN ABOUT GEMS<br />

Lapis lazuli<br />

4Explore the enduring appeal<br />

and fascinating history of<br />

this deep blue mineral.<br />

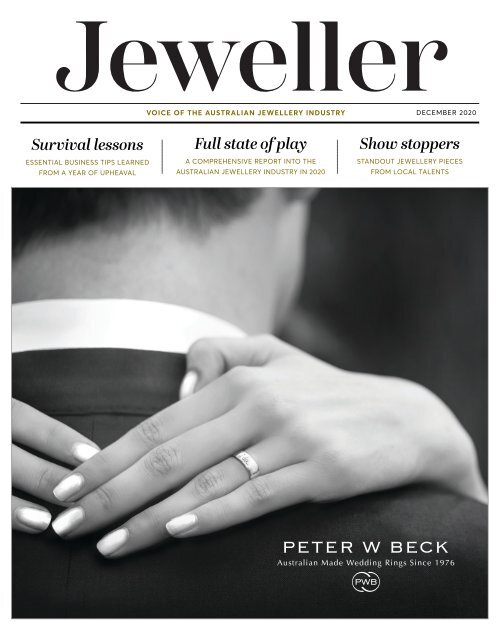

FRONT COVER Peter W Beck is<br />

synonymous with wedding rings<br />

of the highest quality, combining<br />

expert craftsmanship with the<br />

finest materials to create.<br />

<strong>December</strong> <strong>2020</strong> | 11

Every holiday season is vital to your<br />

business, and this year, success has<br />

a new level of importance.<br />

As you meet the demands of this<br />

busy season, Stuller is ready to help<br />

with our robust in-stock inventory.<br />

Visit Stuller.com/Holiday.<br />

Items featured, left to right: 87325 and 124536<br />

Stuller.com<br />

+1 337-262-7700

Editor’s Desk<br />

Listening to the heartbeat of the jewellery trade<br />

What happens when the Australian jewellery industry undergoes an intense medical examination?<br />

ANGELA HAN checks the vitals and shares her findings.<br />

Every word that could describe the global<br />

pandemic has already been written.<br />

The events of <strong>2020</strong> will be recorded in<br />

history’s pages as a central turning point in<br />

the way we view the world and the things<br />

that we value.<br />

Undoubtedly, it’s been an extraordinary year,<br />

one that deserves introspection and analysis<br />

as it draws to an end.<br />

If you wanted to know what the Australian<br />

jewellery industry looks like today in the midst<br />

of an economic crisis, then you’re in luck.<br />

By sheer coincidence, this month is the<br />

10-year anniversary of our 2010 State of<br />

the Industry Report (SOTIR). In a way, this<br />

<strong>2020</strong> update happens to be our contribution<br />

to the pages of history.<br />

A decade ago <strong>Jeweller</strong> researched and<br />

compiled the first-ever comprehensive<br />

analysis of the Australian jewellery industry;<br />

we analysed the core segments of the trade<br />

from fashion and fine jewellery stores to<br />

chain and brand-only and flagship stores.<br />

It was an exhaustive investigation into<br />

the status and health of the trade, which<br />

revealed some very interesting insights.<br />

Much like a medical examination, data was<br />

meticulously recorded and every aspect of<br />

the industry was analysed in-depth.<br />

Indeed, some of the findings of the<br />

2010 report flew in the face of what was<br />

considered conventional wisdom or<br />

common knowledge about Australia’s<br />

retail jewellery market.<br />

In other words, a lot of what was believed<br />

was wrong or, at least, not supported by the<br />

research. Debunking ‘conventional wisdom’<br />

is part of the media’s role.<br />

While our <strong>2020</strong> State of the Industry Report<br />

reviews many aspects of the market, at the<br />

beginning of this year it was our intention<br />

to include an analysis of the most important<br />

industry category - independent jewellery<br />

stores.<br />

However, the COVID pandemic not only<br />

dramatically affected our ability to undertake<br />

the research but, more importantly, the<br />

resulting economic crisis could, and has,<br />

had a major impact on jewellery stores to<br />

the extent that some have closed.<br />

For that reason, we decided to research<br />

and quantify the number of independent<br />

jewellers after the <strong>2020</strong> Christmas trading<br />

period to better compare the results.<br />

As you will discover, our <strong>2020</strong> SOTIR reveals<br />

that fine jewellery chains have remained<br />

resilient over the ensuing 10 years.<br />

In 2010 we reported on the rise of fashion<br />

jewellery chains, however, a decade later<br />

they are all but gone.<br />

While 63 per cent of fashion jewellery chain<br />

stores closed, there was only a 13 per cent<br />

reduction in the number of fine jewellery<br />

chain stores.<br />

In fact, of the seven fashion chains that<br />

existed in 2010, we discover today that six<br />

have collapsed and/or closed their doors!<br />

While the past decade has resulted in the<br />

demise of fashion jewellery chains, back<br />

in 2010, we identified 128 brand-only and<br />

flagship stores, however today there are<br />

220 - a 72 per cent increase in presence.<br />

What we found surprising is the number<br />

of high-end ‘prestige’ brands that have<br />

expanded into Australia courtesy of<br />

international luxury good conglomerates.<br />

The Australian jewellery industry in 2010<br />

was beginning to recover from the global<br />

financial crisis (GFC), which hit the world<br />

from 2007-2009.<br />

Interestingly, CommSec’s 2010 Economic<br />

Insights report announced that the sales of<br />

jewellery, watches, and clocks rose 10.3 per<br />

cent, while spending across other industries<br />

decreased during the same period.<br />

Spending on tools and equipment was down<br />

6.7 per cent, while air travel (4.4), gambling<br />

(2.5) and cigarettes (0.8) all suffered.<br />

Even spending on essential goods and<br />

services was down against jewellery!<br />

A decade later in the midst of a global<br />

pandemic, LVMH stock prices have reached<br />

its highest trade ever at 496.90 EUR since<br />

it first listed on the stock exchange in 1990,<br />

while Pandora and Tiffany stock prices also<br />

continue to soar.<br />

Hong Kong retailer Chow Tai Fook is<br />

trading better than this time last year<br />

and both Michael Hill International and the<br />

The <strong>2020</strong> State<br />

of the Industry<br />

Report update<br />

happens to be<br />

our contribution<br />

to the pages of<br />

history.<br />

US chain, Signet Jewelers, are steadily<br />

recovering since the huge sell off in the<br />

depths of the crisis.<br />

On home soil, jewellery management<br />

consultancy firm Retail Edge released<br />

positive reports of increased sales across<br />

its 450 customers in Australia and NZ.<br />

Reports released since June indicate<br />

that sales have been bouyant despite<br />

the pandemic.<br />

Indeed, there was a 23 per cent increase<br />

in September sales compared to last<br />

year, despite Victoria remaining in Stage 4<br />

lockdown. October’s report indicates that<br />

sales were also up 20 per cent, revealing a<br />

positive growth trend which is predicted to<br />

continue through the holiday trading.<br />

In amidst the chaos, a pattern appears<br />

to be emerging.<br />

Like discovering a speck of gold at the<br />

bottom of a murky pan, turbulent times<br />

appear to be an opportunity for jewellers<br />

who confront challenges with open eyes<br />

and a positive attitude.<br />

What is fast is fleeting, but what is<br />

meaningful can last forever.<br />

Humans will always yearn to be<br />

surrounded by things that are expressive,<br />

beautiful and unchanging, a sentiment that<br />

appears to be magnified during times of<br />

uncertainty.<br />

Be it through an economic crisis or<br />

through a pandemic, people don’t stop<br />

creating memories, celebrating milestones<br />

and falling in love.<br />

A glance back at the past decade has<br />

revealed this insight: consumers have<br />

chosen jewellery, through times both<br />

thick and thin. As long as there is a deep<br />

human experience to celebrate, there will<br />

always be a purpose for jewellers.<br />

To ensure you remain up to date with these<br />

insights and research reports, subscribe<br />

to our eNewseletter and connect with us<br />

to keep track of vitals and listen to the<br />

heartbeat of the industry.<br />

Angela Han<br />

Publisher<br />

<strong>December</strong> <strong>2020</strong> | 13

#ONEFORMEONEFORYOU<br />

C O M P O S A B L E , C R E A T E Y O U R B R A C E L E T L I N K B Y L I N K<br />

Timesupply<br />

jewellery + watches<br />

p +61 (0)8 8221 5580<br />

sales@timesupply.com.au | timesupply.com.au<br />

exclusive distributor AU & NZ

Proudly distributed by<br />

02 9417 0177 | www.dgau.com.au

Upfront<br />

#Instagram hashtags to follow<br />

Alpha Order<br />

#blackopal<br />

383,157+ POSTS<br />

#dreamring<br />

152,666+ POSTS<br />

#minimalistjewelry<br />

333,526+ POSTS<br />

#morganite<br />

193,583+ POSTS<br />

Stranger Things<br />

Weird, wacky and wonderful<br />

jewellery news from around the world<br />

‘Green’ diamonds<br />

#fancydiamonds<br />

48,961+ POSTS<br />

#gemlover<br />

126,476+ POSTS<br />

#jewellerystyle<br />

37,848+ POSTS<br />

#necklaces<br />

5.2 MILLION POSTS<br />

#tanzanite<br />

411,402+ POSTS<br />

#whitegold<br />

2 MILLION POSTS<br />

HISTORIC GEMSTONE<br />

Mogul Mughal Emerald<br />

Weighing 217.80 carats, the Mogul Mughal is one of the world’s largest emeralds.<br />

Originally mined in Colombia, it was likely transported to India by Spanish traders.<br />

Carved with a Shi’a Muslim prayer, the gemstone bears the date ‘1107 AH’ (1695–1696<br />

CE), dating it to the reign of the last great Mughal emperor, Aurangzeb. Scholars<br />

believe it belonged to one of his courtiers. US mineralogist Alan Caplan acquired the<br />

emerald some time in the 20th Century; after his death, it was sold by Christie’s in<br />

2001 for £1.5 million. Today, it is part of the Museum of Islamic Art in Doha, Qatar.<br />

Celebrity Style<br />

4 Actress Tracee Ellis Ross (inset)<br />

showed off her impeccable jewellery<br />

taste at the People’s Choice Awards,<br />

donning a gorgeous set of statement<br />

earrings from Schiaparelli (above).<br />

Inspired by the surrealist art of Jean<br />

Cocteau, the chandelier set features<br />

brass, crystal, and pearl.<br />

4UK clean energy entrepreneur<br />

Dale Vince claims to have created<br />

the first ‘zero-impact’ lab-grown<br />

diamonds. The stones are created<br />

in factories powered by wind and<br />

solar energy, using carbon captured<br />

from the atmosphere. “Making<br />

diamonds from nothing more than<br />

the sky, from the air we breathe, is a<br />

magical, evocative idea – it’s modern<br />

alchemy,” Vince said. “We don’t need<br />

to mine the Earth to have diamonds,<br />

we can mine the sky.”<br />

Ear’s the thing<br />

4US jeweller Jules Kim has<br />

launched jewellery designed to be<br />

slipped onto wireless earphones,<br />

also known as ‘ear pods’. Kim was<br />

inspired by watching athletes<br />

training in New York City. “These<br />

pieces reflect... the future of<br />

jewellery style,” he said. The hoops<br />

and studs are available in 14-carat<br />

white or yellow gold and in silver<br />

and gold vermeil, with 2-carat<br />

diamonds.<br />

Digital Brainwave<br />

The One Small<br />

Step program<br />

also includes<br />

practical guides<br />

to digital tools,<br />

as well as a free<br />

consultation with<br />

Navii Digital.<br />

4Australian technology start-up Navii<br />

Digital is offering a free program called One<br />

Small Step to assist SMEs in adapting to<br />

the digital environment. It includes a series<br />

of webinars featuring representatives from<br />

companies like Facebook and Xero, as well<br />

as SME owners discussing their experiences<br />

with digital marketing and e-commerce.<br />

Liz Ward, founder Navii Digital, said,<br />

“Small businesses tell us they need to see<br />

businesses like theirs, and the benefits and<br />

the costs associated with digital tools before<br />

they adopt them.”<br />

Top Product<br />

4The Pink Kimberley Classic<br />

Collection showcases shimmering<br />

halo and double halo designs set<br />

with stunning pink diamonds from<br />

the iconic Argyle Mine.<br />

Thieves exposed<br />

4UK police have busted a ring<br />

of thieves responsible for a spate<br />

of high-profile celebrity burglaries<br />

after a Romanian call girl posed with<br />

a stolen necklace in a social media<br />

photo. The gang raided the London<br />

homes of billionaire heiress Tamara<br />

Ecclestone and Chelsea FC manager<br />

Frank Lampard, stealing jewellery<br />

and cash valued at £25 million. The<br />

Mirror newspaper reports that<br />

the call girl was part of the gang’s<br />

‘supporting cast’.<br />

VOICE OF THE AUSTRALIAN JEWELLERY INDUSTRY<br />

Published by Befindan Media Pty Ltd<br />

Locked Bag 26, South Melbourne, VIC 3205 AUSTRALIA | ABN 66 638 077 648 | Phone: +61 3 9696 7200 | Subscriptions & Enquiries: info@jewellermagazine.com<br />

Publisher & Managing Editor Angela Han angela.han@jewellermagazine.com • Assistant Editor Arabella Roden arabella.roden@jewellermagazine.com<br />

Digital Co-ordinator Trish Bucheli-Preece trish@jewellermagazine.com • Advertising Toli Podolak toli.podolak@jewellermagazine.com • Accounts Paul Blewitt finance@befindanmedia.com<br />

Copyright All material appearing in <strong>Jeweller</strong> is subject to copyright. Reproduction in whole or in part is strictly forbidden without prior written consent of the publisher. Befindan Media Pty Ltd<br />

strives to report accurately and fairly and it is our policy to correct significant errors of fact and misleading statements in the next available issue. All statements made, although based on information<br />

believed to be reliable and accurate at the time, cannot be guaranteed and no fault or liability can be accepted for error or omission. Any comment relating to subjective opinions should be addressed to<br />

the editor. Advertising The publisher reserves the right to omit or alter any advertisement to comply with Australian law and the advertiser agrees to indemnify the publisher for all damages or liabilities<br />

arising from the published material.

Ethical Colombian Emeralds<br />

direct from the mines to you.<br />

Bringing you the highest-grade, ethically-mined Colombian emeralds<br />

straight from the world’s most recognised mines into your hands.<br />

Dedicated to traceability, quality and reliability, our emeralds<br />

are certified and ready to be set into unique pieces or purchased<br />

as an investment. From uncut roughs and perfectly cut loose stones<br />

to one-of-a-kind preset jewellery and custom-makes,<br />

Colonial Gemstones is at your service.<br />

Mauro<br />

MAURO CARVAJAL<br />

COMPANY DIRECTOR<br />

+61 3 4373 4281<br />

contact@colonialgemstones.com<br />

www.colonialgemstones.com

News<br />

In Brief<br />

End of an era: Argyle Mine officially closed<br />

Russian pink diamond<br />

sold for $27 million<br />

4 The Spirit of the Rose – the largest-ever<br />

vivid purplish-pink diamond to appear at<br />

auction – has sold for $US26.6 million at a<br />

Sotheby’s event in Geneva. The 14.83-carat<br />

stone, mined by Alrosa in Russia, is<br />

internally flawless and was named after a<br />

famous ballet. An anonymous telephone<br />

bidder won the auction, paying the highestever<br />

price per carat for a purple-pink<br />

diamond, according to Sotheby’s.<br />

Man jailed for $3 million<br />

Melbourne robbery<br />

4Karl Kachami, one of two men who<br />

pleaded guilty in relation to the April<br />

armed robbery of a Melbourne gold<br />

dealer, has been sentenced to four years<br />

in prison, with eligibility for parole in<br />

two years. Kachami, 48, planned the<br />

robbery with an employee of the dealer<br />

and believed it was a “victimless crime”.<br />

He made off with more than $3 million<br />

in cash, jewellery and bullion.<br />

Thieves detained over<br />

Green Vaults heist<br />

4Three people have been arrested in<br />

Berlin in relation to the theft of priceless<br />

jewellery from Dresden Castle’s Green<br />

Vault, a year after the crime took<br />

place. The museum – which is home to<br />

the Dresden Green, one of the world’s<br />

largest green diamonds – was burgled in<br />

the early morning of 25 November 2019<br />

after a small fire at an electricity junction<br />

box caused a power failure.<br />

New national sales<br />

manager at Peter W Beck<br />

4Peter W Beck has appointed<br />

Greville Ingham to the newly-created<br />

role of national sales manager, working<br />

across both retail and precious metal<br />

services divisions of the business.<br />

The role encompasses both Australia<br />

and New Zealand. Ingham was previously<br />

precious metal services manager at<br />

Peter W Beck between 1992 and 2000,<br />

and is a member of the Beck family. He<br />

commenced his new role on 2 November.<br />

An aerial view of the Argyle Mine – the world’s premier source of pink diamonds – which ceased production on<br />

3 November after 37 years of operation.<br />

The source of more than 90 per cent of the<br />

world’s pink diamonds, the Argyle Mine in the<br />

Kimberley region of Western Australia, has<br />

been permanently closed by owner Rio Tinto<br />

after more than 30 years<br />

of operation.<br />

The mine’s last day of operation was 3<br />

November, with employees and traditional<br />

owners of the land attending an event to mark<br />

the start of the closure process.<br />

Rio Tinto estimates it will take five years to<br />

dismantle and decommission the Argyle site,<br />

which will be rehabilitated, monitored, and<br />

returned to traditional owners.<br />

Andrew Wilson, general manager of the Argyle<br />

Mine, said, “This is an historic day for the<br />

Argyle Mine and the east Kimberley region,<br />

and a great source of pride for this unique<br />

Australian success story.<br />

“A new chapter will now begin as we start the<br />

process of respectfully closing the Argyle mine<br />

and rehabilitating the land, to be handed back<br />

to its traditional custodians.”<br />

Diamonds were discovered in the region in<br />

1979, with alluvial operations commencing<br />

four years later.<br />

Open pit mining began in 1985, and the Argyle<br />

site was transitioned to a fully underground<br />

operation in 2013 as its diamond reserves<br />

began to be exhausted.<br />

Over its period of operation, the mine has<br />

produced more than 865 million carats of<br />

rough diamonds and is the world’s largest<br />

producer of natural fancy colour diamonds.<br />

The annual Argyle Tender of colour diamonds<br />

began with a 33-stone viewing in Antwerp in<br />

1984, and has since evolved into a staple of<br />

the diamond-buying calendar that captivates<br />

industry figures and consumers alike.<br />

“A new chapter will now begin as we<br />

start the process of respectfully closing<br />

the Argyle Mine and rehabilitating<br />

the land, to be handed back to its<br />

traditional custodians”<br />

ANDREW WILSON<br />

Argyle Mine<br />

Arnaud Soirat, chief executive – copper and<br />

diamonds at Rio Tinto, said, “50 years ago<br />

there were very few people who believed<br />

there were diamonds in Australia – even<br />

fewer could have foreseen how the Argyle<br />

story would unfold.<br />

To arrive at this final chapter has required<br />

vision, courage and determination to overcome<br />

significant challenges to enter new territory in<br />

diamond exploration, mining and marketing.”<br />

He added, “Today Argyle’s influence stretches<br />

into many spheres and over many continents<br />

and I am very proud to acknowledge all<br />

those people who have contributed to the<br />

discovery and development of the mine and the<br />

production of some of the finest diamonds the<br />

world has ever seen.”<br />

Bids for the penultimate Tender, ‘One Lifetime,<br />

One Encounter’, closed on 2 <strong>December</strong>.<br />

20 | <strong>December</strong> <strong>2020</strong>

Louis Vuitton purchases a second large<br />

diamond mined in Botswana<br />

Perfect fit<br />

Speciality jewellers<br />

insurance solutions designed<br />

to match your business<br />

The 549-carat Sethunya diamond has been acquired by Louis Vuitton and will be cut by HB Antwerp.<br />

Image credit: Louis Vuitton<br />

French fashion house Louis Vuitton has acquired<br />

a 549-carat stone unearthed at the Karowe Mine<br />

in Botswana – 10 months after purchasing the<br />

1,758-carat Sewelô diamond, which was mined<br />

at the same site.<br />

The new diamond has been named Sethunya,<br />

which means ‘flower’ in the Setswana language.<br />

It was discovered in February <strong>2020</strong>, a month<br />

after Louis Vuitton acquired the Sewelô, which is<br />

the largest diamond found in Botswana to date.<br />

Both stones were mined by Canada’s Lucara<br />

Diamond Corporation (Lucara).<br />

As part of the deal, the Sethunya diamond will<br />

be cut by HB Antwerp in collaboration with<br />

Louis Vuitton in order to create a personalised<br />

jewellery set for a customer.<br />

A statement from Lucara explained, “Louis<br />

Vuitton envisages crafting beautiful, bespoke<br />

high-value polished stones of variable size<br />

and shape fashioned from this rare specimen<br />

to the client’s wishes: the ultimate personalised<br />

high jewellery experience and the opportunity to<br />

create a truly unique gem, a storied<br />

family heirloom.<br />

“In this way, the client will be involved in the<br />

creative process of plotting, cutting, polishing,<br />

and becoming part of the story that the stone will<br />

carry with it into history.”<br />

Eira Thomas, CEO Lucara, said the company<br />

was “extremely pleased to be building on the<br />

ground-breaking partnership established for the<br />

manufacturing of the Sewelô earlier this year”.<br />

Following the Sethunya sale announcement,<br />

Lucara confirmed it had found another<br />

remarkable diamond – a 998-carat rough – at<br />

Karowe. That stone will be sold directly to HB<br />

Antwerp as part of an overall deal to acquire all<br />

Lucara diamonds above 10.8 carats.<br />

“Lucara is extremely pleased with the continued<br />

recovery of large, high-quality diamonds from<br />

the south lobe of the Karowe mine.<br />

“To recover two [500-carat-plus] diamonds<br />

in 10 months, along with the many other<br />

high-quality diamonds across all the size<br />

ranges, is a testament to the unique aspect<br />

of the resource at Karowe”<br />

EIRA THOMAS<br />

Lucara Diamond Corporation<br />

“To recover two [500-carat-plus] diamonds in<br />

10 months, along with the many other highquality<br />

diamonds across all the size ranges, is a<br />

testament to the unique aspect of the resource<br />

at Karowe,” Thomas said.<br />

The 998-carat rough, the Sethunya, and the<br />

Sewelô are the latest in a string of large<br />

diamonds found at Karowe. In 2015, Lucara<br />

mined the 1,111-carat Lesedi La Rona – the<br />

second-largest Botswanan diamond – from the<br />

site; it was sold to jeweller Graff Diamonds for<br />

$US53 million ($AU77 million) two years later.<br />

In 2016, Lucara sold the 813-carat Constellation<br />

diamond to Dubai-based Nemesis International<br />

for $US63.1 million ($AU86.8 million), setting a<br />

per-carat price record in the process.<br />

Gallagher have been<br />

developing insurance solutions<br />

for jewellers for over 20 years.<br />

Our advice is based on<br />

practical, proven knowledge<br />

of the needs and challenges<br />

facing jewellers in Australia.<br />

Coverage features can include:<br />

Accidental Damage<br />

Flood cover<br />

Burglary / armed hold up<br />

Sendings and carryings worldwide<br />

Entrustments to third parties<br />

Business Interruption<br />

Public and Products Liability<br />

Working upon extension<br />

Contact Gallagher today<br />

to find out how we can help<br />

protect your precious assets.<br />

Gretchen O’Brien<br />

0419 678 149<br />

ajg.com.au<br />

Arthur J. Gallagher & Co (Aus) Limited. AFSL 238812. Cover is<br />

subject to the Policy terms and conditions. You should consider if<br />

the insurance is suitable for you and read the Product Disclosure<br />

Statement (PDS) and Financial Services Guide (FSG) before<br />

making a decision to acquire insurance. These are available at<br />

www.ajg.com.au. REF2825-1120-2.3

The diamond<br />

pipeline<br />

has, for the<br />

first time<br />

in almost<br />

100 years,<br />

become truly<br />

demanddriven<br />

Pranay Narvekar<br />

and Chaim Even-<br />

Zohar<br />

DIAMOND<br />

INDUSTRY<br />

ANALYSTS<br />

New diamond industry report released<br />

The analysis identifies 2019 as a pivotal year.<br />

A new report exploring the restructuring of<br />

the diamond trade over the course of 2019<br />

and <strong>2020</strong> has been published, delving into the<br />

macroeconomic and industry-specific factors<br />

influencing the trade from mine to market.<br />

Authored by diamond industry analysts<br />

Pranay Narvekar and Chaim Even-Zohar –<br />

who have previously contributed to <strong>Jeweller</strong> –<br />

the report is titled The 2019 Pipeline: Prelude<br />

to the Storm.<br />

It details how the diamond market has<br />

switched from being largely supply-driven<br />

to a demand-focused model.<br />

“The diamond pipeline has, for the first time<br />

in almost 100 years, become truly demanddriven<br />

– at each and every level of the<br />

pipeline,” Narvekar and Even-Zohar write.<br />

“It has become a normal competitive industry<br />

not any more driven by the rough supply side,”<br />

they add.<br />

Calling the shift “a most desirable conclusion<br />

for the midstream” of the diamond industry –<br />

that is, cut-and-polishing operations in India,<br />

and polished diamond traders – Narvekar<br />

and Even-Zohar predict that the restructuring<br />

process will lead to an industry that is<br />

“structurally not only more competitive, but<br />

also much healthier”.<br />

The analysts identify 2019 as the turning point<br />

for change, describing it as a “gap year”.<br />

Stock levels were clearing amid falling<br />

prices and sales, ahead of a predicted steady<br />

recovery in the ensuing years.<br />

Even-Zohar and Narvekar also explored<br />

demand shifts in <strong>2020</strong> as a result of<br />

COVID-19.<br />

Indeed, the expected improvement in sales<br />

and prices failed to materialise this year as<br />

the pandemic unfolded, yet Narvekar and<br />

Even-Zohar conclude that the fundamental<br />

shifts initiated last year have ultimately left<br />

the diamond industry in a stronger position.<br />

Queensland jeweller to close Ipswich<br />

store after 20 years<br />

It’s been a<br />

wonderful<br />

experience<br />

for us all and<br />

we’re certainly<br />

going to miss<br />

our time here.<br />

It’s been a<br />

real pleasure<br />

looking after<br />

everybody<br />

The Pascoe <strong>Jeweller</strong>s store, located in the<br />

Riverlink Shopping Centre, will cease trading on<br />

Christmas Eve.<br />

As noted in <strong>Jeweller</strong>’s State of The Industry<br />

Report <strong>2020</strong>, Pascoe <strong>Jeweller</strong>s reduced<br />

its store count from nine to three between<br />

2010 and <strong>2020</strong>.<br />

Speaking to the Courier Mail, Geoff Pascoe<br />

explained, “[Ipswich] is the eighth [store]<br />

I’ve closed down so I’ve got two left.<br />

“My health hasn’t been the best. I’ve had<br />

cancer operations this year and I just had<br />

to close all the stores. I’ve decided it’s a lot<br />

easier to just try and close all the stores<br />

down than try and sell them.”<br />

Featuring the<br />

delicate pink tone of<br />

Argyle pink diamonds<br />

Geoff Pascoe<br />

PASCOE<br />

JEWELLERS<br />

The Ipswich branch of family-owned Pascoe<br />

<strong>Jeweller</strong>s, which had been operating in the<br />

Queensland city for two decades, will<br />

permanently close on Christmas Eve.<br />

The decision to close the store was made due<br />

to the ill health of owner Geoff Pascoe, who<br />

runs the business alongside wife Carolyn.<br />

Pascoe said the business had reduced its<br />

employee headcount from 100 to around<br />

30.Of the Ipswich closure, he added that<br />

customers were “so sad” to see the<br />

Riverlink Shopping Centre store go. The<br />

remaining stores are located in Toowoomba<br />

and Forest Lake; daughter Bianca Pascoe<br />

will take over the latter.<br />

SAMS GROUP<br />

AUSTRALIA<br />

E pink@samsgroup.com.au<br />

W samsgroup.com.au<br />

P 02 9290 2199

Pandora launches holiday marketing<br />

campaign with Millie Bobby Brown<br />

The new animated campaign – which is designed for social media – features a range<br />

of Pandora celebrity spokespeople.<br />

Pandora Jewelry has released its<br />

<strong>2020</strong> holiday season advertisement<br />

featuring its celebrity spokespeople,<br />

including Stranger Things actress<br />

Millie Bobby Brown.<br />

Described as a “mixed media short<br />

film” with “a message of love and<br />

unity”, the advertisement combines<br />

live action with animation and is titled<br />

One Lovely Day.<br />

In the clip, an animated Brown is<br />

joined by the Pandora ‘Muses’ –<br />

Game Of Thrones actress Nathalie<br />

Emmanuel, models Georgia May<br />

Jagger and Halima Aden, dancer<br />

Larsen Thompson, Australian<br />

fashion writer, director and<br />

consultant Margaret Zhang, and<br />

artist Tasya van Ree – and US-based<br />

music and design duo Coco & Breezy<br />

(sisters Corianna and Brianna<br />

Dotson).<br />

The group visit Los Angeles, New<br />

York, London, Shanghai and Australia<br />

in a magical gift box, where they<br />

distribute pink Pandora presents<br />

as the 1977 hit ‘Lovely Day’ by Bill<br />

Withers plays.<br />

Carla Liuni, chief marketing director,<br />

Pandora Jewelry, said, “We know this<br />

holiday season may be unusual, with<br />

some families unable to be together.<br />

So, we wanted to highlight that,<br />

regardless of where you are in the<br />

world, you can still celebrate with the<br />

ones you love and show them how<br />

much you care.<br />

“The aim of this feel-good animation<br />

is to share this sentiment in a really<br />

fun and engaging way.”<br />

The clip was produced by Andy<br />

Baker Studio in London. Andy<br />

Baker, director, said, “We wanted<br />

to combine the realism of the live<br />

action and the 2D in a way that<br />

felt unique and spent a lot of time<br />

working on how we would design the<br />

backgrounds using photography and<br />

background painting techniques to<br />

give us a really cool visual identity.”<br />

“We know this holiday season<br />

may be unusual, with some<br />

families unable to be together.<br />

So, we wanted to highlight that,<br />

regardless of where you are in<br />

the world, you can still celebrate<br />

with the ones you love”<br />

CARLA LIUNI<br />

Pandor Jewelry<br />

The advertisement is designed for<br />

social media and will be posted to<br />

Pandora’s own channels, as well<br />

as the social media channels of the<br />

celebrity spokespeople; they have a<br />

combined following of more than 48<br />

million on Instagram alone.<br />

Pursuing a digital-based advertising<br />

campaign appears to be a prudent<br />

move by Pandora.<br />

The company has focused on<br />

e-commerce growth throughout<br />

<strong>2020</strong> and a recent financial report<br />

indicated ‘triple-digit’ increases<br />

in online sales in its two largest<br />

markets – the US and UK – over the<br />

three months to 30 September.<br />

Proudly distributed by<br />

02 9417 0177 | www.dgau.com.au

10 Years Ago<br />

Time Machine: <strong>December</strong> 2010<br />

A snapshot of the industry events making headlines this time 10 years ago in <strong>Jeweller</strong>.<br />

Historic Headlines<br />

4 IIJS gears up for Mumbai debut<br />

4 Personalisation trend hits bridal jewellery<br />

4 Tiffany loses six-year battle against eBay<br />

4 Australia buoys Asia-Pacific market<br />

4 New consumer laws to aid jewellers<br />

Lab-grown diamonds<br />

to take off?<br />

A diamond manufacturer has revealed that it<br />

has been mass-producing colourless, synthetic<br />

diamonds and is gearing up to sell them online.<br />

Gemesis, which specialises in lab-grown<br />

diamonds, has until now focused mostly on fancycoloured<br />

stones.<br />

Colourless diamonds are more expensive to<br />

cultivate than fancy-coloured stones, but Gemesis<br />

is now using the chemical vapour deposition (CVD)<br />

method to produce thousands of carats a month<br />

from its manufacturing base in Southeast Asia.<br />

Chief executive and president Stephen Lux to US<br />

trade magazine JCK that the “created” gems are<br />

mostly more than 0.5 carat, H colour, and VS clarity.<br />

“This is a momentous thing,” Lux said. “We can<br />

provide to the consumer a colourless diamond<br />

that is identical in every way to a mined stone,<br />

except for its origin.”<br />

Diamond Exchange closes<br />

owing $2.5 million<br />

In what can be described as a tragedy for online<br />

diamond buyers, internet retailer Diamond<br />

Exchange has closed its doors.<br />

Diamond Exchange’s future was dealt a final<br />

blow when the Victorian Supreme Court ended its<br />

administration process and sent it into liquidation<br />

on 12 November after joint administrators Con<br />

Kokkinos and Matthew Jess of Worrells were<br />

unable to prove that the case could be resolved in<br />

a beneficial manner to creditors.<br />

Its debts total $2.5 million, of which $1 million is<br />

owed to customers.<br />

<strong>December</strong> 2010<br />

ON THE COVER State of the Industry Report<br />

Editors’ Desk<br />

4Market Intelligence: “The Yellow Pages<br />

is useless. Have you used it recently?<br />

I’m not just talking about the printed<br />

Yellow Pages either. I stopped using<br />

Yellowpages.com.au some time ago for<br />

many reasons, the main one being its<br />

lack of reliability.<br />

These days we think about directories<br />

differently, especially since the advent of<br />

internet search. Print directories<br />

are, and have always been, databases of<br />

information. The way that information<br />

is delivered – whether print, online or<br />

through your mobile – is less important<br />

than the quality of the information itself.<br />

The online version of the Yellow Pages<br />

is simply a different delivery mechanism<br />

for the same database of information.<br />

What has never changed is the need<br />

for accurate information, and that’s<br />

where the Yellow Pages lets you down<br />

– it’s inaccurate.<br />

Keep in mind that the very business<br />

of Yellow Pages is to provide accurate<br />

and up-to-date information, and if its<br />

information is neither accurate nor<br />

current then it’s useless.”<br />

STILL RELEVANT 10 YEARS ON<br />

Back to the Future:<br />

Increasing commodification will<br />

undoubtedly make some areas of<br />

jewellery retail far more impersonal,<br />

but the general consensus is that<br />

jewellery will become more personal<br />

– particularly at the higher end of the<br />

marke – through increased [customer]<br />

participation in design.<br />

JWNZ losing money<br />

The latest financial statements lodged by<br />

JWNZ show that not only did the association<br />

make a loss of more than $40,000 last year, but<br />

membership income is dropping.<br />

<strong>Jeweller</strong>s and Watchmakers of New Zealand is<br />

classified financially as an “incorporated society”<br />

and as such is required to have its accounts<br />

independently audited. The 2009/10 financial<br />

statements show JWNZ’s trade fair lost $14,000<br />

last year. The September fair had income of<br />

$79,083 but expenses of $93,578.<br />

Revenue from “commission” also declined,<br />

while costs – including travel and meetings,<br />

administrative, and magazine – increased.<br />

Ole Lynggaard eyes<br />

Australian flagship store<br />

High-end European jewellery brand Ole<br />

Lynggaard aims to further build its presence<br />

in Australia by opening a flagship store in<br />

the country.<br />

The move is part of a worldwide strategy to<br />

expand in international markets. Australia is<br />

the Danish brand’s second-strongest export<br />

market after Germany, depsite having only<br />

launched its jewellery here in 2009.<br />

Due to its desire for exclusivity, Ole Lynggaard’s<br />

imminent Australian store will support its<br />

existing retail base, rather than expanding it.<br />

The store will follow the mould of the premium<br />

Ole Lynggaard flagship in Copenhagen.<br />

READ ALL HEADLINES IN FULL ON<br />

JEWELLERMAGAZINE.COM<br />

24 | <strong>December</strong> <strong>2020</strong>

For your free copy of the Peter W Beck Catalogue containing over 2000 styles, please<br />

contact Marketing on 08 8440 3369 or at Marketing@pwbeck.com.au

INTERCHANGEABLE<br />

NEW<br />

A very Happy Christmas<br />

from the Timesupply team,<br />

best wishes for a safe and<br />

successful 2021.<br />

Timesupply<br />

jewellery + watches<br />

p +61 (0)8 8221 5580<br />

sales@timesupply.com.au | timesupply.com.au<br />

exclusive distributor AU & NZ

INSIDE<br />

Now & Then<br />

Fairfax & Roberts<br />

Celebrating 162 Years • SYDNEY, NSW • A moment with Irene Deutsch, CEO<br />

MILESTONE S<br />

L to R: Fairfax & Roberts employees pose for a photograph in 1896; the original Lamb & Fairfax premises on<br />

George Street in the 19th Century – a new workshop would later be established on nearby Hunter Street.<br />

Fairfax & Roberts is proud to be Australia’s<br />

oldest established jeweller. Our incredible<br />

story began in 1826 when Richard Lamb<br />

set up a business on Sydney’s main street<br />

as an optician and jeweller. He was later<br />

joined by Alfred Fairfax, of the Fairfax<br />

newspaper dynasty, and in 1858 together<br />

they established Fairfax & Roberts as<br />

Sydney’s first ‘emporium for fine silver and<br />

watchmaking’.<br />

One of Fairfax & Roberts’ early<br />

achievements, in 1873, was the design and<br />

production of the iconic tower clock that<br />

still marks time at Sydney’s Central Station.<br />

By 1886, the company was designing<br />

and creating the finest luxury jewellery,<br />

watches and objects d’art for Australia’s<br />

wealthiest families. These one-of-a-kind<br />

pieces have been tightly held for generations<br />

by the families who commissioned them.<br />

More than a century-and-a-half later,<br />

Fairfax & Roberts still trades in precious<br />

jewels as well as specialising in private<br />

commissions. We maintain our own<br />

workshop where pieces are exclusively<br />

designed and carved and set by hand.<br />

Most recently, the COVID-19 global<br />

pandemic presented a never-before-seen<br />

challenge for all businesses. We had to<br />

diversify, be agile and think creatively – and<br />

to ultimately accelerate many of our longterm<br />

projects.<br />

We successfully launched an online<br />

boutique for ready-to-wear jewellery,<br />

including our extensive range of<br />

international brands. We also renovated<br />

our flagship showroom and launch a<br />

new homewares brand, No.19, which has<br />

received overwhelmingly positive feedback.<br />

It was important to us that during these<br />

uncertain times, we continued to provide<br />

exceptional service and create a new and<br />

inviting space for our customers to visit once<br />

these times had passed.<br />

Our success throughout our history is<br />

measured in the tears of joy our customers<br />

shed when presented with a bespoke,<br />

heartfelt gift or when we hear of a Fairfax<br />

& Roberts engagement ring being passed<br />

from one generation to the next.<br />

The most beautiful part about our jewellery<br />

is that it carries our client’s life story.<br />

Indeed, tradition is a value that we proudly<br />

promote. Our brand is based on a tradition<br />

of quality, excellence, design innovation and<br />

exquisite craftsmanship.<br />

I enjoy it when customers come into the<br />

store and have stories to tell about their<br />

parents or grandparents having had an<br />

heirloom piece of jewellery made by us, and<br />

when I mention to people that I am CEO<br />

of Fairfax & Roberts, I see the amount of<br />

wonderful brand recognition it evokes.<br />

The most rewarding part is knowing that<br />

we continue to create history every day,<br />

by making beautiful pieces of jewellery to<br />

mark some of the most special occasions<br />

in people’s lives.<br />

I do feel a sense of responsibility to continue<br />

the brand, and the traditions and the high<br />

level of quality our clients expect. However,<br />

I also find it incredibly exciting to be part of<br />

something with such great history.<br />

This desire to create luxury jewellery that<br />

is meaningful, now and in the future, flows<br />

1858<br />

Richard Lamb and<br />

Alfred Fairfax found<br />

Sydney’s first ‘emporium<br />

for fine silver and<br />

watchmaking’ at<br />

394 George Street, under<br />

the name Lamb & Fairfax<br />

1873<br />

Lamb & Fairfax designs<br />

and produces the clock<br />

tower for Sydney’s<br />

Central Station<br />

1876<br />

Richard Lamb passes<br />

away and Alfred<br />

Fairfax’s nephew Barton<br />

joins the business<br />

1886<br />

Oscar G Roberts invests<br />

in the business and its<br />

name is changed to<br />

Fairfax & Roberts. A new<br />

workshop at 23 Hunter<br />

Street and an outlet in<br />

London are opened, and<br />

the company registers its<br />

‘maker’s mark’ with the<br />

London Assay Office<br />

1898<br />

Fairfax & Roberts<br />

manufactures the<br />

commemorative solid<br />

gold ‘opening key’ to<br />

the Queen Victoria<br />

Building<br />

1927<br />

Fairfax & Roberts crafts<br />

a sterling silver kangaroo<br />

pin for the Prince of<br />

Wales – the future King<br />

Edward VIII – upon his<br />

visit to Australia<br />

1990<br />

The business moves<br />

into an iconic Art Deco<br />

building near Sydney’s<br />

Martin Place<br />

2008<br />

Fairfax & Roberts<br />

celebrates its 150th<br />

anniversary with a<br />

coffee table book and<br />

new jewellery collections<br />

Above: The Fairfax & Roberts boutique as it is<br />

today, on Castlereagh Street near Martin Place.<br />

throughout everything we do. It informs<br />

our standard and keeps pushing us to<br />

consistently please our customers with<br />

jewellery that inspires and delights.<br />

At the heart of the Fairfax & Roberts<br />

brand – and what makes our pieces<br />

so desirable – is the unique quality of<br />

our designs.<br />

Creating beautiful jewellery is a task<br />

that the artisans of Fairfax & Roberts<br />

take seriously, continuously creating<br />

new collections to showcase our<br />

stunning showroom.<br />

We have set our quality standards<br />

exceptionally high and we stay true<br />

to this with every piece that leaves<br />

our workshop.<br />

My partner and I love Fairfax & Roberts<br />

for so many reasons. We are committed<br />

to honouring its rich history and want<br />

to continue to make this a place where<br />

happiness is created.<br />

As a newly-appointed CEO, I would<br />

obviously like to put my own stamp on<br />

the business – with a nod to tradition.<br />

Our customers should expect to see<br />

our name out there more often, and<br />

some new jewellery collections in the<br />

new year.<br />

We want to make Fairfax & Roberts a<br />

destination, where people know they<br />

will always find something special and<br />

interesting. We want to be the best at<br />

what we do and continually delight our<br />

customers – hopefully for many years<br />

to come!<br />

Read the full length interview<br />

on <strong>Jeweller</strong>magazine.com<br />

<strong>December</strong> <strong>2020</strong> | 27

INSIDE<br />

My Store<br />

Rohan <strong>Jeweller</strong>s<br />

PERTH, WA with Rohan Milne, founder and creative director • SPACE COMPLETED 2008, though we have made continual updates since then<br />

4Who is the target market?<br />

A love of collaborating with our customers and<br />

handcrafting custom jewellery is at the core of<br />

the Rohan <strong>Jeweller</strong>s philosophy – we have<br />

become synonymous with that.<br />

Our clients seek a highly personalised experience<br />

when embarking on creating a bespoke piece<br />

of jewellery with us, so this factor had great<br />

influence when designing our boutique in<br />

Leederville – one of our two Perth stores.<br />

A private viewing room within the boutique<br />

provides a relaxed and intimate setting to try<br />

on collection pieces, explore ideas with our<br />

designers, and view our range of loose gemstones<br />

– including coveted Argyle pink diamonds –<br />

with me.<br />

4Which features encourage sales?<br />

I was inspired to create a luxury boutique with<br />

a relaxed environment that makes people feel<br />

at ease.<br />

Rohan <strong>Jeweller</strong>s is a welcoming space where<br />

clients can explore their own ideas and work<br />

with a designer to have them turned into highquality<br />

jewellery.<br />

4What is the store design’s ‘wow factor’?<br />

Unique to our Leederville boutique, our workshop<br />

– where all of our pieces are handcrafted – is<br />

located on-site. We invite customers to visit our<br />

workshop at any time where our master jewellers<br />

are constantly working on new pieces.<br />

I’m happy to show them the precise tools that<br />

I and the team of jewellers will use as they<br />

collaborate in the creation of each unique piece.<br />

28 | <strong>December</strong> <strong>2020</strong>

Completing my Diploma in<br />

Gemmology has benefited<br />

me as a jeweller in more<br />

ways than I ever expected.<br />

I have always had an interest<br />

in gemstones and found<br />

the course was not only<br />

informative and challenging<br />

but immensely rewarding.<br />

Studying with the GAA has also<br />

allowed me to meet like-minded<br />

people from many facets of the<br />

jewellery industry and grants me access<br />

to resources that I will continue to use<br />

throughout my professional career.<br />

Emma Meakes FGAA<br />

<strong>Jeweller</strong>, John Miller Design - WA<br />

Diploma in<br />

Gemmology<br />

Enrolments now open<br />

For more information<br />

1300 436 338<br />

learn@gem.org.au<br />

www.gem.org.au<br />

Be<br />

Brilliant<br />

Gem-Ed Australia<br />

ADELAIDE BRISBANE HOBART MELBOURNE PERTH SYDNEY<br />

Passionately educating the industry, gem enthusiasts<br />

and consumers about gemstones

REVIEW<br />

Gems<br />

Lapis lazuli: The night sky in your hand<br />

L to R: Fred Leighton ring, Chow Tai Fook necklace, Andrew Grima<br />

brooch | Below: Boucheron bracelet, Arman Sarkisyan ring<br />

Lapis lazuli, often shortened to lapis, gained<br />

its name from Latin and Persian origins –<br />

lazhuward meaning ‘blue’ in Persian and<br />

lapis meaning ‘stone’ in Latin. The gem has<br />

been highly prized for thousands of years,<br />

being used in jewellery, carvings, seals and<br />

decorative items..<br />

In the ancient world, lapis lazuli was worn<br />

to signify rank and wealth, having been<br />

used by kings and nobles as seals to mark<br />

their official documents.<br />

It has long been associated with wisdom,<br />

protection, love and healing.<br />

During the Renaissance the gem was<br />

prized by European artists. Ground to a fine<br />

powder, lapis was the source of a colour<br />

pigment called ultramarine.<br />

Under a microscope, lapis lazuli looks like<br />

the night sky – with depths of blue lazurite,<br />

a fine white haze of calcite and the starlike<br />

sparkle of pyrite.<br />

Lapis ranges in colour from greenish blue<br />

to rich royal blue and violet blue. The most<br />

prized – and valuable – is an intense royal<br />

blue featuring minute gold flashes of pyrite.<br />

Afghanistan is considered the most<br />

significant source of quality lapis. The gem<br />

has been mined there for thousands of<br />

years in a remote and inhospitable region,<br />

known historically as Bactria.<br />

From isolated valleys, lapis was transported<br />

by camel caravan to the bazaars of the<br />

Mediterranean and then westwards to the<br />

gem trading houses of Europe.<br />

Lapis lazuli<br />

From Persion<br />

lazhuward meaning<br />

‘blue’ and Latin lapis<br />

meaning ‘stone’.<br />

and called ‘Prussian blue’ or ‘Berlin blue’ is<br />

one to note.<br />

To detect staining, look for dye between the<br />

grains of the gem and the tell-tale gleam of<br />

transparent quartz, which is not present in<br />

natural lapis.<br />

Sintered synthetic spinel – to which pyrite<br />

is added during the sintering process<br />

–is another imitant. Sintering involves<br />

compacting synthetic materials to make a<br />

solid mass.<br />

Sodalite is a gem that, to the untrained eye,<br />

can look like lapis. It is not the rich royal<br />

blue of lapis, but rather a greyish blue. Look<br />

for the absence of pyrite and evidence of<br />

dyeing – such as uneven colour and patches<br />

of dye in and around bead drill holes.<br />

It was an expensive material used only<br />

by artists of established reputation for<br />

religious works and private commissions<br />

by wealthy sponsors.<br />

Lapis lazuli is an aggregate comprised<br />

primarily of lazurite, calcite and pyrite.<br />

Quality lapis consists mainly of lazurite<br />

– which gives the gem its intense blue<br />

colour – with small amounts of white<br />

calcite and pyrite.<br />

It is the metallic flash of pyrite against<br />

the deep blue of lazurite that makes it so<br />

attractive to gem collectors and jewellery<br />

artists. Lesser quality lapis will often<br />

be a faded blue, without the depth and<br />

brightness of the finer quality, and will have<br />

a greater concentration of calcite.<br />

Today, other sources are Lake Baikal in<br />

Siberia, Chile, Angola, Pakistan, Canada<br />

and Colorado in the US.<br />

Lapis has long been fashioned into beads,<br />

cabochons, inlays and free-form shapes.<br />

Historically, the gem was also valued<br />

as a carving material for ornaments,<br />

hair combs, game board pieces and<br />

protective amulets.<br />

Lapis is often treated. It is a porous gem<br />

that lends itself to waxing and oiling to<br />

improve its lustre. Lesser quality lapis is<br />

often dyed to reduce the appearance of<br />

calcite and to enhance the blue of lazurite.<br />

As high-quality lapis is expensive there are<br />

imitants on the market; jasper stained blue<br />

Colour: Blue to bluepurple,<br />

mottled<br />

Found in: Afghanistan,<br />

Russia, Chile, Angola,<br />

Pakistan, Canada<br />

and the US<br />

Mohs Hardness: 5–6<br />

Class: Metamorphic<br />

rock<br />

Lustre: Waxy to vitreous<br />

Formula:<br />

(Na,Ca) 8<br />

Al 6<br />

Si 6<br />

O 24<br />

(S,SO) 4<br />

Reconstructed lapis lazuli is made from<br />

low quality lapis crushed and bonded with<br />

resin. Pyrite is added to the mix. To identify<br />

it, look for a smooth surface texture even on<br />

chipped surfaces, a colour that looks ‘too<br />

perfect’, and the absence of calcite.<br />

As lapis is considered a relatively soft gem,<br />

use mild soapy water to clean. Rinse and<br />

leave to dry. Avoid using harsh chemicals<br />

or an ultrasonic cleaner.<br />

Susan Hartwig FGAA combines her love<br />

for writing with a passion for gems and<br />

jewellery through her gemmology blog,<br />

ellysiagems.com. For more information<br />

on gemmology courses and gemstones,<br />

visit gem.org.au<br />

<strong>December</strong> <strong>2020</strong> | 31

CELEBRATING<br />

Local Talent<br />

LUCAS BLACKER<br />

JEWELLERY<br />

Freeform Colour<br />

Stone Bangle<br />

Metals: Platinum,<br />

18-carat yellow gold and<br />

rose gold<br />

Gemstones: Rhodolite<br />

and spessartite<br />

garnet, blue and<br />

parti-colour<br />

sapphire, diamond<br />

Lucas Blacker<br />

Sydney, NSW<br />

MEADOWLARK<br />

Snake & Star Ring Set<br />

Metal: 9-carat yellow gold<br />

Gemstones: Morganite,<br />

diamond<br />

Claire Hammon & Greg<br />

Fromont<br />

Auckland, NZ<br />

DAVID KEEFE FINE<br />

JEWELLERY<br />

Flower Ring<br />

Metal: 9-carat yellow gold<br />

Gemstones: Citrine,<br />

amethyst, blue topaz<br />

David Keefe Jr<br />

Auckland, NZ<br />

Australia and New Zealand are not only home to some of the<br />

rarest gemstones in the world, but also the most talented jewellers.<br />

<strong>Jeweller</strong> showcases a tapestry of local masterpieces that have been<br />

meticulously crafted with great artisanship, right here on home soil<br />

ONE ORANGE DOT<br />

Oval Link Bracelet<br />

Metal: Stainless steel<br />

Sean O’Connell<br />

Bundeena, NSW<br />

RACHEL LAURA GORMAN<br />

Pink Fuchsia Giardinetti<br />

Ring (above) & Gem Garden<br />

Ring (below)<br />

Metal: Sterling silver<br />

Gemstones: Above - Garnet,<br />

pink tourmaline, rose quartz,<br />

amethyst; Below - Sapphire,<br />

tourmaline, blue topaz<br />

Rachel Laura Gorman<br />

Melbourne, VIC<br />

32 | <strong>December</strong> <strong>2020</strong>

PAYET GALLERY<br />

Blue Beryl & Gold Ring<br />

Metal: 18-carat<br />

yellow gold<br />

Gemstone: Blue beryl<br />

Nicholas &<br />

Francois Payet,<br />

Margaret River, WA<br />

MARK EVANS<br />

FINE JEWELLERY<br />

Water Drop Pendant<br />

Metal: 18-carat white gold<br />

Gemstones: Blue topaz,<br />

diamond, clear quartz<br />

(chain)<br />

Mark Evans<br />

Maroochydore, QLD<br />

SCULPTED<br />

JEWELS<br />

Leaf Pendant<br />

Metals: 9-carat<br />

rose and white gold<br />

Gemstone: White<br />

diamond<br />

Roley McIntyre<br />

Wagga Wagga, NSW<br />

JUAN CASTRO<br />

Persefone Earrings<br />

Metal: 9-carat<br />

yellow gold<br />

Gemstone: Pink<br />

tourmaline<br />

Juan Castro<br />

Melbourne, VIC<br />

EBBEKE & CO.<br />

Art Deco Emerald<br />

Ring<br />

Metals: Platinum,<br />

18-carat yellow gold<br />

Gemstones: Emerald,<br />

diamond<br />

Lucas Ebbeke<br />

Auckland, NZ<br />

SUSAN EWINGTON<br />

Hanna Ring<br />

Metal: 18-carat<br />

yellow gold<br />

Gemstones: Parti<br />

sapphire, cognac<br />

diamond<br />

Susan Ewington<br />

Noosaville, QLD<br />

JOHN MILLER DESIGN<br />

Ocean Story – Beneath<br />

The Waves Cuff<br />

Metal: Hand-engraved and<br />

stamped sterling silver<br />

John Miller<br />

Yallingup, WA<br />

<strong>December</strong> <strong>2020</strong> | 33

Proudly distributed by<br />

(02) 9417 0177 | www.dgau.com.au

STATE OF THE INDUSTRY<br />

10 Years at a Glance<br />

STATE OF THE<br />

INDUSTRY REPORT<br />

AN IN-DEPTH REPORT OF AUSTRALIA’S JEWELLERY INDUSTRY OVER A DECADE<br />

RESEARCH FEATURE: 10 YEARS AT A GLANCE<br />

JEWELLERY<br />

RETAIL<br />

EVOLUTION<br />

There is little doubt the past 10 years have led to<br />

a significant change in the Australian jewellery<br />

landscape – yet analysis of the data by <strong>Jeweller</strong><br />

shows a number of surprising trends and stories.<br />

CHAIN STORES<br />

The demise of fashion jewellery chains<br />

Fine jewellery demonstrates unexpected resilience<br />

Mid-sized jewellery chains have mixed results<br />

BRAND-ONLY STORES<br />

Huge increase in brand-only stores over past decade<br />

International luxury groups make their mark<br />

BUYING GROUPS<br />

Shake up for the buying groups in <strong>2020</strong><br />

How will they fare in the future?<br />

<strong>December</strong> <strong>2020</strong> | 35

BACKGROUND<br />

STATE OF THE INDUSTRY<br />

REPORT EXPLAINED<br />

The first detailed analysis of the Australian jewellery industry was published in<br />

2003. It examined, and measured, the number of jewellery stores in the major<br />

shopping centres in each state and, interestingly, found that jewellers accounted<br />

for a ‘standard’ five per cent of all specialty stores in shopping centres.<br />

The research also surveyed the number of jewellery chains and compared their<br />

store count by state, also comparing that data against each state’s population data.<br />

In the following years, <strong>Jeweller</strong> conducted adhoc research and in 2007 we<br />

published a more comprehensive analysis of the chain stores. At the time, there<br />

were around 1,000 stores listed, however, a need emerged to refine the research<br />

by better defining store types and product categories.<br />

This process culminated in the 2010 State of the Industry Report, published in<br />

<strong>December</strong> that year.<br />

The 68-page 2010 report offered a definition of – and differentiation between –<br />

independent jewellery businesses, fashion and fine jewellery stores, chain stores,<br />

brand-only and flagship stores, and finally jewellery kiosks.<br />

Unsurprisingly, the jewellery industry has continued to evolve to the extent that,<br />

in some ways, it’s a little like going ‘back to the future’; the industry appears to<br />

be evolving full circle, back to its roots.<br />

That is, independent jewellers are increasingly focusing on high-value items<br />

– often custom-made jewellery for specific clients – along with repairs and<br />

remodels. In part, it’s a crucial move to differentiate from easily purchased, lowvalue/low-priced<br />

items sold on the internet.<br />

At the same time, a notable change from previous reports is suppliers<br />

(wholesalers) altering their distribution models, becoming defacto retail operations<br />

that compete with independent jewellers.<br />

What began as high-profile watch and jewellery brands establishing ‘Flagship’<br />

stores – purported to assist independent stockists – has, in some cases, morphed<br />

into full-on competition. As part of the evolution, <strong>Jeweller</strong> has redefined the<br />

flagship and brand-only categories, which is explained in the article. It largely<br />

affected how we define Pandora’s business model, moving it from the brand-only<br />

category to the chain store category.<br />

As the industry changes in the coming years, there may be a need to re-evaluate<br />

the definitions used in future State of the Industry Reports.<br />

<strong>Jeweller</strong> endeavours to maintain definitions where they are appropriate and<br />

relevant to the current trading environment, and to enable simple comparison with<br />

data in previous reports.<br />

This edition, therefore, covers the chain and brand-only store categories as well as<br />

the current membership and stores counts of the four buying groups – Nationwide,<br />

Showcase, Leading Edge and the new entrant, Independent <strong>Jeweller</strong>s Collective.<br />

SAVING THE BEST FOR LAST<br />

At the beginning of <strong>2020</strong>, <strong>Jeweller</strong>’s intention was to include an analysis of the<br />

most important category of all: independent jewellery stores. It would mark the<br />

10-year anniversary of the first detailed analysis of the true state of the industry.<br />

However, the COVID-19 pandemic not only dramatically affected our ability to<br />

undertake the research but, more importantly, the resulting economic crisis has<br />

had a major impact on jewellery stores – to the extent that many closed.<br />

For that reason, we decided to research and quantify the number of independent<br />

jewellers after the <strong>2020</strong> Christmas trading period. This report will be available in<br />

the New Year.<br />

36 | <strong>December</strong> <strong>2020</strong>

STATE OF THE INDUSTRY<br />

Chains through the Decade<br />

CHAIN REACTIONS<br />

Australian jewellery retailing has undergone significant evolution over the past<br />

decade, but, surprisingly, the changes are very different to what was expected when<br />

<strong>Jeweller</strong> published its last State of the Industry Report in 2010.<br />

A<br />

decade on from <strong>Jeweller</strong>’s first State of<br />

the Industry Report, the jewellery retail<br />

industry – mirroring the broader retail<br />

sector – has undergone momentous change. Yet<br />

over the past 10 years, fine jewellery chain stores<br />

have remained relatively resilient, at least in<br />

terms of store numbers.<br />

However, the same cannot be said for the fashion<br />

jewellery category!<br />

There were 21 fine jewellery chain store ‘brands’ in 2010,<br />

operating a total of 977 stores nationally. On a Like-By-Like<br />

basis, by <strong>2020</strong> that number had declined by 125 stores to 852,<br />

representing a 13 per cent reduction in total store count.<br />

That contraction could be considered small when compared<br />

with the performance of other consumer categories.<br />

Some fine jewellery chains – such as Prouds and Michael Hill<br />

– managed to increase overall store numbers, while others<br />

marginally decreased.<br />

Only two ‘names’ entirely disappeared from the list: Blue<br />

Spirit, a lesser-known small franchise, which operated six<br />

stores in 2010, and the high-profile Thomas <strong>Jeweller</strong>s, with<br />

nine stores.<br />

James Thomas founded Thomas <strong>Jeweller</strong>s in 1896 in<br />

Ballarat. After 121 years of operation, the Thomas family<br />

decided to close its iconic Bourke Street Mall store in<br />

Melbourne in October 2017, as well as the Warnambool,<br />

Wagga Wagga, Albury, Shepparton, Bendigo, Ballarat and<br />

Geelong stores.<br />

In contrast, of the seven fashion jewellery chains listed in the<br />

State of the Industry Report (SOIR) 10 years ago, only one<br />

remains – six closed their physical stores.<br />

The proverbial ‘last man standing’, Lovisa, has grown from 35<br />

locations in Australia to 152 over the past decade, following<br />

the liquidation and closure of major competitors and smaller<br />

fashion jewellery chains alike – including its sister chain Diva.<br />

The ‘downfall’ of the six fashion jewellery chains means<br />

that of the 378 stores that were operating in 2010, 343 no<br />

longer exist.<br />

Demise of fashion chains<br />

For the purpose of research and a report, it is necessary<br />

to create definitions in order to accurately measure and<br />

compare results across categories and over time.<br />

Therefore, a ‘chain’ is defined as a group of five or more<br />

BY THE NUMBERS<br />

Chain Insights<br />

In this report, a ‘chain’<br />

is defined as a group of<br />

five or more jewellery<br />

stores trading under<br />

the one (brand) name,<br />

with one ownership<br />

entity – a person or<br />

company –<br />

co-ordinating buying<br />

and marketing<br />

activities across the<br />

group. It could include a<br />

franchise operation.<br />

1164<br />

fine jewellery<br />

chain stores<br />

remain open as<br />

at <strong>December</strong> <strong>2020</strong><br />

343<br />

of 378 fashion<br />

jewellery chain<br />

stores have closed<br />

since 2010<br />

50%<br />

chains in<br />

Australia are<br />

owned and / or<br />

controlled by New<br />

Zealand entities<br />

jewellery stores trading under the one (brand) name, with<br />

one ownership entity – a person or company – co-ordinating<br />

buying and marketing activities across the group. It could<br />

include a franchise operation.<br />

In addition, <strong>Jeweller</strong> notes that a chain store usually has<br />