Growth strategies in retail banking Study - Roland Berger

Growth strategies in retail banking Study - Roland Berger

Growth strategies in retail banking Study - Roland Berger

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

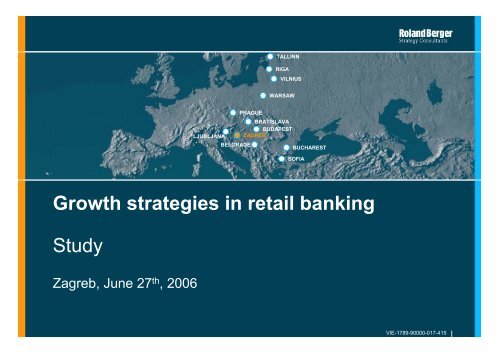

LJUBLJANA<br />

BELGRADE<br />

PRAGUE<br />

TALLINN<br />

RIGA<br />

VILNIUS<br />

WARSAW<br />

BRATISLAVA<br />

BUDAPEST<br />

ZAGREB<br />

BUCHAREST<br />

SOFIA<br />

<strong>Growth</strong> <strong>strategies</strong> <strong>in</strong> <strong>retail</strong> bank<strong>in</strong>g<br />

<strong>Study</strong><br />

Zagreb, June 27 th , 2006<br />

VIE-1789-90000-017-415<br />

1

Contents Page<br />

A. Development of CEE bank<strong>in</strong>g market 3<br />

B. Successful <strong>retail</strong> bus<strong>in</strong>ess models 12<br />

C. Potential development of the Croatian <strong>retail</strong> bank<strong>in</strong>g 32<br />

This document was created for the exclusive use of our clients. It is not complete unless supported by the underly<strong>in</strong>g detailed analyses and oral presentation. It must not<br />

be passed on to third parties except with the explicit prior consent of <strong>Roland</strong> <strong>Berger</strong> Strategy Consultants.<br />

VIE-1789-90000-017-415<br />

2

LJUBLJANA<br />

PRAGUE<br />

BELGRAD<br />

TALLINN<br />

RIGA<br />

VILNIUS<br />

WARSAW<br />

BRATISLAVA<br />

BUDAPEST<br />

ZAGREB<br />

ZAGREB<br />

BUCHAREST<br />

SOFIA<br />

A. Development of CEE bank<strong>in</strong>g markets<br />

VIE-1789-90000-017-415<br />

3

The CEE bank<strong>in</strong>g market has experienced three<br />

dist<strong>in</strong>ct phases<br />

Banks<br />

Customers<br />

Foundation 1990-1995<br />

Countries start build<strong>in</strong>g full<br />

function<strong>in</strong>g bank<strong>in</strong>g sector<br />

Foreign <strong>in</strong>vestors start<br />

enter<strong>in</strong>g the market<br />

Market focus on corporate<br />

bank<strong>in</strong>g<br />

Consumer bank<strong>in</strong>g market<br />

still immature<br />

Privatization 1995-2000 Consolidation 2001-...<br />

Privatization of state<br />

owned banks<br />

Foreign banks start buy<strong>in</strong>g<br />

local banks<br />

Bankruptcy of some new<br />

local banks<br />

Competition <strong>in</strong> corporate<br />

bank<strong>in</strong>g <strong>in</strong>creases<br />

Retail bank<strong>in</strong>g market<br />

develops<br />

Competition heats up, especially from<br />

foreign players<br />

Markets are "underbanked" <strong>in</strong><br />

capitalization and product penetration<br />

International banks start to review<br />

their CEE strategy<br />

Corporate bank<strong>in</strong>g market becomes<br />

mature<br />

SME market segment starts fast<br />

development<br />

Huge potential perceived <strong>in</strong> <strong>retail</strong><br />

lend<strong>in</strong>g market and <strong>in</strong>vestment fund<br />

bus<strong>in</strong>ess<br />

Phase 1 Phase 2 Phase 3<br />

VIE-1789-90000-017-415<br />

4

Bank privatization is almost complete <strong>in</strong> CEE<br />

% bank<strong>in</strong>g assets controlled<br />

by the state, 2005<br />

23.9%<br />

SE<br />

21.0%<br />

19.1%<br />

PL SL RO<br />

5.0% 4.5%<br />

3.1%<br />

2.0% 1.8%<br />

0.0%<br />

CZ<br />

HR<br />

BG<br />

SK<br />

Comments<br />

Source: Central banks, ECB, Raiffeisen Research "CEE Bank<strong>in</strong>g sector report, 2005<br />

HU<br />

Poland: The state reduced its majority stake <strong>in</strong> PKO<br />

through a public offer<strong>in</strong>g <strong>in</strong> 2004; sold stake <strong>in</strong> BGZ to<br />

Rabobank and EBRD<br />

Serbia: Privatization took off <strong>in</strong> 2005, 4 small banks<br />

privatized d<strong>in</strong> 2004/ 2005, Vojvodjanska (#4) up for sale<br />

Bulgaria: Privatization complete <strong>in</strong> 2003<br />

Romania: CEC privatization ongo<strong>in</strong>g, BCR completed<br />

Croatia: Croatia Banka and HPB - Postanska Banka<br />

Notes: Updated to reflect BCR’s privatization <strong>in</strong> 2005: A stake of 62% of BCR was sold to ERSTE Bank<br />

VIE-1789-90000-017-415<br />

5

Four groups of regionally-diversified CEE banks<br />

can be dist<strong>in</strong>guished<br />

1<br />

3<br />

Local champions<br />

OTP<br />

PKO BP<br />

Strong presence <strong>in</strong><br />

selected markets<br />

KBC<br />

Erste Bank<br />

Banca Intesa<br />

ING<br />

= Asset share foreign banks,<br />

as of end 2004<br />

ERSTE<br />

KBC<br />

SocGen<br />

BA CA<br />

KBC<br />

SocGen<br />

BA CA<br />

Overview foreign players<br />

94%<br />

UniCredito<br />

BA CA<br />

Citibank<br />

ING<br />

PL<br />

CZ SK<br />

68%<br />

97%<br />

80%<br />

36% HU RO<br />

SV HR 91%<br />

UniCredito<br />

Banca Intesa<br />

Raiffeisen<br />

89%<br />

Foreign banks with market share of 77 % <strong>in</strong> CEE countries!<br />

Banca Intesa<br />

ERSTE<br />

Raiffeisen<br />

BG<br />

75%<br />

Banca Intesa<br />

Bayern LB<br />

ERSTE<br />

KBC<br />

ERSTE<br />

Raiffeisen<br />

SocGen<br />

ABN<br />

Amro<br />

2<br />

4<br />

Comprehensive<br />

regional players<br />

UniCredito/ BA CA<br />

Raiffeisen<br />

Societe Generale<br />

Citibank<br />

Volksbank<br />

Specialists and<br />

opportunistic<br />

players<br />

Allied Irish Bank<br />

BCP Millenium<br />

Fortis<br />

Credit Lyonnais<br />

ABN Amro<br />

BNPParibas<br />

VIE-1789-90000-017-415<br />

6

A second wave of M&A activities is expected as<br />

smaller foreign banks will review their CEE strategy<br />

Banks<br />

1)<br />

2)<br />

Countries<br />

2005<br />

9<br />

7<br />

5<br />

7<br />

1<br />

2<br />

1<br />

1<br />

Total Assets<br />

<strong>in</strong> CEE, 2004<br />

[EUR m]<br />

15,600<br />

4,100<br />

5,500<br />

16,500<br />

6,500<br />

5,300<br />

5,100<br />

1,600<br />

Notes: 1) Focus Poland/only small subsidiaries <strong>in</strong> other countries 2) 2 as of 2005 (HU and BG)<br />

Foreign players of small size/ with limited<br />

presence review their CEE bank<strong>in</strong>g strategy,<br />

might consider exit<br />

Second wave M&A activities expected/<br />

already happen<strong>in</strong>g (e.g. OTP’s appetite for<br />

more CEE assets, divestments by Unicredit<br />

<strong>in</strong> Croatia)<br />

Consolidation with<strong>in</strong> foreign bank<strong>in</strong>g players<br />

expected<br />

Opportunities for "late entrants" or further<br />

consolidation of the bank<strong>in</strong>g sector<br />

VIE-1789-90000-017-415<br />

7

CEE markets are attractive because they are<br />

underbanked compared to the EU<br />

Bank<strong>in</strong>g assets<br />

% GDP, 2005<br />

350<br />

300<br />

250<br />

200<br />

150<br />

100<br />

50<br />

0<br />

EURO zone<br />

75.913 EUR<br />

SV<br />

14.658 EUR<br />

CZ HU<br />

PL<br />

Croatia: level of f<strong>in</strong>ancial <strong>in</strong>termediation<br />

highest <strong>in</strong> CEE<br />

Despite restrictive measures by the central<br />

bank, cont<strong>in</strong>u<strong>in</strong>g to grow powerfully<br />

Level <strong>in</strong> Croatia still beh<strong>in</strong>d Euro zone,<br />

leav<strong>in</strong>g room for future expansion<br />

Croatia<br />

8.030 EUR<br />

0 5 10 15 20 25 40 30<br />

Notes: 1) 2002-2005 CAGR for bank<strong>in</strong>g assets; The size of the bubble represents the bank<strong>in</strong>g assets/capita<br />

Source: <strong>Roland</strong> <strong>Berger</strong> Strategy Consultants, BA-CA CEE Report, ECB, Eurostat, Central banks<br />

SK<br />

BG<br />

RO<br />

CAGR 1) %<br />

VIE-1789-90000-017-415<br />

8

Croatia is the lead<strong>in</strong>g CEE country on <strong>retail</strong> lend<strong>in</strong>g<br />

– Even more than on <strong>retail</strong> deposits<br />

Retail lend<strong>in</strong>g as % of GDP Retail deposits as % of GDP<br />

4.4<br />

15.3<br />

10.0<br />

4.5<br />

2.1<br />

0.5<br />

18.2<br />

10.9<br />

5.9<br />

5.0<br />

2.8<br />

0.7<br />

24.0<br />

12.4<br />

8.8<br />

6.5<br />

3.7<br />

1.4<br />

28.5<br />

12.6<br />

12.5<br />

8.3<br />

3.8<br />

6.2<br />

31.5<br />

14.9<br />

9.9<br />

4.6<br />

13.1<br />

10.4<br />

37.8<br />

16.5<br />

12.0<br />

2000 2001 2002 2003 2004 2005<br />

52.6% EU 12 54.4% EU 12<br />

7.7<br />

1)<br />

15.9<br />

14.0<br />

HR<br />

BG<br />

HU<br />

PL<br />

CZ<br />

RO<br />

Notes: For EU 12, <strong>retail</strong> lend<strong>in</strong>g and deposits <strong>in</strong>clude non profit <strong>in</strong>stitutions serv<strong>in</strong>g households<br />

Source: ECB Monthly Bullet<strong>in</strong>, CEE Bank<strong>in</strong>g Sector Report 2005 by RZB Group,<br />

1) Data for 2005 estimated – CAGR 20%<br />

CEE Household Credit report by Unicredit<br />

VIE-1789-90000-017-415<br />

31.3<br />

27.8<br />

13.4<br />

36.6<br />

24.4<br />

9.8<br />

43.8<br />

37.5<br />

29.5<br />

24.9<br />

17.0<br />

10.6<br />

41.1<br />

41.9<br />

42.8<br />

35.8 35.2 35.1<br />

30.1<br />

23.9<br />

17.6<br />

10.5<br />

26.1<br />

24.7<br />

19.9<br />

10.1<br />

25.4<br />

23.7<br />

23.2<br />

10.2<br />

44.0<br />

38.2<br />

27.8<br />

22.9<br />

10.9<br />

2000 2001 2002 2003 2004 2005<br />

1)<br />

25.9<br />

HR<br />

CZ<br />

BG<br />

HU<br />

PL<br />

RO<br />

9

Low mortgage penetration will drive growth <strong>in</strong> <strong>retail</strong><br />

lend<strong>in</strong>g, probably more than consumer f<strong>in</strong>ance<br />

Mortgage lend<strong>in</strong>g as % GDP [%] 2005 Consumer lend<strong>in</strong>g as % GDP [%] 2005<br />

EU 12<br />

HR 1)<br />

HU<br />

CZ<br />

PL<br />

RO 2.0<br />

5.3<br />

BG 4.6<br />

11.0<br />

9.5<br />

8.6<br />

36.6<br />

CAGR 2)<br />

10%<br />

18%<br />

66%<br />

50%<br />

26%<br />

124%<br />

98%<br />

EU 12<br />

Notes: For EU 12, <strong>retail</strong> lend<strong>in</strong>g <strong>in</strong>cludes non profit <strong>in</strong>stitutions serv<strong>in</strong>g households 1) Data for 2005 estimated 2) CAGR 2000-2005<br />

HR 1)<br />

Source: Bank<strong>in</strong>g structures CEE (ECB), ECB Monthly Bullet<strong>in</strong>, CEE Bank<strong>in</strong>g Report 2005<br />

BG<br />

PL<br />

HU<br />

RO 5.8<br />

7.4<br />

CZ 6.2<br />

9.5<br />

11.2<br />

16.0<br />

24.0<br />

CAGR 2)<br />

4%<br />

25%<br />

65%<br />

10%<br />

32%<br />

33%<br />

102%<br />

VIE-1789-90000-017-415<br />

10

Shr<strong>in</strong>k<strong>in</strong>g marg<strong>in</strong>s will force banks to <strong>in</strong>crease<br />

operational efficiency – Croatian banks already <strong>in</strong><br />

good shape<br />

Average <strong>in</strong>terest spread Cost-Income Ratio, [%]<br />

25%<br />

20%<br />

15%<br />

10%<br />

5%<br />

0%<br />

20,6%<br />

12,7%<br />

7,6%<br />

7,2%<br />

17,2% 16,1%<br />

11,1% 11,0%<br />

8,8%<br />

6,6%<br />

7,7%<br />

7,3%<br />

14,7%<br />

13,7%<br />

9,1% 9,2%<br />

11,5%<br />

8.0%<br />

7,0% HR<br />

7.6%<br />

6.4% BG<br />

6,7% 6,6%<br />

5,9% PL<br />

2000 2001 2002 2003 2004 2005<br />

Notes: 1) Calculated for top 10 banks<br />

Source: National Banks, WOOD Company CEE Banks-" Manag<strong>in</strong>g South East"<br />

RO<br />

62.8%<br />

RO 1)<br />

61.0%<br />

58.9%<br />

56.7%<br />

PL SK BG<br />

53.3%<br />

HR<br />

50.5%<br />

HU<br />

46.3%<br />

CU<br />

45-50%<br />

EU best<br />

practice<br />

VIE-1789-90000-017-415<br />

11

B. Successful <strong>retail</strong> bank<strong>in</strong>g bus<strong>in</strong>ess models<br />

VIE-1789-90000-017-415<br />

12

CEE bank<strong>in</strong>g markets are sell<strong>in</strong>g markets, with a<br />

focus on expansion and less on cost management<br />

Key success factors<br />

1<br />

Strategy<br />

Position<strong>in</strong>g: Universal or<br />

niche bank?<br />

2 Distribution<br />

Alternative channels<br />

Network optimization and<br />

expansion<br />

3 Market<strong>in</strong>g & Sales<br />

effectiveness<br />

Market<strong>in</strong>g/ Communication<br />

Cross Sell<strong>in</strong>g<br />

Sales empowerment<br />

VIE-1789-90000-017-415<br />

13

Staff, strategy, market<strong>in</strong>g & sales, distribution are<br />

seen as key success factors <strong>in</strong> CEE<br />

Top success factors <strong>in</strong> CEE bank<strong>in</strong>g<br />

Staff<br />

Strategy<br />

Market<strong>in</strong>g & Sales<br />

Distribution network<br />

Speed/Time to market<br />

Pragmatism<br />

Customer base<br />

Risk management<br />

Front office processes<br />

Back office processes<br />

Cost management<br />

Products<br />

Internal organization<br />

IT<br />

8%<br />

8%<br />

12%<br />

19%<br />

19%<br />

25%<br />

25%<br />

25%<br />

31%<br />

38%<br />

50%<br />

58%<br />

58%<br />

Source: "Key factors for success of banks <strong>in</strong> CEE" by EFMA and zeb/<br />

77%<br />

Comments<br />

Staff: management talent is scarce<br />

Strategy: universal bank or niche<br />

bank<br />

Market<strong>in</strong>g & Sales: transform<br />

branch staff from adm<strong>in</strong>istrators<br />

<strong>in</strong>to sales-driven, customer oriented<br />

Distribution:<br />

– Usage of alternative channels is<br />

high <strong>in</strong> CEE<br />

– Modern trends regard<strong>in</strong>g branch<br />

locations: malls, supermarkets<br />

– Invest <strong>in</strong> branch expansion to<br />

close gap with EU <strong>in</strong> terms of<br />

branch density<br />

VIE-1789-90000-017-415<br />

14

STRATEGY<br />

Most banks offer universal services, but specialist<br />

and niche players have also proven successful…<br />

Market Position<strong>in</strong>g– CEE examples<br />

Broad<br />

Product<br />

portfolio<br />

Narrow<br />

Focused player Universal<br />

C D<br />

A B<br />

Niche player Product Specialist<br />

Narrow Distribution channel/segment Broad<br />

Comments<br />

A Niche player, with focus on few<br />

products and/or distribution<br />

channels with competitive advantage<br />

B Product specialist, with focus on<br />

few products, but extensive,<br />

<strong>in</strong>novative distribution channels<br />

C Focused player, on distribution<br />

channel/client segments with broad<br />

product portfolio<br />

D Universal bank, with a wide range<br />

of products and distribution channels<br />

VIE-1789-90000-017-415<br />

15

STRATEGY<br />

…which are sometimes <strong>in</strong>terim stages on the<br />

development path to become a universal <strong>retail</strong> bank<br />

Examples of implementation <strong>strategies</strong><br />

Broad<br />

Product<br />

portfolio<br />

Narrow<br />

Focused player Universal<br />

Niche player Product Specialist<br />

Narrow Distribution channel/segment Broad<br />

Implementation <strong>strategies</strong><br />

2003: Offer basic account, loan an<br />

deposit through m<strong>in</strong>i branches –<br />

high market<strong>in</strong>g cost for brand<strong>in</strong>g<br />

2004: Offer mortgage loan products of<br />

other banks (3rd party provider)<br />

2005: Develop <strong>in</strong>ternet offer, credit cards<br />

Step 1: Consumer f<strong>in</strong>ance through POS<br />

Step 2: Usage of <strong>in</strong>termediaries<br />

Step 3: Own sales units/branches, offer<br />

deposits, enter micro companies<br />

segment<br />

VIE-1789-90000-017-415<br />

16

STRATEGY EXAMPLE<br />

Lukas bank of Poland focuses on consumer f<strong>in</strong>ance<br />

to build up a large customer base<br />

Product<br />

Installment loans to <strong>in</strong>dividual customers, for<br />

products and services purchase, cash and car<br />

loans, mortgage loan with a free of charge analysis<br />

of a loan application with<strong>in</strong> short period<br />

Target: mass clients, high number of clients over 50<br />

years – low risk group as far as loan repayment is<br />

concerned<br />

Plans to enter the segment of small enterprises<br />

Implementation of a new central IT system<br />

Customer<br />

Distribution<br />

Consumer f<strong>in</strong>ance<br />

(Credit Agricole)<br />

large customer base<br />

Branch location <strong>in</strong> the centers of large and smaller<br />

towns, areas close to shopp<strong>in</strong>g centers and block<br />

of flats settlements<br />

Co-operate with more than 31,000 shops, service<br />

po<strong>in</strong>ts and networks of big department stores<br />

where customers can buy and f<strong>in</strong>ance the goods<br />

Extensive promotional campaigns and high<br />

spend<strong>in</strong>g on market<strong>in</strong>g<br />

Substantial <strong>in</strong>crease of revenue and profitability <strong>in</strong><br />

2004; ROE 73%, net profit EUR 68 m<br />

Results<br />

VIE-1789-90000-017-415<br />

17

STRATEGY EXAMPLE<br />

Provident Polska focuses on the low <strong>in</strong>come<br />

segment and delivers cash loans at home<br />

Product<br />

Cash loan up to 1.250 EUR for max. 1 year, pure<br />

mono-l<strong>in</strong>e<br />

Competitive <strong>in</strong>terest rates, but very high<br />

commissions; high effective <strong>in</strong>terest rates (100-200%)<br />

Fast turnover, high marg<strong>in</strong>, low <strong>in</strong>terest rate risk –<br />

cash loans are small and short term<br />

Target: low <strong>in</strong>come segment<br />

Value proposition: Eas<strong>in</strong>ess of gett<strong>in</strong>g the cash<br />

loan – no bank account, no guarantors, relative fast<br />

(<strong>in</strong> 48 hours), only guarantee is the confirmation<br />

about salaries from last 3 months<br />

Customer<br />

Distribution<br />

Cash loans for the low<br />

<strong>in</strong>come segment<br />

Delivery and collection by representatives at<br />

customers' home<br />

Close contact with client through representatives<br />

Representatives´ commission based on collection<br />

Increas<strong>in</strong>g network of small purely sales offices<br />

(223) <strong>in</strong> the whole country<br />

Alternative approach to credit stand<strong>in</strong>g evaluation,<br />

base for the evaluation is the home of the client<br />

Simple, but effective risk management process<br />

(bad loans: market standard)<br />

Bad loans sold to companies specialized <strong>in</strong> the<br />

collection of receivables<br />

Risk Management<br />

VIE-1789-90000-017-415<br />

18

STRATEGY EXAMPLE<br />

Polish credit unions (SKOKs) are also successful <strong>in</strong><br />

tapp<strong>in</strong>g the lower <strong>in</strong>come segment<br />

Strategy<br />

Implementation<br />

Results<br />

Non-profit associations focus<strong>in</strong>g on simple products targeted to low<br />

<strong>in</strong>come customers (members) and rely<strong>in</strong>g on personal relationships <strong>in</strong> local community<br />

Favorable legal status for credit unions <strong>in</strong> Poland (no capital requirements, no <strong>in</strong>come tax until<br />

end 2006, etc.)<br />

Fast service through decentralized and simple processes<br />

Attractive pric<strong>in</strong>g<br />

Internal stabiliz<strong>in</strong>g fund and guarantee system<br />

New services: <strong>in</strong>vestment funds, life <strong>in</strong>surance, mortgage products<br />

Fast growth and <strong>in</strong>creased profitability <strong>in</strong> recent years<br />

One of the most successful concepts for provid<strong>in</strong>g services <strong>in</strong> sav<strong>in</strong>gs and deposit segment<br />

A new competitor for traditional banks<br />

Assets of SKOK now account for over EUR 1 bn<br />

The number of members grew by 29% annually reach<strong>in</strong>g 1,3 m members at the end of 2005<br />

The number of cash desks and branches at the end of 2005: > 1.500<br />

VIE-1789-90000-017-415<br />

19

STRATEGY EXAMPLE<br />

MultiBank built up its client base as an <strong>in</strong>ternet<br />

bank only – Outlets to support client acquisition<br />

Product<br />

Very <strong>in</strong>novative solution <strong>in</strong> the mortgage loan<br />

offer – mechanism of balanc<strong>in</strong>g the loan amount<br />

with client sav<strong>in</strong>gs with<strong>in</strong> the Multiplan<br />

High product flexibility – no fees required for early<br />

repayment and currency change<br />

Target: middle and affluent segment - clear<br />

separation of VIP clients (Aquarius Club) and small<br />

enterprises<br />

Customer<br />

Distribution<br />

Internet bank with<br />

branches for client<br />

acquisition<br />

Multichannel access to the current account –<br />

<strong>in</strong>ternet, branches (51), telephone bank<strong>in</strong>g, SMS,<br />

WAP<br />

Attractive branch style and equipment give clients<br />

the impression of high service quality and<br />

„closeness" to client<br />

Cooperation with the ma<strong>in</strong> <strong>in</strong>termediaries is<br />

centrally coord<strong>in</strong>ated – the bank cooperates mostly<br />

with big <strong>in</strong>termediaries – Expander, Open F<strong>in</strong>ance<br />

Promotion<br />

VIE-1789-90000-017-415<br />

20

STRATEGY EXAMPLE<br />

GE Money exploits full potential of customer needs<br />

via cross sell<strong>in</strong>g – Professional CRM program<br />

GE Capital Multiservis Czech Republic<br />

Basic Idea Realization by Multiservice<br />

Customer applies<br />

for sales f<strong>in</strong>ance<br />

account at POS<br />

to buy e.g.<br />

wash<strong>in</strong>g mach<strong>in</strong>e<br />

Once acquired<br />

customer gets<br />

"converted"<br />

Cross sell<strong>in</strong>g<br />

Customer life<br />

cycle program<br />

% of open<strong>in</strong>g balance<br />

100%<br />

90%<br />

80%<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

1<br />

2<br />

3<br />

Card issued: 4th-6th month<br />

4<br />

x-sell<br />

loans<br />

revolvers<br />

0%<br />

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46<br />

Month on file<br />

1<br />

2<br />

3<br />

4<br />

Drive customer<br />

acquisition by "sales<br />

f<strong>in</strong>ance loan"<br />

products<br />

Drive high conversion<br />

rate by automatic flip<br />

to revolv<strong>in</strong>g credit<br />

Drive revolv<strong>in</strong>g by<br />

strong cash card<br />

access functionality<br />

Drive x-sell and reactivation<br />

by targeted<br />

offers/ products<br />

VIE-1789-90000-017-415<br />

21

Key success factors<br />

1<br />

Strategy<br />

Position<strong>in</strong>g: Universal or<br />

niche bank?<br />

2 Distribution<br />

Alternative channels<br />

Network optimization and<br />

expansion<br />

3 Market<strong>in</strong>g & Sales<br />

effectiveness<br />

Market<strong>in</strong>g/ Communication<br />

Cross Sell<strong>in</strong>g<br />

Sales empowerment<br />

VIE-1789-90000-017-415<br />

22

DISTRIBUTION<br />

Alternative distribution channels offer a faster<br />

payback period with a lower <strong>in</strong>vestment<br />

Products and distribution channels – Assessment CEE<br />

Segments/<br />

products<br />

Investment/<br />

Insurance<br />

Mortgage loans<br />

Car loans<br />

Consumer loans<br />

Credit cards<br />

Deposits<br />

Investment level<br />

Size<br />

Low<br />

<strong>in</strong>vestments<br />

POS 3rd party/<br />

sales agents<br />

Low<br />

<strong>in</strong>vestments<br />

Comb<strong>in</strong>ations are difficult Comb<strong>in</strong>ations are possible<br />

M<strong>in</strong>i offices/<br />

sales outlets<br />

Medium<br />

<strong>in</strong>vestments<br />

Direct access<br />

Large <strong>in</strong>itial<br />

<strong>in</strong>vestments<br />

Standard<br />

branches<br />

Large<br />

<strong>in</strong>vestments<br />

VIE-1789-90000-017-415<br />

23

DISTRIBUTION<br />

Eurobank has a "Supermarket-Bank<strong>in</strong>g" branch<br />

format – small sales outlets <strong>in</strong> high traffic locations<br />

Example "m<strong>in</strong>i-office" Configuration "m<strong>in</strong>i-office"<br />

Information material<br />

ATM Sales person<br />

Needed space: 8-12 m 2<br />

ATM (about 50% with deposit function)<br />

2 work places with computer network access<br />

Place to provide <strong>in</strong>formation material<br />

Located <strong>in</strong> places with high visitor rate<br />

(supermarkets, shopp<strong>in</strong>g centers …)<br />

High market<strong>in</strong>g support of EUR 15 m (2004)<br />

resulted <strong>in</strong> >300,000 clients <strong>in</strong> 2 years<br />

Investments per "m<strong>in</strong>i-office"<br />

ATM with deposit function USD 15,000<br />

ATM without deposit function about USD<br />

5,000<br />

Other equipment for the office about USD<br />

15,000<br />

VIE-1789-90000-017-415<br />

24

DISTRIBUTION<br />

10% of all mortgage loans <strong>in</strong> the Polish market were<br />

granted by <strong>in</strong>termediation of Expander <strong>in</strong> 2004<br />

Expander: Independent F<strong>in</strong>ancial<br />

Intermediary<br />

Offer covers 90%<br />

mortgage<br />

loans <strong>in</strong> Poland<br />

Cooperation with<br />

20<br />

banks and 70<br />

<strong>in</strong>vestment funds<br />

Value of loans <strong>in</strong><br />

2004 USD 400 m<br />

21 branches<br />

<strong>in</strong> 13 cities;<br />

4 years on the<br />

market<br />

Average loan<br />

USD 40.000<br />

120 f<strong>in</strong>ancial<br />

consultants<br />

Comments<br />

Expander offers a full range of sales services<br />

for deposits, <strong>in</strong>surance and mortgage loans:<br />

<strong>in</strong> 2004 10% of all mortgage loans were<br />

granted by Expander<br />

It started <strong>in</strong> 2000 as an <strong>in</strong>ternet portal as the<br />

only distribution channel, evolv<strong>in</strong>g <strong>in</strong>to a<br />

traditional branch network of 23 outlets <strong>in</strong><br />

2005<br />

Expander was bought by the General Electric<br />

group <strong>in</strong> 2003<br />

Ma<strong>in</strong>ly middle class liv<strong>in</strong>g <strong>in</strong> big cities has<br />

used the services of Expander and its<br />

competitor "Open F<strong>in</strong>ance"; people with<br />

average salary for Poland (about USD 600)<br />

use their services<br />

VIE-1789-90000-017-415<br />

25

DISTRIBUTION<br />

Bank BPH is us<strong>in</strong>g franchis<strong>in</strong>g to expand its branch<br />

network <strong>in</strong> suburbs and small towns<br />

Outlets and<br />

development<br />

Product<br />

offer<br />

100 outlets ma<strong>in</strong>ly <strong>in</strong> three Voievodships (out of 16)<br />

Bank <strong>in</strong>tends to ga<strong>in</strong> <strong>in</strong> this way a closer access to the clients <strong>in</strong> the areas where the<br />

bank does not have its own branch network<br />

350 new outlets by the end of 2005, total number of 600 outlets by 2006<br />

90% of all <strong>retail</strong> products (sav<strong>in</strong>gs account, term deposits, credit cards, (cash) loans)<br />

Servic<strong>in</strong>g small bus<strong>in</strong>ess beg<strong>in</strong>n<strong>in</strong>g of 2006<br />

Organization Partner <strong>in</strong>curs all the <strong>in</strong>vestment costs connected to sett<strong>in</strong>g up the branch<br />

Partner employs staff and sets the level of salary<br />

Bank offers the tra<strong>in</strong><strong>in</strong>g for the partners open<strong>in</strong>g the outlets<br />

Break-even po<strong>in</strong>t reached as soon as after 3-6 months<br />

Partner receives part of the transaction fees generated by the branch<br />

Preferred locations: suburbs, large settlements of block of flats, shopp<strong>in</strong>g centers and<br />

centers of small towns<br />

All operations are carried out on-l<strong>in</strong>e and booked directly <strong>in</strong>to the system of the Bank<br />

VIE-1789-90000-017-415<br />

26

DISTRIBUTION<br />

PKO BP, the large sav<strong>in</strong>gs bank <strong>in</strong>creases access<br />

by the set up of agencies po<strong>in</strong>t of sale<br />

Outlets and<br />

development<br />

Product<br />

offer<br />

Organization<br />

Two types of agencies: so called ‘old’ type agencies – located <strong>in</strong> production plants<br />

and ‘new’ type agencies accessible to all customers: approx. 3,000 agencies<br />

Established ma<strong>in</strong>ly <strong>in</strong> small towns where PKO BP does not have their own branches<br />

and bigger cities <strong>in</strong> block of flat areas<br />

PKO BP plans to <strong>in</strong>crease the number of products and services available trough<br />

the agency (next to cash handl<strong>in</strong>g, open<strong>in</strong>g accounts, loan applications, etc.)<br />

Agencies realize around 20% of all cash operations with<strong>in</strong> the bank, 7% of sav<strong>in</strong>g<br />

accounts, <strong>in</strong>termediation <strong>in</strong> loan sale – 20,000 loans <strong>in</strong> value of EUR 70 m p.a. (2004)<br />

Agency functions <strong>in</strong> the name of and on behalf of the bank PKO BP<br />

A person <strong>in</strong>terested <strong>in</strong> open<strong>in</strong>g the agency has to be an entrepreneur (run a bus<strong>in</strong>ess)<br />

Decision concern<strong>in</strong>g sett<strong>in</strong>g up the agency is taken by the director of the<br />

regional <strong>retail</strong> department<br />

Agent must provide space for 1 cash teller, space for servic<strong>in</strong>g client with adequate<br />

safety measures (around 30 m 2 with 2 employees), and has to rent a POS term<strong>in</strong>al<br />

The average <strong>in</strong>vestment <strong>in</strong> the outlet amounts to ca. PLN 10,000<br />

PKO BP provides the agent with software, bank’s logo (free of charge), basic tra<strong>in</strong><strong>in</strong>g<br />

Agency cannot employ anyone without the bank’ s acceptance<br />

VIE-1789-90000-017-415<br />

27

Key success factors<br />

1<br />

Strategy<br />

Position<strong>in</strong>g: Universal or<br />

niche bank?<br />

2 Distribution<br />

Alternative channels<br />

Network optimization and<br />

expansion<br />

3 Market<strong>in</strong>g & Sales<br />

effectiveness<br />

Market<strong>in</strong>g/ Communication<br />

Cross Sell<strong>in</strong>g<br />

Sales empowerment<br />

VIE-1789-90000-017-415<br />

28

MARKETING AND SALES EFFECTIVENESS<br />

Lessons learned from Spanish banks: Market<strong>in</strong>g<br />

expenditure is l<strong>in</strong>ked to sales success<br />

Share of advertis<strong>in</strong>g and communication costs to<br />

all non-personnel costs [<strong>in</strong> %] 1)<br />

Average CIR<br />

<strong>retail</strong> segment<br />

Premises costs<br />

100 100<br />

17-23<br />

IT costs 16-26<br />

Advertis<strong>in</strong>g/<br />

Communication<br />

45% 76% 78% >80%<br />

...<br />

18-21<br />

Spanish<br />

banks<br />

20-31<br />

19-29<br />

6-10<br />

German<br />

banks<br />

Notes: 1) Sample of selected Spanish and German big banks, 2004<br />

...<br />

100<br />

25-33<br />

10-15<br />

...<br />

Polish<br />

banks<br />

100<br />

15-20<br />

8-12<br />

...<br />

1-4 10-15<br />

Croatian<br />

banks<br />

Comments<br />

Spanish banks have a high<br />

share of market<strong>in</strong>g and<br />

communication costs<br />

Effective <strong>in</strong>crease <strong>in</strong> brand<br />

recognition and sales<br />

(Product campaigns, special<br />

offers for target groups, etc.)<br />

Increase <strong>in</strong> market<strong>in</strong>g and<br />

advertis<strong>in</strong>g costs <strong>in</strong> the last<br />

few years (e.g. Santander<br />

+8% s<strong>in</strong>ce 2002) at the<br />

same time decrease <strong>in</strong><br />

other non-personnel cost<br />

(e.g. Santander -9% s<strong>in</strong>ce<br />

2002)<br />

VIE-1789-90000-017-415<br />

29

MARKETING AND SALES EFFECTIVENESS<br />

Cross-sell<strong>in</strong>g ratio is another important measure of<br />

sales effectiveness<br />

Cross-Sell<strong>in</strong>g Ratios of selected Spanish banks, 2004<br />

[<strong>retail</strong> segment] 1)<br />

3.3<br />

Banco<br />

Popular<br />

3.4 2)<br />

3.7<br />

3.9 2)<br />

Banesto Santander Banco BBVA<br />

Sabadell<br />

Notes: 1) Analyzed products: current account, deposits, mortgage loans,<br />

credit cards, consumer loans, <strong>in</strong>vestment funds, <strong>in</strong>surance etc. 2) 2002<br />

Source: Annual reports; Salomon Smith Barney<br />

4.5<br />

6.3<br />

Bank<strong>in</strong>ter<br />

Average of<br />

Croatian<br />

banks: < 2.5<br />

Comments<br />

Mortgage loans as anchor<br />

products for cross sell<strong>in</strong>g<br />

Example: Santander<br />

customers with mortgage<br />

loans have six products <strong>in</strong><br />

average<br />

Bank<strong>in</strong>ter value proposition:<br />

"Most <strong>in</strong>novative,<br />

highest quality, multichannel<br />

convenience,<br />

personalized services"<br />

based on anchor product<br />

mortgage loans<br />

Usage and development of<br />

sophisticated CRM-Tools<br />

VIE-1789-90000-017-415<br />

30

MARKETING AND SALES EFFECTIVENESS<br />

Variable remuneration for sales employees is a<br />

significant lever to support sales culture<br />

Variable remuneration for sales employees –<br />

EXAMPLES [%] 1)<br />

15-45<br />

Spanish<br />

banks<br />

Variable Fixed<br />

Notes:1) Example of selected Spanish, Polish and German banks (<strong>retail</strong> segment)<br />

2) Very few Polish banks have variable part up to 50% values only for full time employees<br />

Source: Company's <strong>in</strong>formation<br />

10-30<br />

Polish<br />

banks 2)<br />

5-15<br />

German<br />

banks<br />

15-25<br />

Croatian<br />

banks<br />

Comments<br />

Variable remuneration share<br />

for sales staff at Spanish<br />

banks is high (up to 45%) –<br />

significant driver of sales<br />

culture<br />

Example Santander<br />

– Collective targets (for<br />

example market share <strong>in</strong><br />

target customer groups)<br />

– Individual targets<br />

(dependent on specific<br />

employee profile)<br />

– Customer satisfaction/service<br />

(based on<br />

customer surveys every<br />

six months)<br />

VIE-1789-90000-017-415<br />

31

LJUBLJANA<br />

PRAGUE<br />

BELGRAD<br />

TALLINN<br />

RIGA<br />

VILNIUS<br />

WARSAW<br />

BRATISLAVA<br />

BUDAPEST<br />

ZAGREB<br />

ZAGREB<br />

BUCHAREST<br />

SOFIA<br />

C. Potential development of Croatian <strong>retail</strong><br />

bank<strong>in</strong>g<br />

VIE-1789-90000-017-415<br />

32

<strong>Growth</strong> <strong>in</strong> <strong>retail</strong> lend<strong>in</strong>g is expected to slow down,<br />

driven more by mortgage than consumer lend<strong>in</strong>g<br />

Outstand<strong>in</strong>g <strong>retail</strong> loans [EUR m]<br />

CAGR<br />

Retail<br />

lend<strong>in</strong>g<br />

% GDP<br />

Mortage<br />

Consumer<br />

24,0%<br />

5,787<br />

1,661<br />

4,126<br />

2002<br />

28,5%<br />

7,190<br />

2,202<br />

4,988<br />

2003<br />

Source: CEE Bank<strong>in</strong>g Sector Report 2005<br />

20% 17%<br />

31,5%<br />

8,533<br />

2,797<br />

5,736<br />

37,8%<br />

11,022<br />

3,543<br />

7,479<br />

2004 2005E<br />

44,2%<br />

12,895<br />

4,145<br />

8,750<br />

2006E<br />

Comments<br />

Mortgage loans account for only 32%<br />

of <strong>retail</strong> loans <strong>in</strong> Croatia, while <strong>in</strong> the<br />

EU the percentage 80%<br />

Consumer f<strong>in</strong>ance boom fueled by<br />

strong demand for durables is<br />

expected to slow down due to<br />

restrictive National Bank measures,<br />

market saturation on certa<strong>in</strong><br />

segments, slow down <strong>in</strong> white goods<br />

demand<br />

VIE-1789-90000-017-415<br />

33

Banks have to f<strong>in</strong>d the right strategic position<strong>in</strong>g;<br />

not everyone can be a universal bank!<br />

Competitive bank<strong>in</strong>g environment<br />

Product<br />

+<br />

–<br />

Croatia<br />

–<br />

Focus Universal<br />

Banka Sonic<br />

Cost Saver/ Niche Product specialist<br />

= Asset size<br />

Splitska Banka<br />

OTP Bank<br />

Auto Banks<br />

Erste Bank<br />

HAAB<br />

Slavonska<br />

Distribution<br />

PB<br />

ZABA<br />

Raiffeisen<br />

Build<strong>in</strong>g societies<br />

Consumer f<strong>in</strong>ance<br />

+<br />

+<br />

Product<br />

–<br />

Eurozone/ Global Retail Bank<strong>in</strong>g<br />

Focus<br />

F<strong>in</strong>ancial<br />

advisors<br />

Self<br />

bank<strong>in</strong>g<br />

Brokers<br />

Mortgage<br />

brokers Niche banks<br />

–<br />

= Asset size<br />

Auto<br />

bank<br />

Universal<br />

Universal banks/<br />

f<strong>in</strong>ancial<br />

supermarket<br />

Private<br />

bank<br />

Mortgage<br />

banks<br />

Niche Product Specialist<br />

+<br />

Distribution<br />

VIE-1789-90000-017-415<br />

34

Branch density is at par with mature CEE bank<strong>in</strong>g<br />

markets<br />

Branch density [# per 100.000 <strong>in</strong>habitants] 1)<br />

H<br />

PL<br />

RO<br />

CZ<br />

HR<br />

UK<br />

FR<br />

IT<br />

DE<br />

ES<br />

11<br />

12<br />

15<br />

16<br />

18<br />

19<br />

44<br />

Notes: 1) Incl. cooperative banks, 2005<br />

52<br />

Source: National Central Banks; Bankscope<br />

58<br />

99<br />

Comments<br />

Low branch density relative to EU<br />

Plans for additional branches<br />

announced for 2006<br />

High potential to improve branch<br />

density and <strong>in</strong>crease revenue BUT<br />

<strong>in</strong>vestment and <strong>in</strong>novative branch<br />

concepts required<br />

VIE-1789-90000-017-415<br />

35

Alternative distribution channels offer a faster<br />

payback period with a lower <strong>in</strong>vestment<br />

Products and distribution channels – Assessment Croatia<br />

Segments/<br />

products<br />

Investment/<br />

Insurance<br />

Mortgage loans<br />

Car loans<br />

Consumer loans<br />

Credit cards<br />

Deposits<br />

Investment level<br />

Size<br />

Low<br />

<strong>in</strong>vestments<br />

POS 3rd party/<br />

sales agents<br />

Low<br />

<strong>in</strong>vestments<br />

Comb<strong>in</strong>ations are difficult Comb<strong>in</strong>ations are possible<br />

M<strong>in</strong>i offices/<br />

sales outlets<br />

Medium<br />

<strong>in</strong>vestments<br />

Direct access<br />

Large <strong>in</strong>itial<br />

<strong>in</strong>vestments<br />

High competition Low competition<br />

Standard<br />

branches<br />

Large<br />

<strong>in</strong>vestments<br />

VIE-1789-90000-017-415<br />

36

Credit cards and mortgages will be <strong>in</strong>creas<strong>in</strong>gly<br />

attractive for <strong>retail</strong> banks<br />

Market segment attractiveness overview<br />

<strong>Growth</strong> potential<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

Grow<strong>in</strong>g Attractiveness<br />

Leas<strong>in</strong>g<br />

Deposits<br />

Consumer lend<strong>in</strong>g<br />

Non-life <strong>in</strong>surance<br />

Corporate lend<strong>in</strong>g<br />

Credit<br />

Cards<br />

Mutual Funds<br />

Life <strong>in</strong>surance<br />

Market<br />

concentration<br />

Notes: Bubble size represents size of the bus<strong>in</strong>ess. Size of the cards bus<strong>in</strong>ess not def<strong>in</strong>ed.<br />

Market concentration measured by HHI (Herf<strong>in</strong>dhahl – Hirschmann) <strong>in</strong>dex from 0 to 1; 0 Represents low market concentration.<br />

Source: BACA, <strong>Roland</strong> <strong>Berger</strong> analysis<br />

Mortgage lend<strong>in</strong>g<br />

Low Medium High<br />

Comments<br />

Some product groups require<br />

more specialist know how such<br />

as <strong>in</strong>vestment products<br />

Credit cards expected to boom<br />

due to co-branded cards, an<br />

<strong>in</strong>creas<strong>in</strong>gly attractive market<strong>in</strong>g<br />

tool for <strong>retail</strong>ers and banks;<br />

smart cards and premium cards<br />

are promis<strong>in</strong>g niche segments<br />

VIE-1789-90000-017-415<br />

37

Levers to grow profitably – cheaper distribution,<br />

product <strong>in</strong>novation, sales effectiveness<br />

1. Choose the right<br />

strategic position<strong>in</strong>g<br />

2. Excellent client<br />

segmentation/focus on<br />

target groups<br />

Position<strong>in</strong>g as a universal bank only if significant market share can be achieved;<br />

otherwise pursue niches<br />

Development of new segments (e.g. low <strong>in</strong>come segment, agribus<strong>in</strong>ess)<br />

Focus on SME client segments<br />

3. Product Innovation Us<strong>in</strong>g one product as an anchor, then cross sell<br />

New <strong>in</strong>novative products (e.g. sav<strong>in</strong>gs+ mortgage loan)<br />

4. Optimize distribution Use alternative distribution channels via third party agents, m<strong>in</strong>i offices<br />

Customize branch format to target clients and location<br />

Periodically reevaluate branch locations<br />

5. Execution Increase of sales efficiency <strong>in</strong> <strong>in</strong>tegrated multi channel concept<br />

Strengthen<strong>in</strong>g of market<strong>in</strong>g/communication<br />

Increase of sales resources and cross sell<strong>in</strong>g leverage of sales channels<br />

Sales focus on performance (Incentives, activity controll<strong>in</strong>g, etc.)<br />

Tight processes; shorten<strong>in</strong>g response time<br />

Risk management<br />

VIE-1789-90000-017-415<br />

38

<strong>Roland</strong> <strong>Berger</strong> Strategy Consultants worldwide<br />

Amsterdam Barcelona Beij<strong>in</strong>g Berl<strong>in</strong> Brussels Bucharest Budapest Detroit Düsseldorf Frankfurt<br />

Hamburg Kiev Lisbon London Madrid Manama Milan Moscow Munich New York Paris Prague<br />

Riga Rome São Paulo Shanghai Stuttgart Tokyo Vienna Warsaw Zagreb Zurich<br />

<strong>Roland</strong> <strong>Berger</strong> Strategy Consultants d.o.o.<br />

Trg bana JelaSiTa 5<br />

10000 Zagreb<br />

Croatia<br />

VIE-1789-90000-017-415<br />

39