Econometria1-Transp-tema5-2

Econometria1-Transp-tema5-2

Econometria1-Transp-tema5-2

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

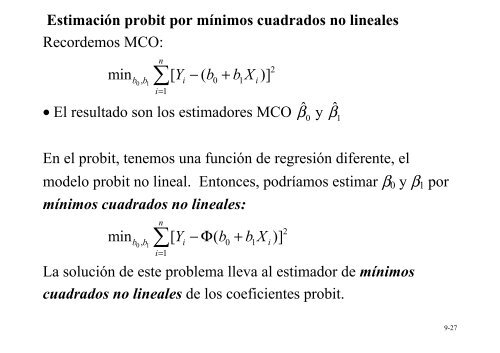

Estimación probit por mínimos cuadrados no lineales<br />

Recordemos MCO:<br />

n<br />

∑<br />

min [ Y − ( b + b X )]<br />

b0, b1 i 0 1 i<br />

i=<br />

1<br />

• El resultado son los estimadores MCO 0<br />

ˆ<br />

2<br />

ˆ β<br />

β y 1<br />

En el probit, tenemos una función de regresión diferente, el<br />

modelo probit no lineal. Entonces, podríamos estimar β0 y β1 por<br />

mínimos cuadrados no lineales:<br />

n<br />

∑<br />

min [ Y −Φ ( b + b X )]<br />

b0, b1 i 0 1 i<br />

i=<br />

1<br />

La solución de este problema lleva al estimador de mínimos<br />

cuadrados no lineales de los coeficientes probit.<br />

2<br />

9-27