Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Bénéfices</strong> <strong>de</strong> <strong>liquidation</strong> <strong>selon</strong> <strong>articles</strong> <strong>33b</strong> <strong>al</strong>. 2 <strong>LF</strong> <strong>et</strong> <strong>37b</strong> <strong>LIFD</strong><br />

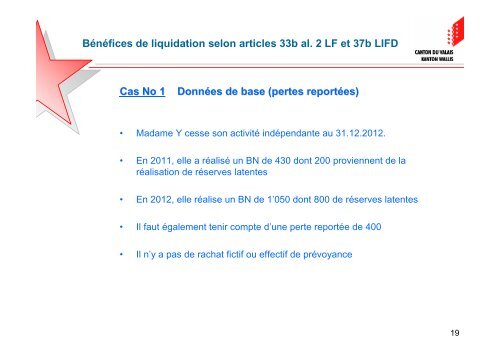

Cas No 1 Données <strong>de</strong> base (pertes reportées)<br />

• Madame Y cesse son activité indépendante au 31.12.2012.<br />

• En 2011, elle a ré<strong>al</strong>isé un BN <strong>de</strong> 430 dont 200 proviennent <strong>de</strong> la<br />

ré<strong>al</strong>isation <strong>de</strong> réserves latentes<br />

• En 2012, elle ré<strong>al</strong>ise un BN <strong>de</strong> 1’050 dont 800 <strong>de</strong> réserves latentes<br />

• Il faut ég<strong>al</strong>ement tenir compte d’une perte reportée <strong>de</strong> 400<br />

• Il n’y a pas <strong>de</strong> rachat fictif ou effectif <strong>de</strong> prévoyance<br />

19