Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

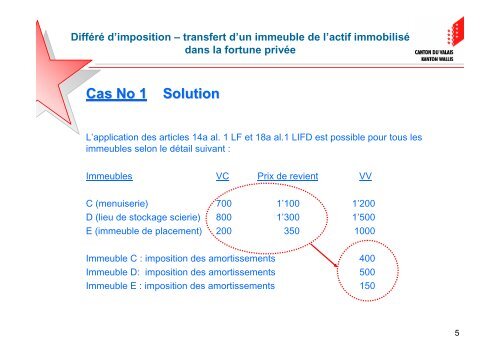

Différé d’imposition – transfert d’un immeuble <strong>de</strong> l’actif immobilisé<br />

dans la fortune privée<br />

Cas No 1 Solution<br />

L’application <strong>de</strong>s <strong>articles</strong> 14a <strong>al</strong>. 1 <strong>LF</strong> <strong>et</strong> 18a <strong>al</strong>.1 <strong>LIFD</strong> est possible pour tous les<br />

immeubles <strong>selon</strong> le détail suivant :<br />

Immeubles VC Prix <strong>de</strong> revient VV<br />

C (menuiserie) 700 1’100 1’200<br />

D (lieu <strong>de</strong> stockage scierie) 800 1’300 1’500<br />

E (immeuble <strong>de</strong> placement) 200 350 1000<br />

Immeuble C : imposition <strong>de</strong>s amortissements 400<br />

Immeuble D: imposition <strong>de</strong>s amortissements 500<br />

Immeuble E : imposition <strong>de</strong>s amortissements 150<br />

5