Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Bénéfices</strong> <strong>de</strong> <strong>liquidation</strong> <strong>selon</strong> <strong>articles</strong> <strong>33b</strong> <strong>al</strong>. 2 <strong>LF</strong> <strong>et</strong> <strong>37b</strong> <strong>LIFD</strong><br />

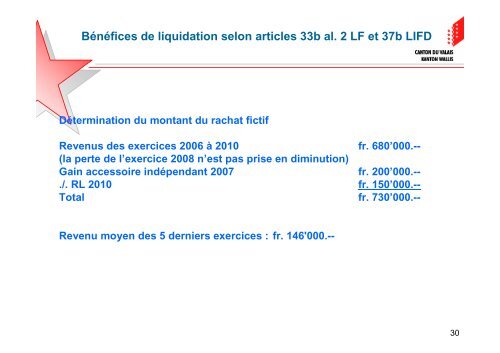

Détermination du montant du rachat fictif<br />

Revenus <strong>de</strong>s exercices 2006 à 2010 fr. 680’000.--<br />

(la perte <strong>de</strong> l’exercice 2008 n’est pas prise en diminution)<br />

Gain accessoire indépendant 2007 fr. 200’000.--<br />

./. RL 2010 fr. 150’000.--<br />

Tot<strong>al</strong> fr. 730’000.--<br />

Revenu moyen <strong>de</strong>s 5 <strong>de</strong>rniers exercices : fr. 146'000.--<br />

30