Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Bénéfices</strong> <strong>de</strong> <strong>liquidation</strong> <strong>selon</strong> <strong>articles</strong> <strong>33b</strong> <strong>al</strong>. 2 <strong>LF</strong> <strong>et</strong> <strong>37b</strong> <strong>LIFD</strong><br />

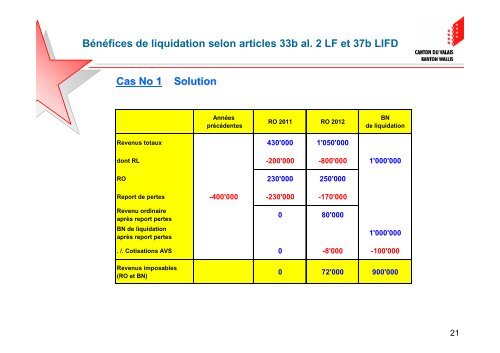

Cas No 1 Solution<br />

Années<br />

précé<strong>de</strong>ntes<br />

RO 2011 RO 2012<br />

Revenus totaux 430'000 1'050'000<br />

BN<br />

<strong>de</strong> <strong>liquidation</strong><br />

dont RL -200'000 -800'000 1'000'000<br />

RO 230'000 250'000<br />

Report <strong>de</strong> pertes -400'000 -230'000 -170'000<br />

Revenu ordinaire<br />

après report pertes<br />

BN <strong>de</strong> <strong>liquidation</strong><br />

après report pertes<br />

0 80'000<br />

1'000'000<br />

. /. Cotisations AVS 0 -8'000 -100'000<br />

Revenus imposables<br />

(RO <strong>et</strong> BN)<br />

0 72'000 900'000<br />

21