Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

Bénéfices de liquidation selon articles 33b al. 2 LF et 37b LIFD

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Bénéfices</strong> <strong>de</strong> <strong>liquidation</strong> <strong>selon</strong> <strong>articles</strong> <strong>33b</strong> <strong>al</strong>. 2 <strong>LF</strong> <strong>et</strong> <strong>37b</strong> <strong>LIFD</strong><br />

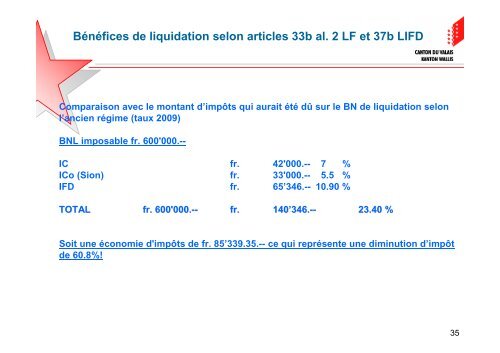

Comparaison avec le montant d’impôts qui aurait été dû sur le BN <strong>de</strong> <strong>liquidation</strong> <strong>selon</strong><br />

l’ancien régime (taux 2009)<br />

BNL imposable fr. 600'000.--<br />

IC fr. 42'000.-- 7 %<br />

ICo (Sion) fr. 33'000.-- 5.5 %<br />

IFD fr. 65’346.-- 10.90 %<br />

TOTAL fr. 600'000.-- 600'000. -- fr. 140’346.-- 140’346. -- 23.40 %<br />

Soit une économie d'impôts <strong>de</strong> fr. 85’339.35.-- ce qui représente une diminution d’impôt<br />

<strong>de</strong> 60.8%!<br />

35