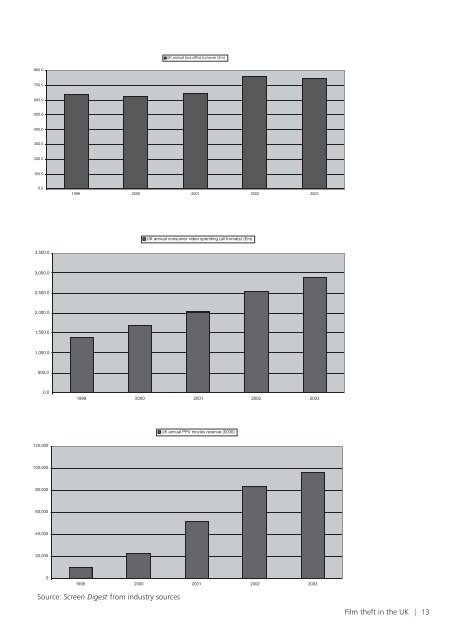

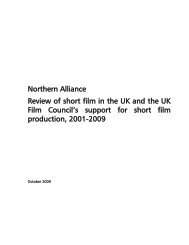

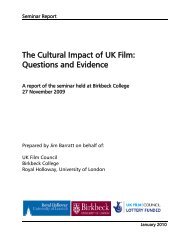

12 around 80% <strong>of</strong> total customers), mak<strong>in</strong>g its film service <strong>the</strong> most popular outside <strong>of</strong> <strong>the</strong> US. Free-to-air television is generally considered <strong>the</strong> f<strong>in</strong>al po<strong>in</strong>t <strong>in</strong> <strong>the</strong> value cha<strong>in</strong>, where films are broadcast on one <strong>of</strong> <strong>the</strong> five terrestrial TV channels. It is worth not<strong>in</strong>g that, while <strong>the</strong> grow<strong>in</strong>g revenues generated by <strong>the</strong> different distribution elements that comprise <strong>the</strong> <strong>UK</strong> film <strong>in</strong>dustry are impressive, <strong>the</strong>se gross numbers do not always translate <strong>in</strong>to similarly impressive pr<strong>of</strong>itability. Indeed, <strong>the</strong> economics <strong>of</strong> <strong>the</strong> <strong>in</strong>dustry can <strong>of</strong>ten be fragile, particularly as <strong>the</strong> cost side <strong>of</strong> <strong>the</strong> bus<strong>in</strong>ess cont<strong>in</strong>ues to escalate. From this perspective, <strong>the</strong> threat <strong>of</strong> piracy and <strong>the</strong> spectre <strong>of</strong> associated lost revenues is an especially worry<strong>in</strong>g prospect. <strong>Film</strong> piracy <strong>in</strong> <strong>the</strong> <strong>UK</strong> Piracy at any stage <strong>in</strong> this process can cause <strong>the</strong> film <strong>in</strong>dustry to susta<strong>in</strong> heavy f<strong>in</strong>ancial losses across <strong>the</strong> whole value cha<strong>in</strong>. If consumers are able to acquire and view a film title illegally, <strong>the</strong> <strong>in</strong>centive to see and acquire that film by legitimate means is diluted; whe<strong>the</strong>r <strong>in</strong> <strong>the</strong> c<strong>in</strong>ema, on DVD/video (rented or purchased), or pay-TV. Also, <strong>the</strong> logical extension <strong>of</strong> this argument is that <strong>the</strong> earlier <strong>the</strong> pirated copy appears <strong>in</strong> a film’s bus<strong>in</strong>ess lifecycle, <strong>the</strong> heavier <strong>the</strong> potential revenue loss is likely to be. Essentially, <strong>the</strong> earlier <strong>the</strong> act <strong>of</strong> piracy is, <strong>the</strong> greater is <strong>the</strong> number <strong>of</strong> ‘w<strong>in</strong>dows’ <strong>of</strong> exploitation that become vulnerable to dim<strong>in</strong>ished revenues. Physical piracy Physical piracy, as it stands at <strong>the</strong> moment, is <strong>the</strong> manufacture and distribution <strong>of</strong> illegally copied movies on ei<strong>the</strong>r videocassette or optical disc (ma<strong>in</strong>ly DVD, DVD-R and CD-R). These illegal copies are typically traded <strong>in</strong> high street shops (as ‘under <strong>the</strong> counter’ trade), on <strong>the</strong> Internet, <strong>in</strong> street markets and car boot sales, or by vendors operat<strong>in</strong>g on <strong>the</strong> street. Physical piracy is <strong>of</strong> particular concern to <strong>the</strong> movie <strong>in</strong>dustry, given that <strong>the</strong> home video market is <strong>the</strong> most lucrative s<strong>in</strong>gle w<strong>in</strong>dow <strong>in</strong> <strong>the</strong> film value cha<strong>in</strong>. There are two ma<strong>in</strong> sources for this type <strong>of</strong> piracy: • Pr<strong>of</strong>essional piracy operations • Consumer home copy<strong>in</strong>g Pr<strong>of</strong>essional piracy Large-scale pr<strong>of</strong>essional piracy, usually <strong>the</strong> doma<strong>in</strong> <strong>of</strong> organised crime, with pr<strong>of</strong>its be<strong>in</strong>g channelled <strong>in</strong>to o<strong>the</strong>r crim<strong>in</strong>al activities, has received considerable legal attention <strong>in</strong> recent years (exam<strong>in</strong>ed <strong>in</strong> <strong>the</strong> next chapter). The Asia Pacific region has been identified as a key base for import<strong>in</strong>g counterfeit films <strong>in</strong>to <strong>the</strong> <strong>UK</strong>. Accord<strong>in</strong>g to <strong>the</strong> Federation Aga<strong>in</strong>st <strong>Copyright</strong> Theft (FACT), <strong>the</strong> ma<strong>in</strong> sources <strong>of</strong> imported pirate DVDs <strong>in</strong> <strong>the</strong> <strong>UK</strong> are now Pakistan (36%), Malaysia (31%) and Ch<strong>in</strong>a (14%). Pakistan has now become one <strong>of</strong> <strong>the</strong> world’s lead<strong>in</strong>g exporters <strong>of</strong> pirate optical discs <strong>of</strong> all k<strong>in</strong>ds and is known to have eight illegal facilities <strong>in</strong> operation. In 2003, <strong>the</strong>se facilities produced upwards <strong>of</strong> 180 million discs, far <strong>in</strong> excess <strong>of</strong> local market demand. Pakistan’s sociogeographical position <strong>in</strong> <strong>the</strong> Middle East makes this <strong>of</strong> exceptional concern. Accord<strong>in</strong>g to local sources, optical disc piracy appears to be tak<strong>in</strong>g over from drug traffick<strong>in</strong>g as a low risk high yield source <strong>of</strong> revenue for crim<strong>in</strong>al elements <strong>in</strong> Pakistan and, accord<strong>in</strong>g to some sources, by <strong>in</strong>ternational terrorist groups. FACT representatives have stated that film piracy <strong>in</strong> London is believed to be feed<strong>in</strong>g Ch<strong>in</strong>ese organised crime and human traffick<strong>in</strong>g. More recently, Russia has jo<strong>in</strong>ed <strong>the</strong> ranks <strong>of</strong> those countries supply<strong>in</strong>g large amounts <strong>of</strong> illegal copies <strong>of</strong> films. The Motion Picture Association (MPA) has estimated that Russian

800.0 700.0 600.0 500.0 400.0 300.0 200.0 100.0 0.0 3,500.0 3,000.0 2,500.0 2,000.0 1,500.0 1,000.0 500.0 0.0 120,000 100,000 80,000 60,000 40,000 20,000 0 <strong>UK</strong> annual box <strong>of</strong>fice turnover (£m) 1999 2000 2001 2002 2003 <strong>UK</strong> annual consumer video spend<strong>in</strong>g (all formats) (£m) 1999 2000 2001 2002 2003 1999 2000 2001 2002 2003 Source: Screen Digest from <strong>in</strong>dustry sources <strong>UK</strong> annual PPV movies revenue (£000) <strong>Film</strong> <strong><strong>the</strong>ft</strong> <strong>in</strong> <strong>the</strong> <strong>UK</strong> | 13