Annual Report 2008-09 - Legal Services Commissioner

Annual Report 2008-09 - Legal Services Commissioner

Annual Report 2008-09 - Legal Services Commissioner

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

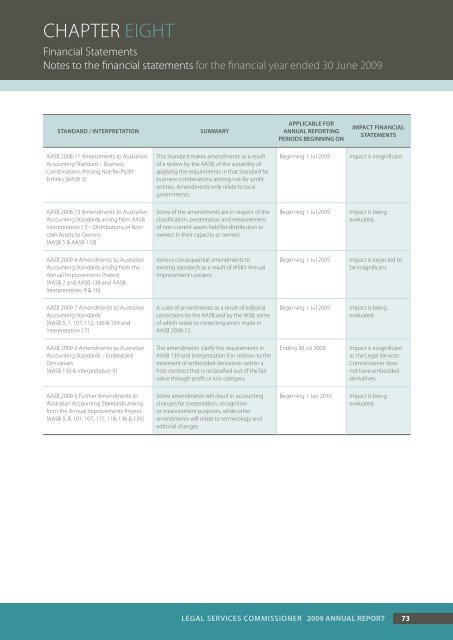

Chapter EIGHT<br />

Financial Statements<br />

Notes to the financial statements for the financial year ended 30 June 20<strong>09</strong><br />

Standard / Interpretation<br />

Summary<br />

Applicable for<br />

annual reporting<br />

periods beginning on<br />

Impact financial<br />

statements<br />

AASB <strong>2008</strong>-11 Amendments to Australian<br />

Accounting Standard – Business<br />

Combinations Among Not-for-Profit<br />

Entities [AASB 3]<br />

This Standard makes amendments as a result<br />

of a review by the AASB, of the suitability of<br />

applying the requirements in that Standard for<br />

business combinations among not-for-profit<br />

entities. Amendments only relate to local<br />

governments.<br />

Beginning 1 Jul 20<strong>09</strong><br />

Impact is insignificant.<br />

AASB <strong>2008</strong>-13 Amendments to Australian<br />

Accounting Standards arising from AASB<br />

Interpretation 17 – Distributions of Noncash<br />

Assets to Owners<br />

[AASB 5 & AASB 110]<br />

Some of the amendments are in respect of the<br />

classification, presentation and measurement<br />

of non-current assets held for distribution to<br />

owners in their capacity as owners<br />

Beginning 1 Jul 20<strong>09</strong><br />

Impact is being<br />

evaluated.<br />

AASB 20<strong>09</strong>-4 Amendments to Australian<br />

Accounting Standards arising from the<br />

<strong>Annual</strong> Improvements Project<br />

[AASB 2 and AASB 138 and AASB<br />

Interpretations 9 & 16]<br />

Various consequential amendments to<br />

existing standards as a result of IASB’s <strong>Annual</strong><br />

Improvement’s project.<br />

Beginning 1 Jul 20<strong>09</strong><br />

Impact is expected to<br />

be insignificant.<br />

AASB 20<strong>09</strong>-7 Amendments to Australian<br />

Accounting Standards<br />

[AASB 5, 7, 107, 112, 136 & 139 and<br />

Interpretation 17]<br />

A suite of amendments as a result of editorial<br />

corrections by the AASB and by the IASB, some<br />

of which relate to correcting errors made in<br />

AASB <strong>2008</strong>-12.<br />

Beginning 1 Jul 20<strong>09</strong><br />

Impact is being<br />

evaluated.<br />

AASB 20<strong>09</strong>-3 Amendments to Australian<br />

Accounting Standards – Embedded<br />

Derivatives<br />

[AASB 139 & Interpretation 9]<br />

The amendments clarify the requirements in<br />

AASB 139 and Interpretation 9 in relation to the<br />

treatment of embedded derivatives within a<br />

host contract that is reclassified out of the fair<br />

value through profit or loss category.<br />

Ending 30 Jul 20<strong>09</strong><br />

Impact is insignificant<br />

as the <strong>Legal</strong> <strong>Services</strong><br />

<strong>Commissioner</strong> does<br />

not have embedded<br />

derivatives.<br />

AASB 20<strong>09</strong>-5 Further Amendments to<br />

Australian Accounting Standards arising<br />

from the <strong>Annual</strong> Improvements Project<br />

[AASB 5, 8, 101, 107, 117, 118, 136 & 139]<br />

Some amendments will result in accounting<br />

changes for presentation, recognition<br />

or measurement purposes, while other<br />

amendments will relate to terminology and<br />

editorial changes.<br />

Beginning 1 Jan 2010<br />

Impact is being<br />

evaluated.<br />

<strong>Legal</strong> <strong>Services</strong> COMMISSIONER 20<strong>09</strong> <strong>Annual</strong> <strong>Report</strong> 73