comprehensive annual financial report - City of St. Petersburg

comprehensive annual financial report - City of St. Petersburg

comprehensive annual financial report - City of St. Petersburg

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

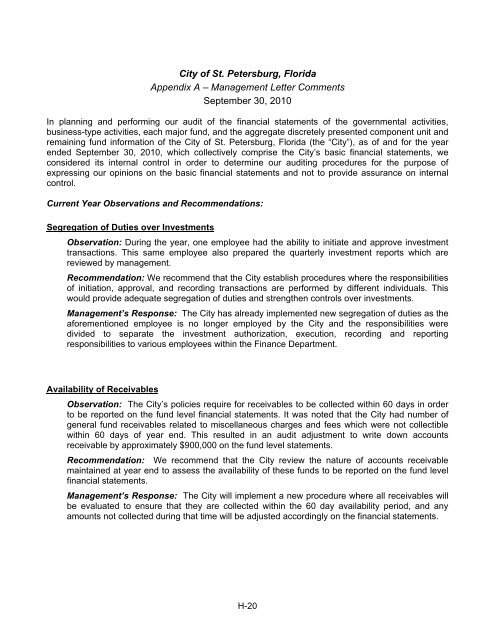

<strong>City</strong> <strong>of</strong> <strong>St</strong>. <strong>Petersburg</strong>, Florida<br />

Appendix A – Management Letter Comments<br />

September 30, 2010<br />

In planning and performing our audit <strong>of</strong> the <strong>financial</strong> statements <strong>of</strong> the governmental activities,<br />

business-type activities, each major fund, and the aggregate discretely presented component unit and<br />

remaining fund information <strong>of</strong> the <strong>City</strong> <strong>of</strong> <strong>St</strong>. <strong>Petersburg</strong>, Florida (the “<strong>City</strong>”), as <strong>of</strong> and for the year<br />

ended September 30, 2010, which collectively comprise the <strong>City</strong>’s basic <strong>financial</strong> statements, we<br />

considered its internal control in order to determine our auditing procedures for the purpose <strong>of</strong><br />

expressing our opinions on the basic <strong>financial</strong> statements and not to provide assurance on internal<br />

control.<br />

Current Year Observations and Recommendations:<br />

Segregation <strong>of</strong> Duties over Investments<br />

Observation: During the year, one employee had the ability to initiate and approve investment<br />

transactions. This same employee also prepared the quarterly investment <strong>report</strong>s which are<br />

reviewed by management.<br />

Recommendation: We recommend that the <strong>City</strong> establish procedures where the responsibilities<br />

<strong>of</strong> initiation, approval, and recording transactions are performed by different individuals. This<br />

would provide adequate segregation <strong>of</strong> duties and strengthen controls over investments.<br />

Management’s Response: The <strong>City</strong> has already implemented new segregation <strong>of</strong> duties as the<br />

aforementioned employee is no longer employed by the <strong>City</strong> and the responsibilities were<br />

divided to separate the investment authorization, execution, recording and <strong>report</strong>ing<br />

responsibilities to various employees within the Finance Department.<br />

Availability <strong>of</strong> Receivables<br />

Observation: The <strong>City</strong>’s policies require for receivables to be collected within 60 days in order<br />

to be <strong>report</strong>ed on the fund level <strong>financial</strong> statements. It was noted that the <strong>City</strong> had number <strong>of</strong><br />

general fund receivables related to miscellaneous charges and fees which were not collectible<br />

within 60 days <strong>of</strong> year end. This resulted in an audit adjustment to write down accounts<br />

receivable by approximately $900,000 on the fund level statements.<br />

Recommendation: We recommend that the <strong>City</strong> review the nature <strong>of</strong> accounts receivable<br />

maintained at year end to assess the availability <strong>of</strong> these funds to be <strong>report</strong>ed on the fund level<br />

<strong>financial</strong> statements.<br />

Management’s Response: The <strong>City</strong> will implement a new procedure where all receivables will<br />

be evaluated to ensure that they are collected within the 60 day availability period, and any<br />

amounts not collected during that time will be adjusted accordingly on the <strong>financial</strong> statements.<br />

H-20