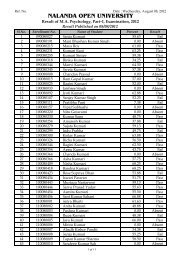

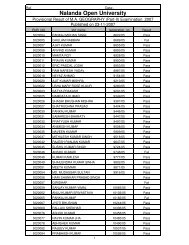

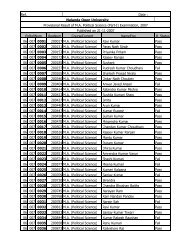

BABSc, B.Com & BCA Questions _III - Nalanda Open University

BABSc, B.Com & BCA Questions _III - Nalanda Open University

BABSc, B.Com & BCA Questions _III - Nalanda Open University

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

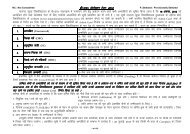

<strong>Nalanda</strong> <strong>Open</strong> <strong>University</strong><br />

Annual Exam-2010,<br />

Bachelor of <strong>Com</strong>merce, Hons<br />

(Cost Accounting)<br />

Part-<strong>III</strong>, Paper-V<br />

Time: 3Hrs Full Marks: 70<br />

Answer any five questions. All questions are of equal value.<br />

fdUgha ik¡p iz'uksa dk mÙkj nsa A lHkh iz'uksa ds vad leku gSa A<br />

1- ykxr ys[kkadu D;k gS\ foÙkh; ys[kkadu ls ;g fdl izdkj fHkUu gS\<br />

What is Cost Accounting? How does it differ from Financial Accounting?<br />

2- Hk.Mkj ls fuxZfer lkexzh ds ewY;kadu dh fofHkUu fof/k;ksa dk o.kZu djsa A<br />

Describe the different methods of pricing of Materials issued from store.<br />

3- ykxr lek/kku fooj.k ls vki D;k le>rs gSa\ ykxr ys[kk vkSj foÙkh; ys[kk }kjk iznf'kZr<br />

ykHkksa esa vUrj ds dkSu&dkSu ls dkj.k gks ldrs gSa\<br />

What do you mean by Cost Reconciliation statement? What can be the causes of<br />

difference in Profit shown by Cost Acconunt.<br />

4- ,d vPNh ikfjJfed iz.kkyh dh izeq[k ckrsa D;k gSa\<br />

What are the essential features of a good wage system.<br />

5- fuEufyf[kr esa ls fdUgha rhu ij fVIi.kh fy[kasz&<br />

Write notes on any three of the following:<br />

¼d½ fufonk ewY; (Tender Price)<br />

¼[k½ fcu dkMZ (Bin-Card)<br />

¼x½ vlkekU; dqw'kyrk (Abnormal efficiency or effectiveness)<br />

¼?k½ fdz;ek.k dk;Z (Work-in-progress)<br />

6- fuEufyf[kr fooj.kksa ls mRiknu [kkrk rS;kj djsa A izfr oLrq ykxr Hkh fn[kkoas ;fn<br />

mRikfnr oLrqvksa dh la[;k 6000 gS A<br />

Prepare a production Account showing Cost per article if the number of articles<br />

produced is 6,000:-<br />

Rs.<br />

Stocks of Materials at end (lkexzh LVkWd vUr esa½ 13]000<br />

Stocks of Materials at start ¼lkexzh LVkWd izkjaHk esa½ 11]000<br />

Purchase of Materials ¼lkexzh dk dz;½ 63]500<br />

Sale of Materials ¼lkexzh dk fodz;½ 1]500<br />

Materials Resersed ¼vkjf{kr lkexzh½ 1]600<br />

Wages ¼ikfjJfed½ 49]400<br />

Manufacturing Expenses ¼fuekZ.k O;;½ 7]800<br />

Work-in-Progress at start ¼fdz;ek.k dk;Z vkjaHk esa½ 4]000<br />

Work-in-progress at end ¼fdz;ek.k dk;Z vUr esa½ 3]000<br />

7- vlk/kkj.k {k; vkSj vlk/kkj.k cpr dk D;k vFkZ gS\ bUgsa izfdz;k ykxr [kkrk esa fdl<br />

izdkj fn[kk;k tkrk gS\ mnkgj.k nsa A<br />

What do yo mean by Abnormal wastage and Abnormal effectiveness? How they are<br />

treated in process Cost Accounts?