Community - GolfBusiness

Community - GolfBusiness

Community - GolfBusiness

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

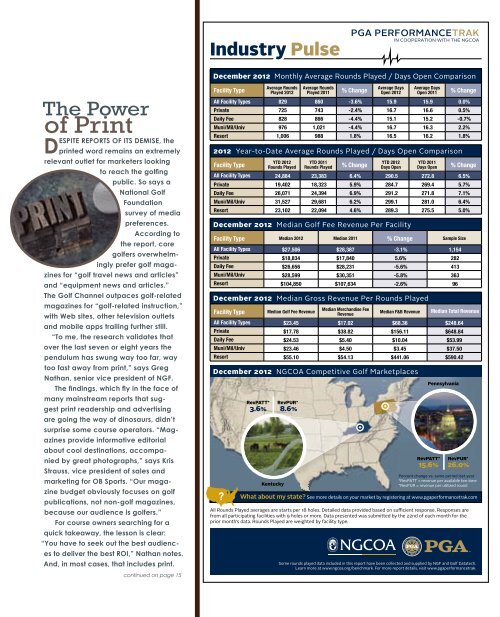

Industry Pulse<br />

December 2012 Monthly Average Rounds Played / Days Open Comparison<br />

The Power<br />

of Print<br />

D<br />

ESPITE REPORTS OF ITS DEMISE, the<br />

printed word remains an extremely<br />

relevant outlet for marketers looking<br />

to reach the golfing<br />

public. So says a<br />

National Golf<br />

Foundation<br />

survey of media<br />

preferences.<br />

According to<br />

the report, core<br />

golfers overwhelmingly<br />

prefer golf magazines<br />

for “golf travel news and articles”<br />

and “equipment news and articles.”<br />

The Golf Channel outpaces golf-related<br />

magazines for “golf-related instruction,”<br />

with Web sites, other television outlets<br />

and mobile apps trailing further still.<br />

“To me, the research validates that<br />

over the last seven or eight years the<br />

pendulum has swung way too far, way<br />

too fast away from print,” says Greg<br />

Nathan, senior vice president of NGF.<br />

The findings, which fly in the face of<br />

many mainstream reports that suggest<br />

print readership and advertising<br />

are going the way of dinosaurs, didn’t<br />

surprise some course operators. “Magazines<br />

provide informative editorial<br />

about cool destinations, accompanied<br />

by great photographs,” says Kris<br />

Strauss, vice president of sales and<br />

marketing for OB Sports. “Our magazine<br />

budget obviously focuses on golf<br />

publications, not non-golf magazines,<br />

because our audience is golfers.”<br />

For course owners searching for a<br />

quick takeaway, the lesson is clear:<br />

“You have to seek out the best audiences<br />

to deliver the best ROI,” Nathan notes.<br />

And, in most cases, that includes print.<br />

continued on page 15<br />

Facility Type<br />

% Change<br />

% Change<br />

Average Rounds Average Rounds<br />

Average Days Average Days<br />

Played 2012 Played 2011<br />

Open 2012 Open 2011<br />

All Facility Types 829 860 -3.6% 15.9 15.9 0.0%<br />

Private 725 743 -2.4% 16.7 16.6 0.5%<br />

Daily Fee 828 866 -4.4% 15.1 15.2 -0.7%<br />

Muni/Mil/Univ 976 1,021 -4.4% 16.7 16.3 2.2%<br />

Resort 1,006 988 1.8% 16.5 16.2 1.8%<br />

2012 Year-to-Date Average Rounds Played / Days Open Comparison<br />

Facility Type<br />

% Change<br />

% Change<br />

YTD 2012<br />

YTD 2011<br />

YTD 2012<br />

YTD 2011<br />

Rounds Played Rounds Played<br />

Days Open Days Open<br />

All Facility Types 24,884 23,383 6.4% 290.5 272.8 6.5%<br />

Private 19,402 18,323 5.9% 284.7 269.4 5.7%<br />

Daily Fee 26,071 24,394 6.9% 291.2 271.8 7.1%<br />

Muni/Mil/Univ 31,527 29,681 6.2% 299.1 281.0 6.4%<br />

Resort 23,102 22,094 4.6% 289.3 275.5 5.0%<br />

December 2012 Median Golf Fee Revenue Per Facility<br />

Facility Type Median 2012 Median 2011 % Change Sample Size<br />

All Facility Types $27,506 $28,387 -3.1% 1,154<br />

Private $18,834 $17,840 5.6% 282<br />

Daily Fee $26,656 $28,231 -5.6% 413<br />

Muni/Mil/Univ $28,599 $30,351 -5.8% 363<br />

Resort $104,850 $107,634 -2.6% 96<br />

December 2012 Median Gross Revenue Per Rounds Played<br />

Median Merchandise Fee<br />

Facility Type<br />

Median Golf Fee Revenue<br />

Median F&B Revenue<br />

Revenue<br />

Median Total Revenue<br />

All Facility Types $23.45 $17.02 $68.36 $248.64<br />

Private $17.78 $38.82 $156.11 $648.84<br />

Daily Fee $24.53 $5.40 $10.04 $53.99<br />

Muni/Mil/Univ $23.46 $4.50 $3.45 $37.50<br />

Resort $55.10 $54.13 $441.06 $590.42<br />

December 2012 NGCOA Competitive Golf Marketplaces<br />

RevPATT*<br />

3.6%<br />

Kentucky<br />

RevPUR*<br />

8.6%<br />

Pennsylvania<br />

RevPATT*<br />

RevPUR*<br />

15.6% 26.0%<br />

Percent change vs. same period last year<br />

*RevPATT = revenue per available tee-time<br />

*RevPUR = revenue per utilized round<br />

What about my state See more details on your market by registering at www.pgaperformancetrak.com<br />

All Rounds Played averages are starts per 18 holes. Detailed data provided based on sufficient response. Responses are<br />

from all participating facilities with 9 holes or more. Data presented was submitted by the 22nd of each month for the<br />

prior month’s data. Rounds Played are weighted by facility type.<br />

Some rounds played data included in this report have been collected and supplied by NGF and Golf Datatech.<br />

Learn more at www.ngcoa.org/benchmark. For more report details, visit www.pgaperformancetrak.