Volume I: Investment Prospectus Rwanda Electricity Sector Access ...

Volume I: Investment Prospectus Rwanda Electricity Sector Access ...

Volume I: Investment Prospectus Rwanda Electricity Sector Access ...

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

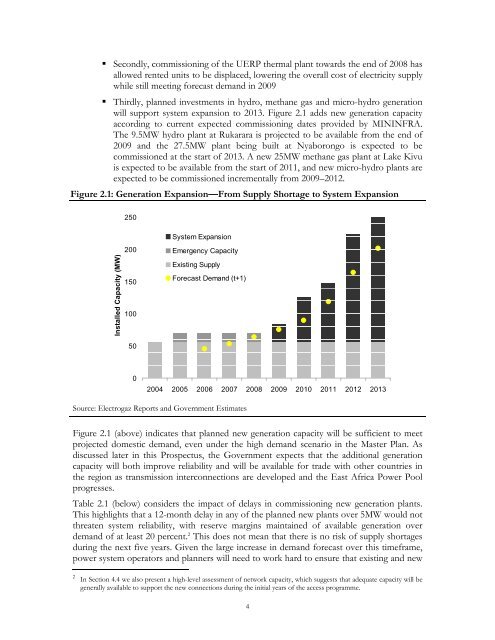

• Secondly, commissioning of the UERP thermal plant towards the end of 2008 hasallowed rented units to be displaced, lowering the overall cost of electricity supplywhile still meeting forecast demand in 2009• Thirdly, planned investments in hydro, methane gas and micro-hydro generationwill support system expansion to 2013. Figure 2.1 adds new generation capacityaccording to current expected commissioning dates provided by MININFRA.The 9.5MW hydro plant at Rukarara is projected to be available from the end of2009 and the 27.5MW plant being built at Nyaborongo is expected to becommissioned at the start of 2013. A new 25MW methane gas plant at Lake Kivuis expected to be available from the start of 2011, and new micro-hydro plants areexpected to be commissioned incrementally from 2009–2012.Figure 2.1: Generation Expansion—From Supply Shortage to System Expansion250Installed Capacity (MW)200150100System ExpansionEmergency CapacityExisting SupplyForecast Demand (t+1)5002004 2005 2006 2007 2008 2009 2010 2011 2012 2013Source: Electrogaz Reports and Government EstimatesFigure 2.1 (above) indicates that planned new generation capacity will be sufficient to meetprojected domestic demand, even under the high demand scenario in the Master Plan. Asdiscussed later in this <strong>Prospectus</strong>, the Government expects that the additional generationcapacity will both improve reliability and will be available for trade with other countries inthe region as transmission interconnections are developed and the East Africa Power Poolprogresses.Table 2.1 (below) considers the impact of delays in commissioning new generation plants.This highlights that a 12-month delay in any of the planned new plants over 5MW would notthreaten system reliability, with reserve margins maintained of available generation overdemand of at least 20 percent. 2 This does not mean that there is no risk of supply shortagesduring the next five years. Given the large increase in demand forecast over this timeframe,power system operators and planners will need to work hard to ensure that existing and new2In Section 4.4 we also present a high-level assessment of network capacity, which suggests that adequate capacity will begenerally available to support the new connections during the initial years of the access programme.4