- Page 2 and 3: THE UNIVERSITY OF HONG KONGLIBRARIE

- Page 4 and 5: VI- . .7 « i8^p ! ««^^OOSHSlVCJ

- Page 6 and 7: Ever since derivatives took centre-

- Page 8 and 9: denominator, value at risk, which c

- Page 10 and 11: the kind of information that superv

- Page 12 and 13: This book is a team effort of the H

- Page 14 and 15: While most market participants defi

- Page 16 and 17: of this investment is 6.32 percent

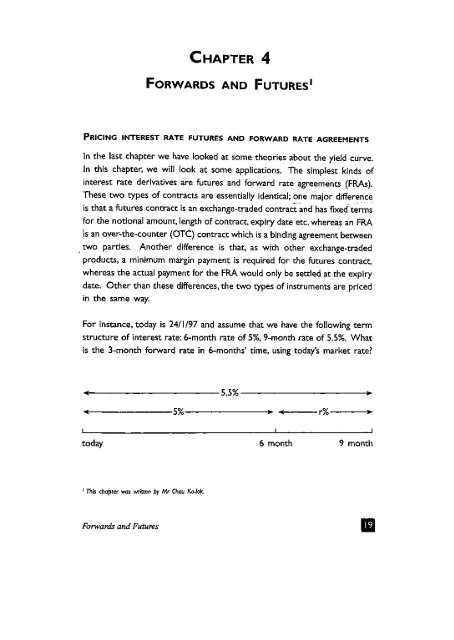

- Page 18 and 19: Mathematically, the relation betwee

- Page 20 and 21: $10,000. (For simplification of pre

- Page 22 and 23: Hong Kong does go up and the HSI ri

- Page 24 and 25: 3OF ATHEPRICING OF A FORWARD CONTRA

- Page 26 and 27: COST OF CARRYIn the above example,

- Page 28 and 29: interest rate swap rates. From thes

- Page 32 and 33: Again we use our method of having t

- Page 34 and 35: ates, the forward rate for the peri

- Page 36 and 37: 5In this chapter, we will discuss w

- Page 38 and 39: often complain that there is too mu

- Page 40 and 41: ABC also has three cash flows:1. It

- Page 42 and 43: Assuming that there is no transacti

- Page 44 and 45: simulation techniques and mathemati

- Page 46 and 47: The calculation of credit risk proc

- Page 48 and 49: The payments are exchanged every th

- Page 50 and 51: the reference rate. When this type

- Page 52 and 53: Effectively this is just a 2-year s

- Page 54 and 55: This measure of duration is referre

- Page 56 and 57: analysis, it also has its shortcomi

- Page 58 and 59: Percentage change in price due to d

- Page 60 and 61: 8OFOptions are generally perceived

- Page 62 and 63: OPTION'S PAYOFF PATTERNWhat about a

- Page 64 and 65: Volatility is the most important fa

- Page 66 and 67: fANDTrading options becomes more po

- Page 68 and 69: You need to hold 7 shares of stock

- Page 70 and 71: di = [ln(IOO/IOO) + (0.06 + O.P/2)

- Page 72 and 73: is10In the previous chapter, we dis

- Page 74 and 75: stock will go up in the near future

- Page 76 and 77: If the stock price of A continues t

- Page 78 and 79: OF AN11In the previous two chapters

- Page 80 and 81:

at-the-money option approaches its

- Page 82 and 83:

12Mortgage-backed securities (MBS)

- Page 84 and 85:

NEGATIVE CONVEXITYFor MBS, there is

- Page 86 and 87:

MULTI-CLASSIn 1983, Freddie Mac int

- Page 88 and 89:

13What is a hedge? According to the

- Page 90 and 91:

management to enter into swap and o

- Page 92 and 93:

transaction. For this criterion to

- Page 94 and 95:

CREDIT DEFAULT SWAPThe simplest for

- Page 96 and 97:

APPLICATION OF CREDIT DERIVATIVESYo

- Page 98 and 99:

in the US. Equally innovative, cred

- Page 100 and 101:

THE VARIANCE-COVARIANCE METHODThe t

- Page 102 and 103:

"cell" would have a cash flow expos

- Page 104 and 105:

Daily profit and loss ranked in asc

- Page 106 and 107:

of the market factor. Through this

- Page 108 and 109:

3. Most value at risk models use hi

- Page 110 and 111:

16ANDIn Chapter 5, we talked about

- Page 112 and 113:

price) of 9,000. For this transacti

- Page 114 and 115:

and the June 3-month futures rate i

- Page 116 and 117:

needs to take the necessary busines

- Page 118 and 119:

ief, the policies and procedures sh

- Page 120 and 121:

The derivatives industry can be com

- Page 122 and 123:

ANDONOFINTRODUCTION1. The Monetary

- Page 124 and 125:

MANAGEMENT AND CORPORATE5. As the B

- Page 126 and 127:

ensure that there is sufficient awa

- Page 128 and 129:

15. Branches of foreign banks which

- Page 130 and 131:

20. Where the institution considers

- Page 132 and 133:

RISK MEASUREMENT25. Having identifi

- Page 134 and 135:

) the tendency of the relevant mark

- Page 136 and 137:

38. The measurement of the market r

- Page 138 and 139:

market, credit and liquidity risk o

- Page 140 and 141:

Consideration must be given to the

- Page 142 and 143:

55. As noted earlier, the market or

- Page 144 and 145:

changes in portfolio value;d) the r

- Page 146 and 147:

66. A basic and essential safeguard

- Page 148 and 149:

73. It is essential that the intern

- Page 150 and 151:

Market liquidity risk is the risk t

- Page 152 and 153:

Furthermore, contracts with the sam

- Page 154 and 155:

There are three main VAR approaches

- Page 156 and 157:

Options risk should be captured; ri

- Page 158 and 159:

Annex D1. NOTIONAL OR VOLUME LIMITS

- Page 160 and 161:

assumptions on which they are based

- Page 162 and 163:

* There should be a unit independen

- Page 164 and 165:

- the customer had specifically req

- Page 166 and 167:

addition and deletion of operators,

- Page 168 and 169:

• Profits and losses resulting fr

- Page 170 and 171:

This book is due for return or rene