企 業 應 收 帳 款 與 授 信 決 策 關 係 之 研 究

ä¼æ¥ææ¶å¸³æ¬¾èæ信決çéä¿ä¹ç 究 - ä¸å°ä¼æ¥ä¿¡ç¨ä¿èåºé

ä¼æ¥ææ¶å¸³æ¬¾èæ信決çéä¿ä¹ç 究 - ä¸å°ä¼æ¥ä¿¡ç¨ä¿èåºé

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> <strong>關</strong> <strong>係</strong> <strong>之</strong> <strong>研</strong> <strong>究</strong>pp. 01-20<strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> <strong>關</strong> <strong>係</strong> <strong>之</strong> <strong>研</strong> <strong>究</strong>1鄭 鴻 章摘 要本 論 文 建 立 一 經 濟 理 論 分 析 模 型 , 從 <strong>企</strong> <strong>業</strong> 的 <strong>授</strong> <strong>信</strong> 管 理 角 度 , 分 析 <strong>企</strong> <strong>業</strong> 在 追 求 最 大淨 利 潤 目 標 下 , 採 取 <strong>信</strong> 用 交 易 方 式 <strong>之</strong> 最 適 <strong>授</strong> <strong>信</strong> 金 額 及 最 適 償 債 期 限 條 件 <strong>與</strong> 最 佳 <strong>授</strong> <strong>信</strong> 對象 選 擇 <strong>之</strong> 資 訊 需 求 <strong>決</strong> <strong>策</strong> 。 本 文 發 現 :(1) 滿 足 最 適 <strong>授</strong> <strong>信</strong> 金 額 <strong>之</strong> 條 件 是 當 變 動 <strong>授</strong> <strong>信</strong> 金 額<strong>之</strong> 邊 際 實 <strong>收</strong> 入 利 潤 等 於 其 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 ,(2) 滿 足 最 適 償 債 期 限 <strong>之</strong> 條 件 是 當 變 動 償債 期 限 <strong>之</strong> 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 利 潤 等 於 其 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 ,(3) 滿 足 最 適 資 訊 需 求 量 的 條件 是 當 <strong>信</strong> 用 資 訊 <strong>之</strong> 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 額 等 於 所 使 用 <strong>之</strong> <strong>信</strong> 用 資 訊 價 格 時 <strong>之</strong> 資 訊 量 。<strong>關</strong> 鍵 詞 : 現 金 交 易 、 <strong>信</strong> 用 交 易 、 交 易 成 本 、 <strong>信</strong> 用 交 易 風 險 、 最 適 <strong>授</strong> <strong>信</strong> 金 額 、最 適 償 債 期 限壹 、 前 言一 般 而 言 , 人 類 社 會 中 的 交 易 活 動 乃 是 市 場 經 濟 制 度 中 最 主 要 的 經 濟 活 動 <strong>之</strong> 一 ,而 所 謂 交 易 <strong>係</strong> 指 買 賣 雙 方 對 於 交 易 條 件 達 成 協 議 後 所 進 行 <strong>之</strong> 商 <strong>業</strong> 經 濟 活 動 , 交 易 雙 方各 自 依 據 協 議 條 件 履 行 義 務 。 其 中 交 易 條 件 是 指 交 易 價 格 、 交 易 數 量 、 交 貨 時 間 <strong>與</strong> 地點 、 付 <strong>款</strong> 時 間 及 地 點 等 雙 方 交 易 的 方 式 。 由 此 可 見 , 交 易 方 式 乃 構 成 交 易 條 件 的 主 要部 份 。 現 代 經 濟 社 會 買 賣 雙 方 主 要 的 交 易 方 式 大 致 又 可 區 分 為 現 金 交 易 及 <strong>信</strong> 用 交 易 兩種 。 早 期 人 類 社 會 <strong>之</strong> 間 的 經 濟 交 易 <strong>係</strong> 以 現 金 交 易 為 主 , 其 後 <strong>信</strong> 用 交 易 普 遍 受 到 買 賣 雙方 的 歡 迎 , 甚 至 於 逐 漸 取 代 現 金 交 易 而 成 為 現 代 經 濟 社 會 盛 行 的 主 流 交 易 方 式 。 這 是因 為 在 一 個 工 商 <strong>業</strong> 高 度 發 達 的 經 濟 體 系 裡 ,「 <strong>信</strong> 用 」(credit) 扮 演 著 重 要 角 色 , 其 不但 可 提 高 交 易 完 成 的 效 率 , 同 時 也 具 有 加 速 經 濟 發 展 的 功 能 。 尤 其 是 在 當 前 跨 國 交 易頻 繁 的 時 代 裡 , <strong>信</strong> 用 交 易 更 可 完 成 在 現 金 交 易 方 式 限 制 下 無 法 完 成 的 買 賣 清 算 作 <strong>業</strong> 。1國 立 政 治 大 學 國 際 經 營 <strong>與</strong> 貿 易 學 系 副 教 <strong>授</strong> 。1

第 11 期我 們 特 別 強 調 「 <strong>信</strong> 用 」 的 經 濟 功 能 , 但 問 題 是 , 何 謂 「 <strong>信</strong> 用 」? 一 般 而 言 , <strong>信</strong> 用 是 一種 付 <strong>款</strong> 的 承 諾 ,Hair (1992) 將 <strong>信</strong> 用 定 義 為 , 藉 由 允 諾 在 未 來 某 一 特 定 期 限 內 償 還 財物 , 促 使 目 前 可 獲 得 商 品 、 勞 務 、 服 務 的 力 量 ; 而 此 一 力 量 <strong>之</strong> 來 源 乃 是 以 <strong>信</strong> 任 為 基礎 。 陳 肇 榮 (1985) 定 義 , <strong>信</strong> 用 就 是 先 行 取 得 或 給 予 一 些 經 濟 價 值 , 然 後 在 經 過 一 段 時間 <strong>之</strong> 後 <strong>收</strong> 回 或 償 還 經 濟 價 值 的 一 種 行 為 。 葉 邱 南 (1996) 則 將 <strong>信</strong> 用 定 義 為 , 一 種 有 限 性的 交 易 媒 介 <strong>與</strong> 一 種 付 <strong>款</strong> 的 承 諾 。 <strong>授</strong> <strong>信</strong> 者 根 據 被 <strong>授</strong> <strong>信</strong> 者 的 財 力 、 人 品 、 生 活 習 慣 、 過 去償 債 記 錄 等 來 評 斷 其 <strong>信</strong> 用 可 靠 度 , 以 <strong>決</strong> 定 交 易 是 否 進 行 。如 上 所 述 , <strong>信</strong> 用 交 易 已 成 為 現 代 經 濟 社 會 主 要 的 交 易 方 式 <strong>之</strong> 一 , 就 產 品 或 勞 務 供給 者 ( <strong>授</strong> <strong>信</strong> 者 , 通 常 是 指 <strong>企</strong> <strong>業</strong> 經 營 者 、 生 產 者 或 賣 方 ) 而 言 , 採 取 <strong>信</strong> 用 交 易 方 式 可 為其 帶 來 節 省 大 量 交 易 成 本 的 好 處 2 。 不 過 , <strong>信</strong> 用 交 易 方 式 雖 然 有 此 優 點 , 其 卻 也 同 時 伴隨 著 <strong>信</strong> 用 交 易 風 險 。 <strong>企</strong> <strong>業</strong> 經 營 目 的 在 於 追 求 最 大 淨 利 潤 , 亦 即 追 求 <strong>企</strong> <strong>業</strong> 淨 實 際 營 <strong>業</strong> <strong>收</strong>入 扣 除 總 成 本 後 <strong>之</strong> 最 大 餘 額 。 所 謂 <strong>企</strong> <strong>業</strong> 淨 實 際 營 <strong>業</strong> <strong>收</strong> 入 即 營 <strong>業</strong> 毛 <strong>收</strong> 入 減 去 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>之</strong>壞 <strong>帳</strong> 及 呆 <strong>帳</strong> 損 失 <strong>之</strong> 差 額 。 <strong>企</strong> <strong>業</strong> 營 <strong>業</strong> 毛 <strong>收</strong> 入 提 升 對 於 <strong>企</strong> <strong>業</strong> 淨 利 潤 有 正 面 的 影 響 , 但 是 <strong>應</strong><strong>收</strong> <strong>帳</strong> <strong>款</strong> 產 生 壞 <strong>帳</strong> <strong>與</strong> 呆 <strong>帳</strong> 損 失 則 對 <strong>企</strong> <strong>業</strong> 淨 利 潤 有 負 面 作 用 。 因 此 , <strong>企</strong> <strong>業</strong> 為 達 到 最 大 淨 利2一 般 <strong>企</strong> <strong>業</strong> 營 運 成 本 可 概 略 分 為 生 產 成 本 及 交 易 成 本 兩 大 類 。 所 謂 生 產 成 本 即 為 生 產 該 <strong>企</strong> <strong>業</strong> 所 供 給 產 品或 勞 務 所 產 生 <strong>之</strong> 生 產 要 素 投 入 成 本 , 交 易 成 本 則 為 <strong>企</strong> <strong>業</strong> 為 供 給 其 產 品 或 勞 務 , 包 括 廣 告 、 行 銷 、 執行 交 易 過 程 及 <strong>收</strong> 取 貨 <strong>款</strong> 等 , 所 產 生 <strong>之</strong> 成 本 。 換 言 <strong>之</strong> , 就 <strong>企</strong> <strong>業</strong> 而 言 , 一 切 不 直 接 發 生 於 產 品 或 勞 物 生產 過 程 中 所 產 生 的 成 本 , 均 可 稱 <strong>之</strong> 為 交 易 成 本 。 寇 斯 (Coase,1937) 出 版 「 廠 商 的 本 質 」(TheNature of the Firm) 一 書 <strong>之</strong> 後 , 許 多 經 濟 學 家 不 斷 地 投 入 <strong>研</strong> <strong>究</strong> 交 易 過 程 的 各 種 現 象 。 直 到 1975 年Williamson 綜 合 Coase 的 理 論 和 其 他 有 <strong>關</strong> 交 易 成 本 的 文 獻 , 提 出 一 套 較 完 整 的 交 易 成 本 理 論 。 一 般而 言 , 交 易 成 本 可 以 視 為 一 系 列 的 「 制 度 成 本 」 , 包 括 (1) 搜 尋 <strong>與</strong> 資 訊 成 本 (Search andInformation Costs),(2) 談 判 <strong>與</strong> <strong>決</strong> <strong>策</strong> 成 本 (Bargaining and Decision Costs),(3) <strong>策</strong> 略 <strong>與</strong> 執 行 成 本(Policing and Enforcement Costs),(4) 制 度 結 構 變 化 的 成 本 (Systematic Changing Costs) 等 。由 於 本 文 重 點 並 非 討 論 交 易 成 本 的 內 容 , 因 此 有 <strong>關</strong> 此 議 題 將 不 再 深 入 <strong>研</strong> <strong>究</strong> 。現 代 經 濟 交 易 由 於 交 通 、 電 訊 等 傳 播 工 具 發 達 , 大 幅 縮 短 空 間 距 離 , 因 此 訂 貨 交 易 通 常 經 由 買 方 使用 現 代 通 訊 工 具 , 如 電 話 、 傳 真 或 電 腦 網 路 連 線 進 行 <strong>之</strong> 。 賣 方 在 <strong>收</strong> 到 訂 購 單 後 , 經 由 一 定 的 作 <strong>業</strong> 程序 ( 包 括 徵 <strong>信</strong> ), 開 立 付 <strong>款</strong> 請 求 單 ( <strong>帳</strong> 單 ) 後 連 同 貨 品 送 達 訂 購 者 , 完 成 交 貨 手 續 。 由 於 銷 售 部 門 只需 發 貨 並 開 立 <strong>帳</strong> 單 , 即 可 完 成 交 貨 手 續 , 縮 短 交 貨 時 間 , 貨 品 亦 可 迅 速 運 抵 訂 購 者 。 購 買 者 則 於 <strong>收</strong>到 貨 品 後 再 透 過 銀 行 匯 <strong>款</strong> , 繳 納 貨 <strong>款</strong> , 銷 售 者 不 必 派 遣 人 員 <strong>收</strong> 取 貨 <strong>款</strong> , 因 此 可 大 量 節 省 雙 方 交 易 成本 。2

<strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> <strong>關</strong> <strong>係</strong> <strong>之</strong> <strong>研</strong> <strong>究</strong>pp. 01-20潤 的 目 標 , 除 <strong>應</strong> 努 力 增 加 營 <strong>業</strong> 毛 <strong>收</strong> 入 外 , 亦 需 盡 量 減 少 壞 <strong>帳</strong> 及 呆 <strong>帳</strong> 損 失 。 壞 <strong>帳</strong> 及 呆 <strong>帳</strong>損 失 可 概 略 稱 <strong>之</strong> 為 交 易 風 險 , 此 種 風 險 僅 發 生 於 <strong>信</strong> 用 交 易 方 式 。 反 觀 現 金 交 易 方 式 ,雖 然 不 具 交 易 風 險 但 卻 帶 來 較 高 的 交 易 成 本 3 。 因 此 , 不 管 採 取 何 種 交 易 方 式 , 對 <strong>企</strong><strong>業</strong> 經 營 者 而 言 , 事 實 上 均 存 在 著 魚 <strong>與</strong> 熊 掌 不 能 兼 得 的 兩 難 問 題 。 如 何 選 擇 最 適 交 易 方式 乃 成 為 <strong>企</strong> <strong>業</strong> 為 達 成 其 營 運 目 標 的 重 要 <strong>決</strong> <strong>策</strong> <strong>之</strong> 一 。 鄭 鴻 章 (2008) 建 立 一 經 濟 理 論 分析 模 型 , 同 時 考 慮 交 易 風 險 <strong>與</strong> 交 易 成 本 兩 項 因 素 , 以 數 理 分 析 方 法 探 討 <strong>企</strong> <strong>業</strong> 最 適 交 易方 式 <strong>之</strong> 選 擇 。 <strong>研</strong> <strong>究</strong> 發 現 工 資 愈 高 , <strong>信</strong> 用 交 易 風 險 愈 小 , 愈 有 利 於 使 用 <strong>信</strong> 用 交 易 方 式 ;反 <strong>之</strong> , 工 資 愈 低 , <strong>信</strong> 用 風 險 愈 高 , 愈 有 利 於 現 金 交 易 方 式 。 如 果 現 金 交 易 率 降 低 , 而邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 額 有 急 速 下 降 現 象 , 則 以 採 取 現 金 交 易 及 <strong>信</strong> 用 交 易 <strong>之</strong> 混 和 搭 配 方 式 最為 適 當 。如 上 所 述 , 現 代 <strong>企</strong> <strong>業</strong> 經 營 可 以 採 取 現 金 交 易 方 式 或 <strong>信</strong> 用 交 易 方 式 , 而 一 旦 <strong>企</strong> <strong>業</strong> <strong>決</strong>定 採 取 <strong>信</strong> 用 交 易 方 式 時 , <strong>信</strong> 用 交 易 風 險 <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>之</strong> 選 擇 <strong>決</strong> <strong>策</strong> 卽 具 有 非 常 密 切 的 <strong>關</strong> <strong>係</strong> 。 現代 <strong>企</strong> <strong>業</strong> 經 營 成 敗 和 發 展 <strong>與</strong> 其 營 <strong>業</strong> 額 水 準 具 有 密 切 <strong>關</strong> <strong>係</strong> , 在 採 用 <strong>信</strong> 用 交 易 方 式 時 , <strong>企</strong> <strong>業</strong><strong>決</strong> <strong>策</strong> 者 經 常 遭 遇 到 的 選 擇 問 題 是 : <strong>信</strong> 用 交 易 風 險 <strong>與</strong> 營 <strong>業</strong> 額 <strong>決</strong> <strong>策</strong> <strong>之</strong> 取 捨 。 一 般 而 言 , 若<strong>企</strong> <strong>業</strong> 經 營 者 過 於 保 守 , 希 望 能 完 全 避 免 掉 <strong>信</strong> 用 風 險 , 則 其 營 <strong>業</strong> 額 必 然 會 受 到 不 利 影響 , 甚 至 可 能 影 響 到 <strong>企</strong> <strong>業</strong> 的 生 存 <strong>與</strong> 發 展 。有 鑑 於 <strong>信</strong> 用 交 易 可 能 存 在 交 易 風 險 , 目 前 歐 洲 主 要 徵 <strong>信</strong> 機 構 德 國 「 <strong>信</strong> 用 改 革 聯 合會 」 最 初 即 是 以 倡 導 現 金 交 易 及 拒 絕 <strong>信</strong> 用 交 易 為 其 主 要 宗 旨 而 成 立 , 惟 成 立 不 久 , 該會 即 接 受 無 法 實 現 其 成 立 宗 旨 <strong>之</strong> 事 實 , 因 而 變 更 會 名 , 修 改 宗 旨 4 。 對 現 代 <strong>企</strong> <strong>業</strong> 而言 , 沒 有 <strong>信</strong> 用 交 易 , 便 也 沒 有 交 易 。 因 此 , <strong>企</strong> <strong>業</strong> 不 能 因 噎 廢 食 , 完 全 拒 絕 <strong>信</strong> 用 交 易 。但 是 在 <strong>企</strong> <strong>業</strong> 採 用 <strong>信</strong> 用 交 易 方 式 時 , 當 其 <strong>授</strong> <strong>信</strong> 金 額 愈 高 、 <strong>授</strong> <strong>信</strong> 對 象 愈 廣 , 或 還 債 期 限 愈長 , 則 其 <strong>信</strong> 用 交 易 風 險 也 愈 大 。 因 此 , <strong>企</strong> <strong>業</strong> 在 <strong>授</strong> <strong>與</strong> <strong>信</strong> 用 時 , 必 須 謹 慎 選 擇 <strong>授</strong> <strong>信</strong> 對 象 ,<strong>決</strong> 定 最 高 <strong>授</strong> <strong>信</strong> 金 額 以 及 最 適 <strong>授</strong> <strong>信</strong> 期 限 , 以 期 能 在 營 <strong>業</strong> 額 <strong>與</strong> <strong>信</strong> 用 風 險 <strong>之</strong> 間 , 作 出 最 適 的34由 於 現 金 交 易 方 式 只 認 錢 不 認 人 , 其 交 易 能 否 順 利 進 行 的 先 <strong>決</strong> 條 件 是 買 方 必 須 先 備 有 購 物 所 需 的 現金 , 在 買 賣 成 交 時 , 以 錢 易 貨 。 銷 售 者 於 交 貨 同 時 <strong>收</strong> 進 現 金 , 因 此 , 沒 有 <strong>收</strong> 不 到 貨 <strong>款</strong> 的 風 險 , 交 易風 險 也 就 不 存 在 。 另 外 , 採 用 現 金 交 易 方 式 , 由 於 銷 售 者 必 須 隨 時 派 遣 人 員 <strong>收</strong> 取 貨 <strong>款</strong> , 因 此 其 交 易成 本 較 高 , 此 時 供 給 者 <strong>之</strong> 生 產 <strong>決</strong> <strong>策</strong> 總 成 本 <strong>應</strong> 該 包 括 生 產 成 本 及 交 易 成 本 兩 項 。請 參 閱 陳 重 任 ,1999,「 德 奧 債 <strong>款</strong> 代 <strong>收</strong> <strong>業</strong> 營 運 概 況 」, 台 北 : 財 團 法 人 金 融 聯 合 徵 <strong>信</strong> 中 心 編 印 。3

第 11 期<strong>決</strong> <strong>策</strong> 。所 謂 謹 慎 選 擇 <strong>授</strong> <strong>信</strong> 對 象 , <strong>係</strong> 指 在 <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> 前 , 先 行 判 斷 客 戶 <strong>之</strong> 債 <strong>信</strong> , 從 而 避 免 未來 可 能 遭 受 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 變 成 壞 <strong>帳</strong> 或 呆 <strong>帳</strong> 的 損 失 。 而 欲 作 此 判 斷 , 必 須 事 先 進 行 相 <strong>關</strong> 徵 <strong>信</strong>工 作 或 蒐 集 相 <strong>關</strong> 資 料 , 以 取 得 被 <strong>授</strong> <strong>信</strong> 對 象 必 要 <strong>之</strong> 債 <strong>信</strong> 參 考 資 訊 。所 謂 最 高 <strong>授</strong> <strong>信</strong> 金 額 , <strong>係</strong> 指 <strong>授</strong> 予 每 一 客 戶 <strong>之</strong> 最 高 <strong>信</strong> 用 金 額 而 言 。 現 代 <strong>企</strong> <strong>業</strong> 對 於 往 來客 戶 通 常 給 予 一 定 的 <strong>信</strong> 用 額 度 , 在 不 超 出 此 最 高 <strong>信</strong> 用 金 額 範 圍 , 該 客 戶 可 以 隨 時 訂購 , 並 依 <strong>信</strong> 用 交 易 方 式 , 取 得 所 訂 購 <strong>之</strong> 貨 品 , 同 時 在 約 定 期 限 內 清 償 購 貨 金 額 。 因此 , 若 <strong>授</strong> <strong>信</strong> 金 額 高 , 則 該 客 戶 即 可 訂 購 愈 多 的 貨 品 。 <strong>授</strong> <strong>信</strong> 金 額 對 營 <strong>業</strong> 額 具 有 正 面 的 影響 , 其 影 響 程 度 大 小 則 端 視 客 戶 資 金 是 否 寬 鬆 而 定 , 如 果 客 戶 週 轉 現 金 較 少 , 則 提 高<strong>授</strong> <strong>信</strong> 金 額 , 對 營 <strong>業</strong> 額 <strong>之</strong> 作 用 較 大 。 反 <strong>之</strong> , 如 果 客 戶 週 轉 現 金 充 裕 , 則 提 高 <strong>授</strong> <strong>信</strong> 金 額 對於 該 客 戶 <strong>之</strong> 訂 購 量 影 響 較 小 。 雖 然 <strong>授</strong> <strong>信</strong> 金 額 對 於 營 <strong>業</strong> 額 有 正 面 的 作 用 , 但 另 一 方 面 ,其 對 於 營 <strong>業</strong> 實 <strong>收</strong> 入 率 卻 有 負 面 的 影 響 。 如 果 供 <strong>應</strong> 商 無 限 提 供 客 戶 <strong>授</strong> <strong>信</strong> 金 額 , 則 可 能 造成 若 干 客 戶 , 尤 其 是 經 營 不 善 的 客 戶 , 超 額 進 貨 , 此 舉 將 可 能 對 於 <strong>企</strong> <strong>業</strong> 實 際 營 <strong>收</strong> 造 成不 利 的 影 響 。 一 般 而 言 , <strong>授</strong> <strong>信</strong> 金 額 對 營 <strong>業</strong> 額 及 營 <strong>業</strong> 實 <strong>收</strong> 入 率 <strong>之</strong> 作 用 , 具 有 邊 際 作 用 遞減 的 現 象 。 換 言 <strong>之</strong> , <strong>授</strong> <strong>信</strong> 金 額 提 高 對 營 <strong>業</strong> 額 <strong>之</strong> 正 面 作 用 , <strong>與</strong> 其 對 營 <strong>業</strong> 實 <strong>收</strong> 入 率 <strong>之</strong> 負 面作 用 , 有 逐 漸 遞 減 現 象 。 也 就 是 當 <strong>企</strong> <strong>業</strong> 最 初 引 進 <strong>信</strong> 用 交 易 時 , 對 於 擴 大 營 <strong>業</strong> 額 <strong>之</strong> 刺 激最 大 , 但 繼 續 增 加 <strong>授</strong> <strong>信</strong> 金 額 對 於 營 <strong>業</strong> 額 <strong>之</strong> 作 用 將 逐 漸 減 少 , 因 而 對 於 營 <strong>業</strong> 實 <strong>收</strong> 入 <strong>之</strong> 負面 影 響 也 會 隨 <strong>之</strong> 降 低 。所 謂 償 債 期 限 , <strong>係</strong> 指 自 <strong>授</strong> <strong>信</strong> 時 日 起 , 至 償 還 債 務 <strong>之</strong> 日 期 止 。 清 償 債 務 期 限 可 長 可短 , 若 償 債 期 限 長 , 則 客 戶 償 還 債 <strong>款</strong> 較 有 時 間 彈 性 , 因 此 , 可 能 有 增 加 營 <strong>業</strong> 額 的 作用 , 反 <strong>之</strong> , 如 償 債 期 限 短 , 則 客 戶 在 訂 購 貨 品 時 , 即 需 立 刻 籌 集 資 金 , 否 則 便 無 法 如期 償 還 債 <strong>款</strong> , 此 <strong>與</strong> 現 金 交 易 <strong>之</strong> 差 異 不 大 , 當 然 其 對 於 擴 大 營 <strong>業</strong> 額 的 作 用 亦 很 小 。 因此 , 償 債 期 限 愈 長 愈 較 有 利 於 增 加 營 <strong>業</strong> 額 , 但 償 債 期 限 愈 長 則 有 如 夜 長 夢 多 , 尤 其 對債 <strong>信</strong> 情 況 不 佳 <strong>之</strong> 客 戶 , 無 法 <strong>收</strong> 回 債 <strong>款</strong> 可 能 性 愈 大 。 因 此 , 償 債 期 限 的 長 短 <strong>與</strong> 營 <strong>業</strong> 實 <strong>收</strong>入 比 率 存 在 著 負 相 <strong>關</strong> 。基 於 <strong>授</strong> <strong>信</strong> 對 象 、 <strong>授</strong> <strong>信</strong> 金 額 及 償 債 期 限 對 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 具 重 要 影 響 , 因 此 , <strong>授</strong> <strong>信</strong> 者 為 實現 <strong>企</strong> <strong>業</strong> 經 營 達 到 最 大 淨 實 <strong>收</strong> 利 潤 目 標 , 即 不 容 忽 視 此 三 項 因 素 對 於 營 <strong>業</strong> 利 潤 <strong>之</strong> 影 響 ,4

<strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> <strong>關</strong> <strong>係</strong> <strong>之</strong> <strong>研</strong> <strong>究</strong>pp. 01-20而 必 須 對 其 有 充 分 的 了 解 , 以 便 在 做 <strong>決</strong> <strong>策</strong> 時 有 所 取 捨 。目 前 國 內 在 <strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 的 相 <strong>關</strong> <strong>研</strong> <strong>究</strong> 方 面 , 施 才 憲 (2001) 利 用 <strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>之</strong> 數量 <strong>與</strong> 質 量 間 敏 感 性 的 分 析 提 出 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 的 敏 感 度 值 。 <strong>研</strong> <strong>究</strong> 指 出 影 響 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 數 量 變 動的 敏 感 因 素 , 為 銷 售 變 動 因 素 <strong>與</strong> <strong>信</strong> 用 政 <strong>策</strong> 變 數 中 <strong>之</strong> <strong>收</strong> <strong>款</strong> 期 間 , 其 中 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> 營 <strong>業</strong> <strong>收</strong>入 成 長 率 及 <strong>收</strong> <strong>帳</strong> 期 間 成 長 率 <strong>之</strong> 間 具 有 正 相 <strong>關</strong> 。 池 佳 曄 (2002) 以 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 資 訊 內 涵 <strong>之</strong> 相<strong>關</strong> 解 釋 銷 貨 動 力 說 及 盈 餘 品 質 說 , 檢 視 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>企</strong> <strong>業</strong> 未 來 銷 貨 、 盈 餘 間 <strong>之</strong> <strong>關</strong> 聯 性 ,探 討 我 國 上 市 公 司 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>之</strong> 隱 含 資 訊 內 涵 , 以 期 分 析 我 國 上 市 公 司 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 所 適 用<strong>之</strong> 經 濟 模 型 。 實 證 結 果 顯 示 , 對 於 銷 貨 及 盈 餘 而 言 , <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 的 確 具 有 存 貨 資 訊 以 外的 增 額 資 訊 內 涵 , 同 時 , 不 論 是 否 考 慮 存 貨 資 訊 <strong>之</strong> 影 響 , <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 增 加 , 反 映 出 對 <strong>企</strong><strong>業</strong> 未 來 銷 貨 負 面 的 訊 息 , 亦 即 未 來 銷 貨 、 盈 餘 及 毛 利 率 皆 有 向 下 調 整 <strong>之</strong> 趨 勢 , 也 就 是說 我 國 上 市 公 司 所 適 用 <strong>之</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 經 濟 模 型 較 符 合 「 盈 餘 品 質 說 」 <strong>之</strong> 推 論 。 葉 榮 忠(2002) 以 理 論 及 實 務 並 重 為 基 礎 , 先 建 構 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 的 風 險 管 理 理 論 , 再 以 個 案 <strong>研</strong> <strong>究</strong> 的方 法 來 探 討 此 風 險 管 理 <strong>之</strong> 理 論 如 何 運 用 於 中 小 <strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 管 理 上 , 以 及 風 險 管 理 顧問 在 整 個 協 助 推 動 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 風 險 管 理 的 過 程 中 所 面 臨 的 問 題 。 <strong>研</strong> <strong>究</strong> 結 果 發 現 風 險 管 理<strong>之</strong> 理 論 確 實 可 以 運 用 於 中 小 <strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 管 理 上 , 惟 必 須 同 時 考 慮 到 中 小 <strong>企</strong> <strong>業</strong> 經 營 管理 的 特 性 、 個 別 公 司 管 理 型 態 及 管 理 者 的 差 異 。 郭 一 聰 (2005) <strong>應</strong> 用 <strong>決</strong> <strong>策</strong> 樹 <strong>與</strong> 類 神 經 網路 於 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>之</strong> 呆 <strong>帳</strong> 預 警 模 式 , 此 一 <strong>研</strong> <strong>究</strong> <strong>應</strong> 用 <strong>決</strong> <strong>策</strong> 樹 <strong>與</strong> 類 神 經 網 路 <strong>之</strong> 探 勘 技 術 , 根 據客 戶 基 本 資 料 <strong>與</strong> 交 易 活 動 後 <strong>之</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 資 料 , 組 成 分 析 變 數 , 建 立 逾 期 預 警 模 式 , 提供 <strong>企</strong> <strong>業</strong> 於 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 逾 期 <strong>之</strong> 分 析 , <strong>與</strong> <strong>信</strong> 用 額 度 的 檢 討 <strong>與</strong> 設 定 , 以 降 低 <strong>企</strong> <strong>業</strong> 呆 <strong>帳</strong> 的 機 率 。愛 因 斯 坦 曾 指 出 「 宇 宙 各 種 力 量 終 將 結 合 在 一 起 」。 <strong>企</strong> <strong>業</strong> 的 <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> 亦 然 , 它 包含 各 種 不 同 的 風 險 因 素 。 因 此 , 如 欲 做 出 良 好 的 <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> , 必 須 將 各 個 風 險 因 素 加 以結 合 , 而 非 僅 將 各 項 因 素 加 以 彙 總 而 已 。 本 文 <strong>研</strong> <strong>究</strong> 目 的 在 於 試 圖 建 立 一 經 濟 理 論 分 析模 型 , 從 <strong>企</strong> <strong>業</strong> <strong>授</strong> <strong>信</strong> 管 理 的 角 度 , 結 合 <strong>授</strong> <strong>信</strong> 對 象 、 <strong>授</strong> <strong>信</strong> 金 額 及 償 債 期 限 等 三 項 因 素 , 分析 <strong>企</strong> <strong>業</strong> 在 追 求 最 大 淨 利 潤 目 標 下 , 採 取 <strong>信</strong> 用 交 易 方 式 <strong>之</strong> 最 適 <strong>授</strong> <strong>信</strong> 金 額 及 最 適 償 債 期 限條 件 <strong>與</strong> 最 佳 <strong>授</strong> <strong>信</strong> 對 象 選 擇 <strong>之</strong> 資 訊 需 求 <strong>決</strong> <strong>策</strong> 。 模 型 將 以 <strong>企</strong> <strong>業</strong> 營 運 目 標 在 於 追 求 最 大 淨 實<strong>收</strong> 利 潤 以 及 產 <strong>業</strong> 結 構 為 完 全 競 爭 市 場 等 多 項 前 提 假 設 為 基 礎 建 立 。本 文 章 節 架 構 如 下 : 第 一 節 為 緒 論 , 闡 述 <strong>研</strong> <strong>究</strong> 動 機 <strong>與</strong> <strong>研</strong> <strong>究</strong> 目 的 , 以 及 針 對 <strong>研</strong> <strong>究</strong> 主5

第 11 期題 說 明 相 <strong>關</strong> 概 念 。 第 二 節 將 建 立 一 理 論 模 型 , 首 先 說 明 模 型 假 設 <strong>與</strong> 本 文 分 析 所 用 <strong>之</strong> 相<strong>關</strong> 函 數 定 義 , 然 後 根 據 定 義 探 討 <strong>企</strong> <strong>業</strong> 最 適 交 易 方 式 <strong>之</strong> 選 擇 <strong>決</strong> <strong>策</strong> , 進 而 分 析 採 用 <strong>信</strong> 用 交易 方 式 下 <strong>之</strong> 最 適 <strong>授</strong> <strong>信</strong> 金 額 、 最 適 償 債 期 限 <strong>與</strong> 最 適 資 訊 需 求 量 等 <strong>之</strong> 滿 足 條 件 。 第 三 節 為結 論 , 說 明 <strong>企</strong> <strong>業</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> 者 如 何 <strong>應</strong> 用 本 文 <strong>之</strong> 分 析 結 果 。貳 、 模 型一 、 模 型 假 設 <strong>與</strong> 函 數 定 義本 模 型 <strong>係</strong> 根 據 下 列 三 項 前 提 假 設 而 建 立 :假 設 1: <strong>企</strong> <strong>業</strong> 營 運 可 採 取 <strong>信</strong> 用 交 易 方 式 或 現 金 交 易 方 式 , 本 文 假 設 現 金 交 易 方 式沒 有 交 易 風 險 5 , 因 此 其 實 <strong>收</strong> 營 <strong>業</strong> 額 <strong>與</strong> 毛 營 <strong>業</strong> 額 一 致 。 同 時 我 們 假 設 <strong>信</strong>用 交 易 <strong>之</strong> 交 易 成 本 為 零 6 , 因 此 在 本 文 分 析 <strong>企</strong> <strong>業</strong> 供 給 財 貨 採 <strong>信</strong> 用 交 易 方式 時 將 只 考 慮 生 產 成 本 。假 設 2: <strong>企</strong> <strong>業</strong> 經 營 目 標 在 於 追 求 最 大 淨 實 <strong>收</strong> 利 潤 , 淨 實 <strong>收</strong> 利 潤 <strong>係</strong> 指 毛 利 潤 減 去 壞<strong>帳</strong> 、 呆 <strong>帳</strong> 損 失 <strong>之</strong> 餘 額 。假 設 3: 經 濟 交 易 市 場 為 完 全 競 爭 市 場 , 無 論 供 <strong>應</strong> 者 或 需 求 者 皆 無 單 獨 影 響 市 場的 力 量 。為 分 析 <strong>企</strong> <strong>業</strong> 所 採 用 <strong>之</strong> 交 易 方 式 對 於 <strong>企</strong> <strong>業</strong> 實 <strong>收</strong> 利 潤 淨 額 <strong>之</strong> 影 響 , 我 們 將 使 用 下 列 基本 定 義 <strong>與</strong> 函 數 :56其 理 由 已 於 註 1 中 說 明 , 雖 然 現 金 交 易 亦 略 具 交 易 風 險 , 唯 其 風 險 遠 低 於 <strong>信</strong> 用 交 易 非 常 明 顯 , 不 須贅 述 。採 <strong>信</strong> 用 交 易 方 式 時 , 由 於 銷 售 者 並 非 一 手 交 貨 一 手 <strong>收</strong> 錢 , 雖 然 因 此 可 能 遭 遇 壞 <strong>帳</strong> 或 呆 <strong>帳</strong> 損 失 , 導 致營 <strong>業</strong> 實 <strong>收</strong> 入 率 可 能 並 非 百 分 <strong>之</strong> 百 , 惟 其 交 易 成 本 亦 相 對 較 低 。 由 於 本 文 旨 在 比 較 現 金 交 易 <strong>與</strong> <strong>信</strong> 用 交易 <strong>之</strong> 優 劣 。 因 此 , 本 模 型 所 稱 <strong>之</strong> 交 易 成 本 函 數 , 實 <strong>係</strong> 指 此 兩 種 交 易 方 式 <strong>之</strong> 交 易 成 本 差 額 。 為 便 於 分析 起 見 , 模 型 中 假 設 <strong>信</strong> 用 交 易 <strong>之</strong> 交 易 成 本 為 零 。 雖 然 此 一 假 設 並 不 完 全 <strong>與</strong> 事 實 一 致 , 惟 <strong>信</strong> 用 交 易 <strong>之</strong>交 易 成 本 遠 低 於 現 金 交 易 亦 為 不 爭 <strong>之</strong> 事 實 , 做 此 假 設 可 以 反 映 二 者 <strong>之</strong> 間 交 易 成 本 的 差 別 。6

<strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> <strong>關</strong> <strong>係</strong> <strong>之</strong> <strong>研</strong> <strong>究</strong>pp. 01-20( 一 ) <strong>企</strong> <strong>業</strong> 實 <strong>收</strong> 營 <strong>業</strong> 額此 即 <strong>企</strong> <strong>業</strong> 營 <strong>業</strong> 毛 額 減 去 壞 <strong>帳</strong> 、 呆 <strong>帳</strong> 損 失 <strong>之</strong> 餘 額 。 在 完 全 競 爭 市 場 <strong>之</strong> 前 提 下 ,<strong>企</strong> <strong>業</strong> 營 <strong>業</strong> 毛 額 為 價 格 <strong>與</strong> 銷 售 量 <strong>之</strong> 乘 積 , 即 PQ , 其 中 P 為 產 品 市 價 ,Q 為 銷售 量 。 由 於 <strong>企</strong> <strong>業</strong> 實 <strong>收</strong> 營 <strong>業</strong> 額 為 營 <strong>業</strong> 毛 額 扣 除 壞 <strong>帳</strong> 、 呆 <strong>帳</strong> 損 失 <strong>之</strong> 餘 額 。 若 我 們定 義 <strong>企</strong> <strong>業</strong> 實 <strong>收</strong> 營 <strong>業</strong> 額 <strong>與</strong> 毛 營 <strong>業</strong> 額 兩 者 <strong>之</strong> 比 率 為 α ( 即 α = 實 <strong>收</strong> 營 <strong>業</strong> 額 / 毛 營 <strong>業</strong>額 ), 則 壞 <strong>帳</strong> 、 呆 <strong>帳</strong> 損 失 佔 毛 營 <strong>業</strong> 額 <strong>之</strong> 比 率 即 為 1–α 。 依 此 , <strong>企</strong> <strong>業</strong> 實 <strong>收</strong> 營 <strong>業</strong>額 為 α PQ 。在 完 全 競 爭 市 場 裡 , 單 一 供 給 者 無 法 影 響 市 場 價 格 , 且 為 市 場 價 格 <strong>之</strong> 接 受者 。 因 此 , 產 品 價 格 P 在 該 <strong>企</strong> <strong>業</strong> <strong>決</strong> <strong>策</strong> 時 , <strong>應</strong> 視 為 外 生 變 數 ( exogenousvariable )。 另 一 方 面 , 由 於 <strong>信</strong> 用 交 易 具 交 易 風 險 , 可 能 無 法 全 部 <strong>收</strong> 回 貨 <strong>款</strong> ,因 此 , <strong>企</strong> <strong>業</strong> 實 <strong>收</strong> 營 <strong>業</strong> 額 佔 毛 營 <strong>業</strong> 額 比 率 介 於 零 <strong>與</strong> 一 <strong>之</strong> 間 , 即 0≦α ≦1。( 二 ) 生 產 成 本 函 數生 產 成 本 函 數 即 <strong>企</strong> <strong>業</strong> 為 生 產 某 一 數 量 物 品 或 勞 務 <strong>之</strong> 最 低 成 本 。 此 一 函 數 可 由在 所 建 立 <strong>之</strong> 生 產 函 數 前 提 下 , 追 求 最 低 生 產 成 本 推 導 而 得 7 :( Q)C = C W, , (1)符 號 說 明 :C : 生 產 成 本 函 數 ,W : 工 資 ( 要 素 價 格 ),Q : 生 產 量 。生 產 成 本 函 數 C ( W , Q)具 有 下 列 二 種 特 性 :1. ∂C ≥ 0 : 生 產 成 本 為 工 資 <strong>之</strong> 正 函 數 , 即 工 資 上 漲 , 生 產 成 本 也 會 上∂W升 ,7請 參 閱 Varian, Hal R., 1992, Microeconomics Analysis, 3rd ed., W. W. Norton.7

第 11 期2.∂ C > 0 及 ∂Q2∂ C2 > 0: 邊 際 生 產 成 本 為 正 且 遞 增 。∂ Q此 一 特 性 適 合 於 分 析 一 般 完 全 競 爭 市 場 <strong>之</strong> 廠 商 生 產 。根 據 上 面 所 建 立 <strong>之</strong> 基 本 函 數 , <strong>企</strong> <strong>業</strong> 使 用 <strong>信</strong> 用 交 易 方 式 <strong>之</strong> 目 標 函 數 , 可 由 下 式表 示 <strong>之</strong> :( Q)π = αPQ − C W ,(2)其 中 α 為 <strong>企</strong> <strong>業</strong> 實 <strong>收</strong> 營 <strong>業</strong> 額 比 率 ,1≧α ≧0,π 為 ( 以 <strong>信</strong> 用 交 易 方 式 <strong>之</strong> ) <strong>企</strong> <strong>業</strong>淨 實 <strong>收</strong> 利 潤 。 由 於 <strong>信</strong> 用 交 易 存 在 發 生 壞 <strong>帳</strong> 、 呆 <strong>帳</strong> 損 失 <strong>之</strong> 可 能 性 。 因 此 , 實 <strong>收</strong>營 <strong>業</strong> 額 比 率 通 常 低 於 現 金 交 易 。 唯 <strong>信</strong> 用 交 易 <strong>之</strong> 交 易 成 本 低 ( 本 文 假 設 其 相 當於 零 )。 因 此 , <strong>企</strong> <strong>業</strong> 淨 實 <strong>收</strong> 利 潤 為 實 <strong>收</strong> 營 <strong>業</strong> 額 減 去 生 產 成 本 <strong>之</strong> 餘 額 。 為 推 導出 <strong>企</strong> <strong>業</strong> 最 適 <strong>授</strong> <strong>信</strong> 金 額 <strong>與</strong> 償 債 期 限 , 我 們 必 須 進 一 步 作 下 列 假 設 :假 設 4: 營 <strong>業</strong> 實 <strong>收</strong> 入 率 α 受 到 <strong>授</strong> <strong>信</strong> 金 額 及 償 債 期 限 <strong>之</strong> 影 響 。 當 <strong>授</strong> <strong>信</strong> 金 額 愈 高 , 償債 期 限 愈 長 , 則 營 <strong>業</strong> 實 <strong>收</strong> 入 率 愈 低 ; 反 <strong>之</strong> , 愈 高 。 三 者 <strong>之</strong> 間 具 有 下 列 函數 <strong>關</strong> <strong>係</strong> :∂α∂αα = α( β , l) , < 0 及 < 0 , (3)∂β∂l2∂ α2∂ β

<strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> <strong>關</strong> <strong>係</strong> <strong>之</strong> <strong>研</strong> <strong>究</strong>pp. 01-20∂Q∂Q> 0 及 > 0,∂β∂l22∂ Q ∂ Q< 0 及 < 022∂β∂lo(4)二 、 <strong>企</strong> <strong>業</strong> 最 適 交 易 方 式 <strong>之</strong> 選 擇 <strong>決</strong> <strong>策</strong>根 據 <strong>企</strong> <strong>業</strong> 經 營 追 求 最 大 淨 實 <strong>收</strong> 利 潤 的 原 則 , 交 易 方 式 <strong>之</strong> 選 擇 <strong>決</strong> <strong>策</strong> 可 由 下 列 數 學 求極 大 值 問 題 表 示 :Maxβ ,lπ = αPQ− C( W , Q), (5)Aα = α ( β,l), (6)Q = Q ( β,l), (7)C =C [ Q( β , l ), W ], (8)β ≧0, l ≧0。 (9)(5) 式 為 利 潤 目 標 函 數 ,(6)、(7) 及 (8) 式 則 分 別 顯 示 α , Q , C <strong>與</strong> β , l <strong>之</strong> 間 的 <strong>關</strong><strong>係</strong> 。 為 求 得 利 潤 極 大 值 , 我 們 將 (6)、(7) 及 (8) 式 代 入 (5) 式 中 可 得 :B, l( ) ( ) ( )π = α β PQ β C ⎡ Q β W ⎤A⎣ ⎦Max , l , l - , l , , (10)s.t β ≥ 0,l ≥ 0 。在 (10) 式 求 極 大 值 問 題 中 , <strong>企</strong> <strong>業</strong> <strong>授</strong> <strong>信</strong> <strong>之</strong> <strong>決</strong> <strong>策</strong> 變 數 ( control variables ) 有 <strong>授</strong> <strong>信</strong> 金 額β 及 償 債 期 限 l 等 二 項 。 上 列 求 極 大 值 問 題 <strong>之</strong> 解 答 , 可 <strong>應</strong> 用 非 線 性 規 劃 ( non-linearprogramming ) 方 法 , 求 出 下 列 Kuhn-Tucker 最 適 化 條 件8:8請 參 閱 Sydsaeter, K., 1981. Topics in Mathematical Analysis for Economists, AcademicPress Inc.9

第 11 期⎛ ∂α∂Q∂Q⎞⎜ PQ + Pα -C′⎟β= 0,⎝ ∂β∂β∂β⎠⎛ ∂α∂Q∂Q⎞⎜ PQ + Pα -C′⎟l= 0,⎝ ∂l∂l∂l⎠β ≥ 0, l ≥ 0,[ αPQ-C( Q,W )] ≥ 0 o(11)由 於 目 標 函 數 屬 於 凹 型 ( concave ) 函 數 , 因 此 , 上 列 條 件 屬 於 充 分 條 件 。 依 據 上述 條 件 , <strong>企</strong> <strong>業</strong> 淨 利 潤 極 大 值 <strong>之</strong> 解 , 存 在 下 列 四 種 可 能 組 合 :(1) β =0 及 l = 0 ,(2) β =0 及 l > 0 , (12)(3) β >0 及 l = 0 ,(4) β >0 及 l > 0 。上 述 第 (4) 種 組 合 即 屬 於 典 型 的 <strong>信</strong> 用 交 易 方 式 , β > 0 及 l > 0 。 在 β ≠ 0且l ≠ 0 的情 況 下 , 採 用 <strong>信</strong> 用 交 易 方 式 <strong>之</strong> 最 佳 <strong>授</strong> <strong>信</strong> 金 額 <strong>與</strong> 最 適 償 債 期 限 組 合 <strong>應</strong> 滿 足 下 列 兩 項 條件 :⎧ ∂α∂Q∂Q⎪其 一 : PQ + Pα- C′= 0,∂β∂β∂β⎨⎪ ∂α∂Q∂Q其 二 : PQ + Pα- C′= 0 o⎪⎩∂l∂l∂l(13)三 、 最 適 <strong>授</strong> <strong>信</strong> 金 額 及 最 適 償 債 期 限本 節 進 一 步 分 析 採 用 <strong>信</strong> 用 交 易 方 式 <strong>之</strong> 淨 利 潤 極 大 值 二 條 件 如 下 。 我 們 可 以 將 (13)式 第 一 項 條 件 改 寫 成 下 式 :∂Q∂α− = -PQ(14)∂β∂β( Pα C′)上 式 左 邊 ( Pα C′)− ( ∂Q ∂β) 實 即 邊 際 實 <strong>收</strong> 入 利 潤 , 由 於 Pα ( ∂Q ∂β) 相 當 於 變 動 <strong>授</strong><strong>信</strong> 金 額 因 而 影 響 銷 售 量 所 致 <strong>之</strong> 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 , 而 ( ∂Q ∂β) C′ 則 為 變 動 <strong>授</strong> <strong>信</strong> 金 額 影 響10

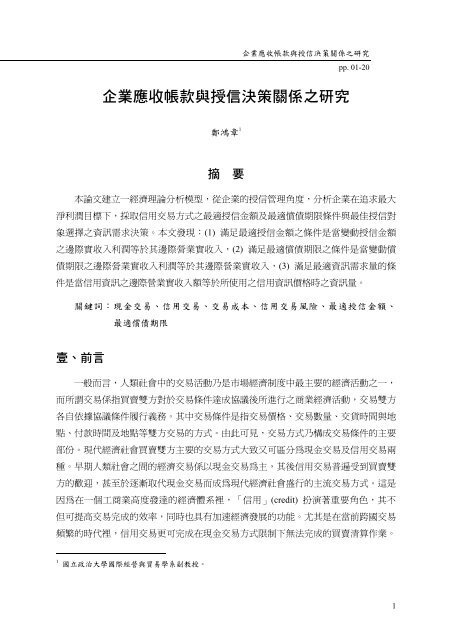

<strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> <strong>關</strong> <strong>係</strong> <strong>之</strong> <strong>研</strong> <strong>究</strong>pp. 01-20銷 售 量 而 導 致 產 出 變 動 所 產 生 <strong>之</strong> 邊 際 成 本 。 上 式 右 邊 <strong>之</strong> PQ ( ∂α ∂β) 表 示 變 動 <strong>授</strong> <strong>信</strong> 金額 影 響 <strong>企</strong> <strong>業</strong> 實 <strong>收</strong> 營 <strong>業</strong> 額 比 率 所 產 生 <strong>之</strong> 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 。 所 以 滿 足 最 適 <strong>授</strong> <strong>信</strong> 金 額 <strong>之</strong> 條 件是 當 <strong>授</strong> <strong>信</strong> 金 額 <strong>之</strong> 邊 際 實 <strong>收</strong> 入 利 潤 等 於 其 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 。 第 二 項 條 件 可 改 寫 為 (15)式 :∂Q∂αPα = -PQ(15)∂l ∂l( − C′)此 條 件 <strong>與</strong> 最 適 <strong>授</strong> <strong>信</strong> 金 額 <strong>之</strong> 條 件 有 類 似 的 解 釋 , 也 就 是 最 適 償 債 期 限 必 須 滿 足 邊 際實 <strong>收</strong> 入 利 潤 等 於 其 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 金 額 。 由 於 無 論 是 提 高 <strong>授</strong> <strong>信</strong> 金 額 或 延 長 償 債 期 限 ,對 於 營 <strong>業</strong> 實 際 <strong>收</strong> 入 率 皆 有 負 面 作 用 , 即 ( ∂α ∂β) < 0 以 及 ( ∂α∂l)< 0 。 因 此 ,− ( ∂α∂β) > 0 以 及 − ( ∂α∂l)> 0 。 由 此 可 見 , 上 述 第 一 及 第 二 條 件 等 式 左 右 兩 邊 皆為 正 數 。 根 據 此 兩 條 件 式 , 以 第 二 條 件 式 左 邊 除 以 第 一 條 件 式 <strong>之</strong> 左 邊 , 同 時 以 第 二 條件 式 右 邊 除 以 第 一 條 件 式 右 邊 , 即 可 求 得 同 時 考 慮 <strong>授</strong> <strong>信</strong> 金 額 <strong>與</strong> <strong>授</strong> <strong>信</strong> 期 限 達 到 最 大 淨 <strong>收</strong>入 利 潤 <strong>應</strong> 滿 足 <strong>之</strong> 條 件 如 下 :∂Q∂β=∂Q∂l∂Q∂β∂α∂β或∂α∂l∂α∂Q=∂β∂l∂α∂lo(16)上 式 表 示 變 動 <strong>授</strong> <strong>信</strong> 金 額 <strong>之</strong> 邊 際 營 <strong>業</strong> 額 <strong>與</strong> 邊 際 營 <strong>業</strong> 實 際 <strong>收</strong> 入 率 <strong>之</strong> 比 例 , 必 需 等 於 改變 償 債 期 限 <strong>之</strong> 邊 際 營 <strong>業</strong> 額 <strong>與</strong> 邊 際 營 <strong>業</strong> 實 際 <strong>收</strong> 入 率 <strong>之</strong> 比 例 。 由 上 面 所 求 得 <strong>之</strong> 實 現 極 大 淨利 潤 最 適 <strong>授</strong> <strong>信</strong> 金 額 及 最 適 償 債 期 限 , 兩 者 <strong>之</strong> 間 具 有 替 代 作 用 , 其 性 質 類 似 於 無 差 異 曲線 ( indifference curve), 可 以 表 示 如 下 圖 1。11

第 11 期α1α 2圖 1: <strong>授</strong> <strong>信</strong> 金 額 <strong>與</strong> 償 債 期 限 <strong>關</strong> <strong>係</strong> 曲 線l為 達 到 某 一 水 準 的 營 <strong>業</strong> 實 <strong>收</strong> 入 比 率 αi , <strong>企</strong> <strong>業</strong> 得 在 選 擇 特 定 的 償 債 期 限 條 件 下 ,<strong>決</strong> 定 其 <strong>授</strong> <strong>信</strong> 金 額 。 若 償 債 期 限 短 , 則 可 增 加 <strong>授</strong> <strong>信</strong> 金 額 , 以 達 到 相 同 的 營 <strong>業</strong> 實 <strong>收</strong> 入 比率 。α = α( β,l)∂α∂α0 = dβ+ d∂β∂l,l o(17)其 中 α 為 某 特 定 營 <strong>業</strong> 實 <strong>收</strong> 入 比 率 。 另 外 , 我 們 可 以 定 義 :MRS β , l∂α= d β= - ∂l,dl∂α∂β(18)即 為 在 某 一 特 定 營 <strong>業</strong> 實 <strong>收</strong> 入 下 <strong>之</strong> <strong>授</strong> <strong>信</strong> 金 額 <strong>與</strong> 償 債 期 限 <strong>之</strong> 邊 際 替 代 率 。 由 於MRS β , l<strong>授</strong> <strong>信</strong> 金 額 <strong>與</strong> <strong>授</strong> <strong>信</strong> 期 限 對 於 營 <strong>業</strong> 實 <strong>收</strong> 入 額 <strong>之</strong> 影 響 具 有 替 代 作 用 。 因 此 , <strong>授</strong> <strong>信</strong> 者 如 <strong>決</strong> 定 達到 一 定 的 營 <strong>業</strong> 實 <strong>收</strong> 入 率 , 可 以 由 <strong>授</strong> <strong>信</strong> 金 額 <strong>之</strong> 高 低 <strong>與</strong> <strong>授</strong> <strong>信</strong> 期 限 <strong>之</strong> 長 短 作 選 擇 。 如 提 高 <strong>授</strong><strong>信</strong> 金 額 則 須 降 低 <strong>授</strong> <strong>信</strong> 期 限 , 以 期 能 達 到 相 同 的 營 <strong>業</strong> 額 <strong>收</strong> 入 率 , 反 <strong>之</strong> , 如 降 低 <strong>授</strong> <strong>信</strong> 金額 , 則 可 以 相 對 延 長 <strong>授</strong> <strong>信</strong> 期 限 。 二 者 <strong>之</strong> 間 的 替 代 作 用 , 視 二 者 <strong>之</strong> 替 代 性 程 度 而 定 。 替代 率 愈 高 , 則 <strong>授</strong> <strong>信</strong> 者 <strong>之</strong> 取 捨 選 擇 可 能 範 圍 亦 較 大 , 如 替 代 率 低 , 則 其 選 擇 取 捨 <strong>之</strong> 可 能範 圍 亦 較 小 。四 、 最 佳 <strong>授</strong> <strong>信</strong> 對 象 選 擇 <strong>之</strong> 資 訊 需 求由 於 被 <strong>授</strong> <strong>信</strong> 者 是 否 誠 實 及 其 債 <strong>信</strong> 優 劣 程 度 <strong>與</strong> <strong>信</strong> 用 交 易 風 險 的 產 生 具 有 密 切 的 <strong>關</strong><strong>係</strong> 。 因 此 , <strong>授</strong> <strong>信</strong> 者 <strong>授</strong> <strong>信</strong> 對 象 <strong>之</strong> 選 擇 , 對 於 營 <strong>業</strong> 實 <strong>收</strong> 入 率 確 實 具 有 正 面 積 極 的 作 用 。 如果 <strong>授</strong> <strong>信</strong> 者 能 在 <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> 前 取 得 有 <strong>關</strong> <strong>授</strong> <strong>信</strong> 對 象 充 分 及 正 確 的 <strong>信</strong> 用 資 訊 , 據 以 正 確 判 斷 被<strong>授</strong> <strong>信</strong> 對 象 <strong>之</strong> 財 務 狀 況 、 債 <strong>信</strong> 等 , 以 避 免 不 當 的 <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> , 必 可 因 而 降 低 <strong>信</strong> 用 交 易 風12

<strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> <strong>關</strong> <strong>係</strong> <strong>之</strong> <strong>研</strong> <strong>究</strong>pp. 01-20險 , 壞 <strong>帳</strong> 、 呆 <strong>帳</strong> 的 交 易 損 失 亦 必 然 會 降 低 , 營 <strong>業</strong> 實 <strong>收</strong> 入 率 也 會 相 對 提 高 。 而 有 <strong>關</strong> <strong>授</strong> <strong>信</strong>對 象 <strong>之</strong> <strong>信</strong> 用 資 訊 來 源 , <strong>授</strong> <strong>信</strong> 者 可 以 親 自 進 行 徵 <strong>信</strong> 工 作 , 或 向 專 營 <strong>信</strong> 用 資 訊 <strong>之</strong> 徵 <strong>信</strong> 機構 , 購 買 該 項 資 訊9。 但 無 論 是 以 何 種 方 式 取 得 <strong>信</strong> 用 資 訊 , <strong>授</strong> <strong>信</strong> 者 為 避 免 <strong>授</strong> <strong>信</strong> 風 險 、選 擇 最 佳 <strong>授</strong> <strong>信</strong> 對 象 , 事 實 上 均 面 臨 資 訊 需 求 的 問 題 , 即 必 須 <strong>決</strong> 定 其 最 適 資 訊 需 求 量 。<strong>授</strong> <strong>信</strong> 者 <strong>之</strong> 最 適 資 訊 需 求 問 題 , 可 由 <strong>授</strong> <strong>信</strong> 者 ( 尤 其 是 銷 貨 <strong>授</strong> <strong>信</strong> 者 ) 依 其 追 求 最 大 淨利 潤 <strong>之</strong> 營 運 目 標 , 利 用 生 產 <strong>決</strong> <strong>策</strong> 模 型 進 行 分 析 。 而 為 推 導 <strong>企</strong> <strong>業</strong> 最 適 資 訊 需 求 <strong>決</strong> <strong>策</strong> , 我們 必 須 進 一 步 作 下 列 假 設 :假 設 6: 由 於 <strong>授</strong> <strong>信</strong> 者 為 選 擇 適 當 的 <strong>授</strong> <strong>信</strong> 對 象 , 必 須 使 用 被 <strong>授</strong> <strong>信</strong> 對 象 的 <strong>信</strong> 用 資 訊 。當 其 所 使 用 資 訊 愈 充 分 , <strong>信</strong> 用 交 易 風 險 愈 低 , 則 營 <strong>業</strong> 實 <strong>收</strong> 入 率 亦 將 愈高 , 即 營 <strong>業</strong> 實 <strong>收</strong> 入 率 <strong>與</strong> <strong>信</strong> 用 資 訊 使 用 量 二 者 <strong>之</strong> 間 具 有 下 列 函 數 <strong>關</strong> <strong>係</strong> :α = α( I )∂ααI= > 0,∂I2∂ ααII= < 0 o2∂I,(19)其 中 I 表 示 <strong>授</strong> <strong>信</strong> 者 <strong>之</strong> <strong>信</strong> 用 資 訊 需 求 量 。 在 上 述 營 <strong>業</strong> 實 <strong>收</strong> 入 率 <strong>與</strong> <strong>信</strong> 用 資 訊 需 求 量 <strong>之</strong>函 數 <strong>關</strong> <strong>係</strong> 中 ,α I >0 表 示 當 <strong>信</strong> 用 資 訊 使 用 量 增 加 , 則 營 <strong>業</strong> 實 <strong>收</strong> 入 率 亦 將 增 加 。 第 二 偏微 分 α < II0 表 示 <strong>信</strong> 用 資 訊 對 營 <strong>業</strong> 實 <strong>收</strong> 入 率 <strong>之</strong> 邊 際 作 用 , 具 有 遞 減 <strong>之</strong> 特 性 。 這 是 因 為 通常 較 容 易 發 現 <strong>之</strong> 不 當 <strong>授</strong> <strong>信</strong> 對 象 , 僅 須 使 用 較 少 較 簡 單 的 資 訊 , 便 足 以 辨 別 <strong>之</strong> , 尤 其 是對 於 那 些 具 有 惡 意 詐 騙 者 。 惟 有 些 <strong>授</strong> <strong>信</strong> 者 <strong>之</strong> <strong>信</strong> 用 介 於 優 劣 <strong>授</strong> <strong>信</strong> 對 象 <strong>之</strong> 邊 緣 , 其 辨 別 識較 不 易 , 使 用 更 多 <strong>信</strong> 用 資 訊 雖 有 助 於 提 高 營 <strong>業</strong> 實 <strong>收</strong> 入 率 , 其 邊 際 效 果 也 會 愈 來 愈 小 。根 據 <strong>企</strong> <strong>業</strong> 追 求 最 大 淨 利 潤 <strong>之</strong> 營 運 目 標 , <strong>信</strong> 用 資 訊 <strong>之</strong> 需 求 , 可 由 求 解 下 列 極 大 值 數 學 問題 導 引 出 來 :9<strong>信</strong> 用 徵 <strong>信</strong> 機 構 是 以 提 供 <strong>信</strong> 用 資 訊 <strong>之</strong> 營 利 事 <strong>業</strong> 。 所 提 供 <strong>之</strong> 資 訊 , 除 有 <strong>關</strong> <strong>授</strong> <strong>信</strong> 對 象 <strong>之</strong> 一 般 資 訊 , 如 地址 、 組 織 型 態 、 所 有 者 、 經 理 人 員 姓 名 、 資 本 額 等 等 , 尤 其 提 供 對 <strong>授</strong> <strong>信</strong> 對 象 債 <strong>信</strong> 評 等 , 提 供 資 訊 使用 者 參 考 。 目 前 在 臺 灣 有 中 華 徵 <strong>信</strong> 所 、 金 融 聯 合 徵 <strong>信</strong> 中 心 等 相 <strong>關</strong> 機 構 。13

第 11 期I( ) ( )π = a I PQ-C Q ηI, (20)BMax -上 式 為 營 運 淨 利 潤 π <strong>之</strong> 定 義 , 其 中 α ( I )PQ 為 營 <strong>業</strong> 實 <strong>收</strong> 入 額 , C ( Q)為 成 本 函B數 ,η 表 示 <strong>信</strong> 用 資 訊 價 格 ,I 為 <strong>信</strong> 用 資 訊 需 求 量 , 其 亦 為 上 式 <strong>之</strong> 求 極 大 值 問 題 中 , <strong>企</strong><strong>業</strong> <strong>授</strong> <strong>信</strong> <strong>之</strong> <strong>決</strong> <strong>策</strong> 變 數 。 由 上 面 極 大 值 問 題 求 出 <strong>之</strong> 最 適 資 訊 需 求 量 I ∗ , 必 須 符 合 下 列 條件 :α I(I)PQ = η , (21)(21) 式 <strong>之</strong> 左 邊 即 使 用 <strong>信</strong> 用 資 訊 <strong>之</strong> 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 額 , 右 邊 便 是 <strong>信</strong> 用 資 訊 價 格 , 也就 是 使 用 <strong>信</strong> 用 資 訊 <strong>之</strong> 邊 際 成 本 。 α 是 使 用 <strong>信</strong> 用 資 訊 對 營 <strong>業</strong> 實 <strong>收</strong> 入 率 <strong>之</strong> 邊 際 作 用 。 由 此I可 見 , 滿 足 最 適 資 訊 需 求 量 的 條 件 是 <strong>信</strong> 用 資 訊 <strong>之</strong> 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 額 等 於 所 使 用 <strong>之</strong> <strong>信</strong> 用資 訊 價 格 。 由 上 式 可 以 進 一 步 解 出 <strong>信</strong> 用 資 訊 需 求 函 數 如 下 :I*⎛ PQ ⎞= I⎜⎟ = α⎝ η ⎠-1I⎛⎜⎝PQη⎞⎟⎠(22)*其 中 I 為 最 適 <strong>信</strong> 用 資 訊 需 求 量 , α -1I為 αI<strong>之</strong> 反 函 數 , I( PQ η) 是 資 訊 需 求 函 數 。由 於 α I (I ) 函 數 具 有 <strong>信</strong> 用 資 訊 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入 率 遞 減 特 性 , 即 ∂ α ( I)∂ I = α < II0I ,10因 此 , <strong>信</strong> 用 資 訊 需 求 函 數 具 有 下 列 特 性 :1. 營 <strong>業</strong> 額 PQ 愈 高 , <strong>信</strong> 用 資 訊 需 求 量 愈 大 , 反 <strong>之</strong> , 愈 小 。<strong>信</strong> 用 資 訊 需 求 <strong>與</strong> 營 <strong>業</strong> 額 <strong>之</strong> 間 的 <strong>關</strong> <strong>係</strong> , 可 由 兩 種 不 同 的 角 度 說 明 : 第 一 , 當 每一 筆 <strong>之</strong> <strong>信</strong> 用 交 易 金 額 愈 高 , 則 對 <strong>信</strong> 用 資 訊 <strong>之</strong> 需 求 量 亦 愈 高 。 換 言 <strong>之</strong> , 如 果 單筆 <strong>信</strong> 用 交 易 額 偏 低 , 即 不 值 得 使 用 <strong>信</strong> 用 資 訊 , 對 於 資 訊 需 求 的 必 要 性 亦 會 相對 降 低 。 第 二 , 當 每 一 交 易 期 間 <strong>之</strong> <strong>信</strong> 用 交 易 總 額 愈 高 , 則 對 <strong>信</strong> 用 資 訊 <strong>之</strong> 需 求量 亦 愈 高 。2. <strong>信</strong> 用 資 訊 價 格 η 愈 高 , <strong>信</strong> 用 資 訊 需 求 量 愈 小 , 反 <strong>之</strong> , 愈 大 。<strong>企</strong> <strong>業</strong> <strong>信</strong> 用 資 訊 <strong>之</strong> 需 求 <strong>與</strong> 其 對 於 生 產 要 素 或 中 間 產 品 <strong>之</strong> 需 求 並 無 差 異 , 均 符 合10得 此 特 性 <strong>之</strong> 數 學 證 明 請 見 附 錄 。14

<strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> <strong>關</strong> <strong>係</strong> <strong>之</strong> <strong>研</strong> <strong>究</strong>pp. 01-20需 求 法 則 。 換 言 <strong>之</strong> , 當 其 價 格 愈 高 , 需 求 量 愈 低 , 反 <strong>之</strong> , 其 價 格 愈 低 , 則 需求 量 愈 高 。綜 言 <strong>之</strong> , <strong>企</strong> <strong>業</strong> <strong>授</strong> <strong>信</strong> 者 <strong>之</strong> <strong>信</strong> 用 資 訊 需 求 , 可 分 別 從 <strong>企</strong> <strong>業</strong> 對 每 一 <strong>授</strong> <strong>信</strong> 對 象 或 從 其 在 一定 期 間 內 <strong>授</strong> <strong>信</strong> 總 額 二 種 不 同 角 度 說 明 :1. 就 <strong>授</strong> <strong>信</strong> 者 對 於 單 一 <strong>授</strong> <strong>信</strong> 對 象 而 言 , 可 依 <strong>授</strong> <strong>信</strong> 者 對 於 <strong>授</strong> <strong>信</strong> 對 象 <strong>之</strong> 認 識 程 度 而 分 :(1) 若 確 知 <strong>授</strong> <strong>信</strong> 對 象 必 能 或 必 不 能 償 還 債 <strong>款</strong> 者 , 不 必 需 求 <strong>信</strong> 用 資 訊 。(2) 若 無 法 確 知 <strong>授</strong> <strong>信</strong> 對 象 <strong>之</strong> 債 <strong>信</strong> 者 , 則 最 適 <strong>信</strong> 用 資 訊 需 求 量 <strong>之</strong> 條 件 ,α I PQ = η , 無 法 滿 足 。 此 時 由 於 資 訊 價 格 η 確 定 , 若 銷 售 金 額 不 高 , 則 可能 存 在 P < ( η α I ) , 其 中 Q i為 對 該 <strong>授</strong> <strong>信</strong> 對 象 <strong>之</strong> 銷 售 量 , 則 此 時 <strong>應</strong> 以 不Q i購 買 使 用 <strong>信</strong> 用 資 訊 較 為 有 利 。 但 如 果 對 該 <strong>授</strong> <strong>信</strong> 對 象 <strong>之</strong> 銷 售 金 額 較 大 而 存 在P Q i≧( η α I ) 的 情 形 , 則 以 購 買 使 用 <strong>信</strong> 用 資 訊 較 為 有 利 。 此 種 考 慮 , 是 <strong>授</strong><strong>信</strong> 者 依 個 別 <strong>授</strong> <strong>信</strong> 對 象 <strong>之</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> 原 則 。2. 就 <strong>授</strong> <strong>信</strong> 者 <strong>之</strong> 總 <strong>授</strong> <strong>信</strong> 額 而 言 , <strong>企</strong> <strong>業</strong> <strong>授</strong> <strong>信</strong> 對 <strong>信</strong> 用 資 訊 <strong>之</strong> 需 求 , <strong>係</strong> 上 述 三 種 情 況 <strong>之</strong> 綜合 。 除 排 除 確 知 <strong>授</strong> <strong>信</strong> 對 象 債 <strong>信</strong> 及 銷 售 額 過 低 <strong>之</strong> 對 象 , 不 需 使 用 <strong>信</strong> 用 資 訊 外 , 其他 所 有 凡 銷 售 額 超 過 一 定 水 準 ( 即 P ≥ η α I ), 而 且 尚 未 確 知 <strong>授</strong> <strong>信</strong> 對 象 <strong>之</strong> 債<strong>信</strong> 者 , 皆 在 需 求 資 訊 <strong>之</strong> 列 , 總 合 對 於 這 些 <strong>授</strong> <strong>信</strong> 對 象 <strong>之</strong> <strong>信</strong> 用 資 訊 需 求 量 , 即 為 <strong>企</strong><strong>業</strong> <strong>授</strong> <strong>信</strong> 者 對 於 <strong>信</strong> 用 資 訊 使 用 <strong>之</strong> 需 求 。由 於 <strong>信</strong> 用 資 訊 <strong>係</strong> 以 每 一 <strong>授</strong> <strong>信</strong> 對 象 為 客 體 <strong>之</strong> 資 訊 , 因 此 , 所 謂 資 訊 需 求 量 實 際 上 是指 需 求 資 訊 <strong>之</strong> 次 數 。 一 般 而 言 , <strong>授</strong> <strong>信</strong> 者 在 一 定 期 間 ( 指 被 <strong>授</strong> <strong>信</strong> 對 象 債 <strong>信</strong> 狀 況 不 會 有 重大 變 動 期 間 ), 會 對 每 一 <strong>授</strong> <strong>信</strong> 客 體 需 求 一 項 <strong>信</strong> 用 資 訊 。 因 此 , <strong>授</strong> <strong>信</strong> 者 在 一 定 期 間 內 ,其 <strong>信</strong> 用 資 訊 需 求 量 , 相 當 於 所 有 符 合 於 下 列 二 條 件 <strong>授</strong> <strong>信</strong> 對 象 數 目 <strong>之</strong> 總 數 :(1) 未 確 知債 <strong>信</strong> <strong>之</strong> 對 象 , 及 (2) 銷 售 額 超 過 一 定 水 準 ( 即 η α I ) <strong>之</strong> 對 象 。 而 所 謂 銷 售 額 是 指 <strong>授</strong> <strong>信</strong> 者在 一 定 期 間 銷 售 給 該 對 象 <strong>之</strong> 總 額 , 而 非 單 一 次 <strong>之</strong> 銷 售 額 。Q i15

第 11 期參 、 結 論歸 納 上 述 理 論 模 型 的 分 析 結 果 , 求 取 最 適 <strong>授</strong> <strong>信</strong> 金 額 及 最 適 償 債 期 限 <strong>之</strong> 解 有 二 :一 、 採 現 金 交 易 <strong>之</strong> 解此 種 情 形 發 生 於 營 <strong>業</strong> 實 <strong>收</strong> 入 率 過 低 , 不 適 合 於 採 用 <strong>信</strong> 用 交 易 方 式 。 就 <strong>企</strong> <strong>業</strong> 銷 售 <strong>決</strong><strong>策</strong> 而 言 , 此 種 解 答 有 兩 種 可 能 的 說 明 :(1) 對 每 一 客 戶 而 言 , <strong>應</strong> 視 該 客 戶 <strong>之</strong> 償 債 能 力( 亦 即 債 <strong>信</strong> ) 而 定 , 如 該 客 戶 為 償 債 能 力 差 或 債 <strong>信</strong> 不 佳 者 , 則 預 期 其 償 還 債 <strong>款</strong> <strong>之</strong> 比 率( 平 均 償 還 債 <strong>款</strong> 率 ) 低 , 則 以 採 取 現 金 交 易 為 上 <strong>策</strong> 。 否 則 , 若 採 用 <strong>信</strong> 用 交 易 即 使 有 提高 營 <strong>業</strong> 額 的 作 用 , 但 卻 可 能 因 償 還 債 <strong>款</strong> 率 過 低 , 而 得 不 償 失 ;(2) 就 <strong>企</strong> <strong>業</strong> 面 對 所 有 客戶 <strong>之</strong> <strong>決</strong> <strong>策</strong> 而 論 , 如 果 營 <strong>業</strong> 實 <strong>收</strong> 入 率 過 低 , 則 使 用 <strong>信</strong> 用 交 易 雖 可 能 增 加 營 <strong>業</strong> 額 , 但 卻 可能 不 僅 無 法 增 加 淨 利 潤 , 而 且 有 負 面 效 果 。 此 時 即 <strong>應</strong> 該 採 用 現 金 交 易 方 式 。二 、 採 <strong>信</strong> 用 交 易 <strong>之</strong> 解採 <strong>信</strong> 用 交 易 方 式 <strong>之</strong> 最 適 <strong>授</strong> <strong>信</strong> 金 額 滿 足 條 件 是 : 當 其 邊 際 實 <strong>收</strong> 入 利 潤 等 於 其 邊 際 營<strong>業</strong> 實 <strong>收</strong> 入 額 。 最 適 償 債 期 限 滿 足 條 件 是 , 當 其 邊 際 實 <strong>收</strong> 入 利 潤 等 於 其 邊 際 營 <strong>業</strong> 實 <strong>收</strong> 入額 。 而 所 謂 邊 際 實 <strong>收</strong> 入 利 潤 <strong>係</strong> 指 因 為 提 高 <strong>授</strong> <strong>信</strong> 金 額 或 延 長 償 債 期 限 導 致 銷 售 量 增 加 因而 增 加 <strong>之</strong> 實 <strong>收</strong> 入 利 潤 ( 即 營 <strong>業</strong> 額 增 加 <strong>與</strong> 成 本 增 加 <strong>之</strong> 差 額 )。 所 謂 邊 際 營 <strong>業</strong> <strong>收</strong> 入 額 , <strong>係</strong>指 提 高 <strong>授</strong> <strong>信</strong> 金 額 , 或 延 長 償 債 期 限 對 營 <strong>業</strong> 實 <strong>收</strong> 入 額 <strong>之</strong> 變 動 作 用 。 除 上 述 件 外 , 最 適 <strong>授</strong><strong>信</strong> 金 額 <strong>與</strong> 最 適 償 債 期 限 兩 者 <strong>之</strong> 間 亦 具 有 下 列 <strong>關</strong> <strong>係</strong> : 最 適 <strong>授</strong> <strong>信</strong> 金 額 <strong>之</strong> 邊 際 營 <strong>業</strong> 額 <strong>與</strong> 邊 際營 <strong>業</strong> 實 際 <strong>收</strong> 入 率 <strong>之</strong> 比 額 , 需 等 於 最 適 償 債 期 限 <strong>之</strong> 邊 際 營 <strong>業</strong> 額 <strong>與</strong> 邊 際 營 <strong>業</strong> 實 際 <strong>收</strong> 入 率 <strong>之</strong>比 率 。<strong>企</strong> <strong>業</strong> 或 <strong>授</strong> <strong>信</strong> 者 欲 <strong>應</strong> 用 上 述 最 適 <strong>授</strong> <strong>信</strong> 金 額 及 最 適 償 債 期 限 <strong>之</strong> 理 論 , 必 須 估 計 兩 者 對其 營 <strong>業</strong> 額 及 對 於 營 <strong>業</strong> 實 際 <strong>收</strong> 入 率 <strong>之</strong> 影 響 。 如 <strong>企</strong> <strong>業</strong> 經 營 者 擁 有 該 <strong>企</strong> <strong>業</strong> 營 運 的 數 據 , 即 可<strong>應</strong> 用 計 量 經 濟 方 法 , 估 計 營 <strong>業</strong> 額 及 營 <strong>業</strong> 實 <strong>收</strong> 入 率 兩 迴 歸 方 程 式 , 依 此 即 可 做 出 利 潤 極大 <strong>之</strong> 最 適 <strong>授</strong> <strong>信</strong> 金 額 <strong>與</strong> 償 債 期 限 <strong>決</strong> <strong>策</strong> 。16

<strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> <strong>關</strong> <strong>係</strong> <strong>之</strong> <strong>研</strong> <strong>究</strong>pp. 01-20附 錄本 附 錄 證 明 <strong>信</strong> 用 資 訊 需 求 函 數 <strong>之</strong> 二 項 主 要 特 性 :1. 營 <strong>業</strong> 額 愈 高 , <strong>信</strong> 用 資 訊 需 求 量 亦 愈 多 , 即 資 訊 需 求 量 <strong>與</strong> 營 <strong>業</strong> 額 <strong>之</strong> 間 具 有 正 向函 數 <strong>關</strong> <strong>係</strong> : ∂I ∂( PQ)> 0 。證 明 :由 最 適 資 訊 需 求 量 條 件 :α PQ = ηI全 微 分 上 式 後 可 得 ,( ) ( )PQ α dI + α d PQ = dη,II( ) = ( )因 此 ,IIIPQ α dI dη - α d PQ ,1dI = dη - αId( PQ ) ,PQα⎡ ⎣⎤ ⎦III由 此 可 見 :∂I -α∂ PQα( PQ)I= >II0,由 於 - α < 0, α < 0, PQ > 0,得 證 oIII2. 資 訊 價 格 愈 高 , 其 需 求 量 愈 低 , 即 資 訊 需 求 受 資 訊 價 格 負 面 <strong>之</strong> 影 響 :( ∂I ∂η)< 0 。證 明 :17

第 11 期1=I,PQα由 dI [ dη−αd(PQ)] 可 得II∂I=∂η1PQαII< 0,由 於 αII 0, Q > 0, 因 此 ( ∂I) < 0,得 証 o∂η參 考 文 獻中 文 部 分 :池 佳 曄 ,2002, <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> 銷 貨 、 盈 餘 <strong>關</strong> 聯 性 <strong>之</strong> 實 證 <strong>研</strong> <strong>究</strong> , 私 立 東 吳 大 學 會 計 <strong>研</strong> <strong>究</strong> 所碩 士 論 文 。施 才 憲 ,2001, <strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 敏 感 性 分 析 <strong>之</strong> <strong>研</strong> <strong>究</strong> , 國 立 中 山 大 學 財 務 管 理 <strong>研</strong> <strong>究</strong> 所 碩士 論 文 。郭 一 聰 ,2005, <strong>應</strong> 用 <strong>決</strong> <strong>策</strong> 樹 <strong>與</strong> 類 神 經 網 路 於 <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>之</strong> 呆 <strong>帳</strong> 預 警 模 式 <strong>研</strong> <strong>究</strong> , 私 立 中 原大 學 資 訊 管 理 <strong>研</strong> <strong>究</strong> 所 碩 士 論 文 。葉 秋 南 ,1996, 美 國 消 費 者 <strong>信</strong> 用 管 理 , 台 北 : 財 團 法 人 金 融 聯 合 徵 <strong>信</strong> 中 心 編 印 。葉 榮 忠 ,2002, 中 小 <strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> 風 險 管 理 <strong>之</strong> <strong>研</strong> <strong>究</strong> , 國 立 高 雄 第 一 科 技 大 學 碩 士 論文 。陳 重 任 ,1999 , 德 奧 債 <strong>款</strong> 代 <strong>收</strong> <strong>業</strong> 營 運 概 況 , 台 北 : 財 團 法 人 金 融 聯 合 徵 <strong>信</strong> 中 心 編印 。陳 肇 榮 ,1985, <strong>信</strong> 用 管 理 <strong>之</strong> 做 法 <strong>與</strong> 評 核 , 現 代 管 理 月 刊 , 六 月 號 。鄭 鴻 章 ,2008 , <strong>企</strong> <strong>業</strong> 最 適 交 易 方 式 選 擇 <strong>之</strong> <strong>研</strong> <strong>究</strong> , 永 豐 金 融 季 刊 , 第 四 十 期 :85-104。英 文 部 分 :Chen, John-ren, 1997. Economics of Credit Information, University of Innsbruck,Unpublished Manuscript.18

<strong>企</strong> <strong>業</strong> <strong>應</strong> <strong>收</strong> <strong>帳</strong> <strong>款</strong> <strong>與</strong> <strong>授</strong> <strong>信</strong> <strong>決</strong> <strong>策</strong> <strong>關</strong> <strong>係</strong> <strong>之</strong> <strong>研</strong> <strong>究</strong>pp. 01-20Coase, R., 1937. The Nature of the Firm. Economics, 4: 386-405.Hair, S., 1992. Sound Credit Risk Assessment, University of Innsbruck, Working Paper.Sydsaeter, K., 1981. Topics in Mathematical Analysis for Economists, Academic Press Inc.Varian, Hal R., 1992. Microeconomic Analysis, 3rd ed., W. W. Norton.Williamson, O.E., 1975. Markets and Hierachies, New York: The Free Press.The Study on the Relationship between CreditTransaction Risk and Decision Making of theEnterprise’s Credit ExtensionHung-Chang Cheng 11AbstractThis paper establishes an economic theoretical analysis model, jointly considering therisk of financing the transaction and the transaction cost factors, first utilizing thequantitative analysis to explore the selection of the enterprise’s optimum transaction method,follow by analyzing the selection strategy of the information required to determine theoptimum credit line, the optimum credit duration and the preferred obligor profile of a profitmaximizing enterprise. This paper discovers: the condition to satisfy the optimum credit lineis determined where the net marginal profit of the variable credit line equals its net marginalrevenue. The condition to satisfy the optimum credit duration is determined where the netmarginal profit of the variable credit duration equals its net marginal revenue. The conditionto satisfy the optimum volume of the information required is determined where the net11 Associate Professor, Department of International Business, National Chengchi University.19

第 11 期marginal revenue of the credit information equals the volume of the information at the priceof the credit information consumed.Key Words: Cash Sale, Credit Sale, Transaction Cost, The Credit Sale Risk, TheOptimum Credit Line, The Optimum Credit Duration.20