KEY ISSUES FOR DIGITAL TRANSFORMATION IN THE G20

2jz0oUm

2jz0oUm

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

These adoption gaps between large firms and SMEs appear to persist over time. Both small and large firms<br />

have increasingly adopted ERP software: On average, 78% of large firms used ERPs in 2015 compared with 64%<br />

in 2010, and 33% of small firms used ERPs in 2015 compared to only 16% in 2010. However, even though ERPs<br />

have diffused to more small and large firms, the disparity across firm sizes in 2015 remains at similar levels to<br />

2010. On average, large firms remain around 50% more likely to have adopted ERPs than small firms in 2015, a<br />

similar adoption gap as in 2010.<br />

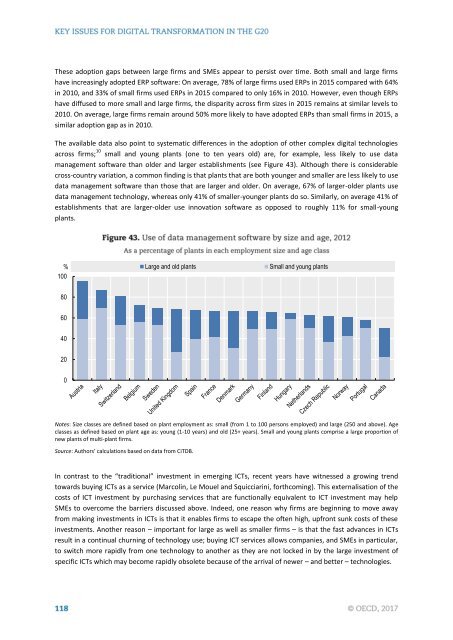

The available data also point to systematic differences in the adoption of other complex digital technologies<br />

across firms; 10 small and young plants (one to ten years old) are, for example, less likely to use data<br />

management software than older and larger establishments (see Figure 43). Although there is considerable<br />

cross-country variation, a common finding is that plants that are both younger and smaller are less likely to use<br />

data management software than those that are larger and older. On average, 67% of larger-older plants use<br />

data management technology, whereas only 41% of smaller-younger plants do so. Similarly, on average 41% of<br />

establishments that are larger-older use innovation software as opposed to roughly 11% for small-young<br />

plants.<br />

% Large and old plants Small and young plants<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

Notes: Size classes are defined based on plant employment as: small (from 1 to 100 persons employed) and large (250 and above). Age<br />

classes as defined based on plant age as: young (1-10 years) and old (25+ years). Small and young plants comprise a large proportion of<br />

new plants of multi-plant firms.<br />

Source: Authors’ calculations based on data from CiTDB.<br />

In contrast to the “traditional” investment in emerging ICTs, recent years have witnessed a growing trend<br />

towards buying ICTs as a service (Marcolin, Le Mouel and Squicciarini, forthcoming). This externalisation of the<br />

costs of ICT investment by purchasing services that are functionally equivalent to ICT investment may help<br />

SMEs to overcome the barriers discussed above. Indeed, one reason why firms are beginning to move away<br />

from making investments in ICTs is that it enables firms to escape the often high, upfront sunk costs of these<br />

investments. Another reason – important for large as well as smaller firms – is that the fast advances in ICTs<br />

result in a continual churning of technology use; buying ICT services allows companies, and SMEs in particular,<br />

to switch more rapidly from one technology to another as they are not locked in by the large investment of<br />

specific ICTs which may become rapidly obsolete because of the arrival of newer – and better – technologies.