Global Compact International Yearbook 2017

Sustainability in Troubled Times We life in times of uncertainty and global (dis)Order. „Understanding global mega-trends is crucial. We live in times of multiple, evolving and mutually-reinforcing shifts“, says UN Secretary-General António Guterres. He adds: „These dynamics, of geopolitical, demographic, climatic, technological, social and economic nature, enhance threats and opportunities on an unprecedented scale.“ Therefore sustainability in troubled times is the key topic of the Global Compact International Yearbook 2017, edited by macondo publishing.

Sustainability in Troubled Times

We life in times of uncertainty and global (dis)Order. „Understanding global mega-trends is crucial. We live in times of multiple, evolving and mutually-reinforcing shifts“, says UN Secretary-General António Guterres. He adds: „These dynamics, of geopolitical, demographic, climatic, technological, social and economic nature, enhance threats and opportunities on an unprecedented scale.“ Therefore

sustainability in troubled times is the key topic of the Global Compact International Yearbook 2017, edited by macondo publishing.

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

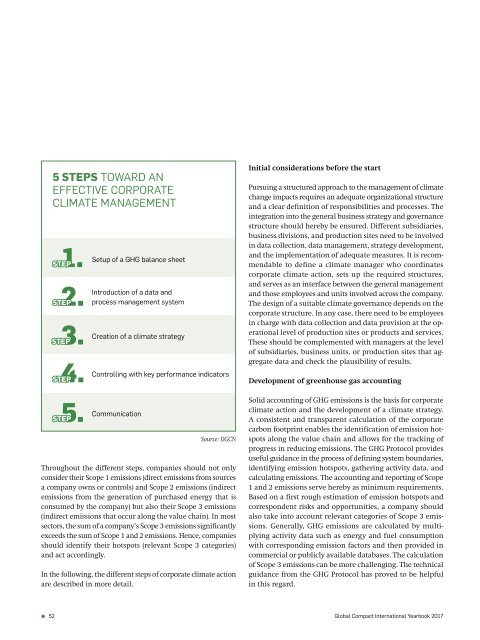

5 STEPS TOWARD AN<br />

EFFECTIVE CORPORATE<br />

CLIMATE MANAGEMENT<br />

STEP 1.<br />

STEP 2.<br />

STEP 3.<br />

STEP 4.<br />

STEP 5.<br />

Setup of a GHG balance sheet<br />

Introduction of a data and<br />

process management system<br />

Creation of a climate strategy<br />

Controlling with key performance indicators<br />

Communication<br />

Source: DGCN<br />

Throughout the different steps, companies should not only<br />

consider their Scope 1 emissions (direct emissions from sources<br />

a company owns or controls) and Scope 2 emissions (indirect<br />

emissions from the generation of purchased energy that is<br />

consumed by the company) but also their Scope 3 emissions<br />

(indirect emissions that occur along the value chain). In most<br />

sectors, the sum of a company’s Scope 3 emissions significantly<br />

exceeds the sum of Scope 1 and 2 emissions. Hence, companies<br />

should identify their hotspots (relevant Scope 3 categories)<br />

and act accordingly.<br />

In the following, the different steps of corporate climate action<br />

are described in more detail.<br />

Initial considerations before the start<br />

Pursuing a structured approach to the management of climate<br />

change impacts requires an adequate organizational structure<br />

and a clear definition of responsibilities and processes. The<br />

integration into the general business strategy and governance<br />

structure should hereby be ensured. Different subsidiaries,<br />

business divisions, and production sites need to be involved<br />

in data collection, data management, strategy development,<br />

and the implementation of adequate measures. It is recommendable<br />

to define a climate manager who coordinates<br />

corporate climate action, sets up the required structures,<br />

and serves as an interface between the general management<br />

and those employees and units involved across the company.<br />

The design of a suitable climate governance depends on the<br />

corporate structure. In any case, there need to be employees<br />

in charge with data collection and data provision at the operational<br />

level of production sites or products and services.<br />

These should be complemented with managers at the level<br />

of subsidiaries, business units, or production sites that aggregate<br />

data and check the plausibility of results.<br />

Development of greenhouse gas accounting<br />

Solid accounting of GHG emissions is the basis for corporate<br />

climate action and the development of a climate strategy.<br />

A consistent and transparent calculation of the corporate<br />

carbon footprint enables the identification of emission hotspots<br />

along the value chain and allows for the tracking of<br />

progress in reducing emissions. The GHG Protocol provides<br />

useful guidance in the process of defining system boundaries,<br />

identifying emission hotspots, gathering activity data, and<br />

calculating emissions. The accounting and reporting of Scope<br />

1 and 2 emissions serve hereby as minimum requirements.<br />

Based on a first rough estimation of emission hotspots and<br />

correspondent risks and opportunities, a company should<br />

also take into account relevant categories of Scope 3 emissions.<br />

Generally, GHG emissions are calculated by multiplying<br />

activity data such as energy and fuel consumption<br />

with corresponding emission factors and then provided in<br />

commercial or publicly available databases. The calculation<br />

of Scope 3 emissions can be more challenging. The technical<br />

guidance from the GHG Protocol has proved to be helpful<br />

in this regard.<br />

52<br />

<strong>Global</strong> <strong>Compact</strong> <strong>International</strong> <strong>Yearbook</strong> <strong>2017</strong>