PINC POWERPICKS - Myiris.com

PINC POWERPICKS - Myiris.com

PINC POWERPICKS - Myiris.com

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>PINC</strong> <strong>POWERPICKS</strong> RESEARCH<br />

RESEARCH<br />

JYOTHY LABORATORIES: BUY, TP-Rs246 (23% upside)<br />

What’s the theme?<br />

Jyothy Laboratories (Jyothy) is in the transformation phase following the acquisition of Henkel India. The<br />

strong operational performance of Henkel India in Q2CY11 gives us confidence of a turnaround. We see<br />

various operational synergies following the acquisition and expect numerous positives for Jyothy Labs in<br />

the medium to long term, which would improve overall profitability. Jyothy is among the few <strong>com</strong>panies in<br />

the FMCG space which has immense potential for long-term profitability growth.<br />

What will move the stock?<br />

1) The acquisition of Henkel India added 4-5 established brands that improved Jyothy's sales mix; 2) Full<br />

impact of the price increase of Ujala Supreme will support revenue and profitability growth; 3) Maxo Military<br />

will add Rs600mn and Rs700mn revenue in FY12 and FY13 respectively; 4) We expect improvement in<br />

profitability in Henkel India; 5) Debt restructuring can lead to higher profitability; 6) Merger of Jyothy and<br />

Henkel India will engender massive tax benefits of Rs1.2bn; 7) Restructuring of Jyothy's distribution model<br />

would improve EBITDA margin by 3%.<br />

Where are we stacked versus consensus?<br />

Our estimates for FY13 are among the highest on the street, led by expectation of profitability improvement<br />

in Henkel India. We assign 16x to FY13 earnings and add Rs12/share NPV on tax saving of Rs1.2bn<br />

@12% discount rate to derive the TP of Rs246.<br />

What will challenge our target price?<br />

1) We are cautious on FY12 performance due to restructuring over next 6-9 months; 2) Any delay in operational<br />

improvement in Henkel India will impact the overall profitability; 3) Higher brand building investments; 4) Change<br />

in our estimates for input costs owing to volatility in crude prices and 5) Inability to attract retail clients in the<br />

laundry business.<br />

7<br />

(Rs mn) FY10 FY11 FY12E YoY % FY13E YoY %<br />

Net Sales 5,975 6,230 11,963 92.0 13,872 16.0<br />

EBITDA 929 775 1,110 43.3 1,778 60.1<br />

EBITDA Marg. (%) 15.5 12.4 9.3 (316)bps 12.8 353bps<br />

Adj. Net Profits 742 717 557 (22.3) 1,180 111.9<br />

Dil. EPS (Rs) 9.2 8.9 6.9 (22.3) 14.6 111.9<br />

PER (x) 21.8 22.6 29.0 - 13.7 -<br />

ROE (%) 19.1 11.2 11.4 23bps 20.8 936bps<br />

ROCE (%) 23.2 11.0 9.7 (137)bps 15.4 571bps<br />

Sector: FMCG<br />

CMP: Rs200; Mcap: Rs16bn<br />

Bloomberg: JYL IN; Reuters: JYOI.BO<br />

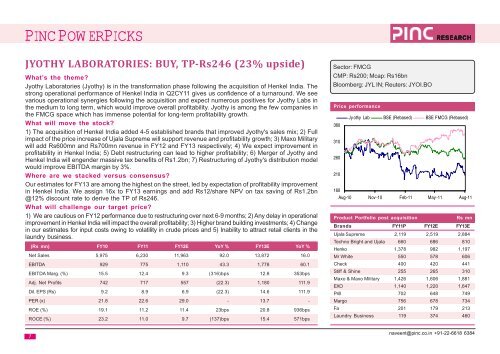

Price performance<br />

360<br />

310<br />

260<br />

210<br />

Jy othy Lab BSE (Rebased) BSE FMCG (Rebased)<br />

160<br />

Aug-10 Nov -10 Feb-11 May -11 Aug-11<br />

Product Portfolio post acquisition Rs mn<br />

Brands FY11P FY12E FY13E<br />

Ujala Supreme 2,119 2,519 2,884<br />

Techno Bright and Ujala 660 686 810<br />

Henko 1,378 982 1,197<br />

Mr White 550 578 606<br />

Check 400 420 441<br />

Stiff & Shine 255 265 310<br />

Maxo & Maxo Military 1,426 1,606 1,881<br />

EXO 1,140 1,220 1,647<br />

Prill 702 648 749<br />

Margo 756 678 734<br />

Fa 201 179 213<br />

Laundry Business 119 374 460<br />

naveent@pinc.co.in +91-22-6618 6384