Equilibrium Growth, Inflation, and Bond Yields - Duke University's ...

Equilibrium Growth, Inflation, and Bond Yields - Duke University's ...

Equilibrium Growth, Inflation, and Bond Yields - Duke University's ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

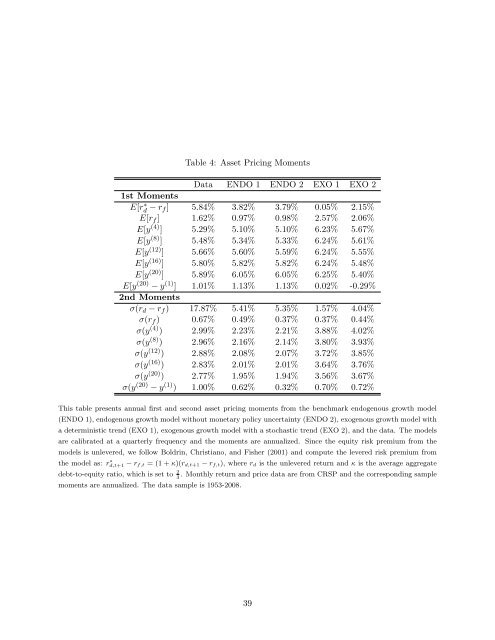

Table 4: Asset Pricing Moments<br />

Data ENDO 1 ENDO 2 EXO 1 EXO 2<br />

1st Moments<br />

E[r ∗ d − rf ] 5.84% 3.82% 3.79% 0.05% 2.15%<br />

E[rf ] 1.62% 0.97% 0.98% 2.57% 2.06%<br />

E[y (4) ] 5.29% 5.10% 5.10% 6.23% 5.67%<br />

E[y (8) ] 5.48% 5.34% 5.33% 6.24% 5.61%<br />

E[y (12) ] 5.66% 5.60% 5.59% 6.24% 5.55%<br />

E[y (16) ] 5.80% 5.82% 5.82% 6.24% 5.48%<br />

E[y (20) ] 5.89% 6.05% 6.05% 6.25% 5.40%<br />

E[y (20) − y (1) ] 1.01% 1.13% 1.13% 0.02% -0.29%<br />

2nd Moments<br />

σ(rd − rf ) 17.87% 5.41% 5.35% 1.57% 4.04%<br />

σ(rf ) 0.67% 0.49% 0.37% 0.37% 0.44%<br />

σ(y (4) ) 2.99% 2.23% 2.21% 3.88% 4.02%<br />

σ(y (8) ) 2.96% 2.16% 2.14% 3.80% 3.93%<br />

σ(y (12) ) 2.88% 2.08% 2.07% 3.72% 3.85%<br />

σ(y (16) ) 2.83% 2.01% 2.01% 3.64% 3.76%<br />

σ(y (20) ) 2.77% 1.95% 1.94% 3.56% 3.67%<br />

σ(y (20) − y (1) ) 1.00% 0.62% 0.32% 0.70% 0.72%<br />

This table presents annual first <strong>and</strong> second asset pricing moments from the benchmark endogenous growth model<br />

(ENDO 1), endogenous growth model without monetary policy uncertainty (ENDO 2), exogenous growth model with<br />

a deterministic trend (EXO 1), exogenous growth model with a stochastic trend (EXO 2), <strong>and</strong> the data. The models<br />

are calibrated at a quarterly frequency <strong>and</strong> the moments are annualized. Since the equity risk premium from the<br />

models is unlevered, we follow Boldrin, Christiano, <strong>and</strong> Fisher (2001) <strong>and</strong> compute the levered risk premium from<br />

the model as: r ∗ d,t+1 − rf,t = (1 + κ)(rd,t+1 − rf,t), where rd is the unlevered return <strong>and</strong> κ is the average aggregate<br />

debt-to-equity ratio, which is set to 2<br />

. Monthly return <strong>and</strong> price data are from CRSP <strong>and</strong> the corresponding sample<br />

3<br />

moments are annualized. The data sample is 1953-2008.<br />

39