Introduction : EDP et finance. - Université du Maine

Introduction : EDP et finance. - Université du Maine

Introduction : EDP et finance. - Université du Maine

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

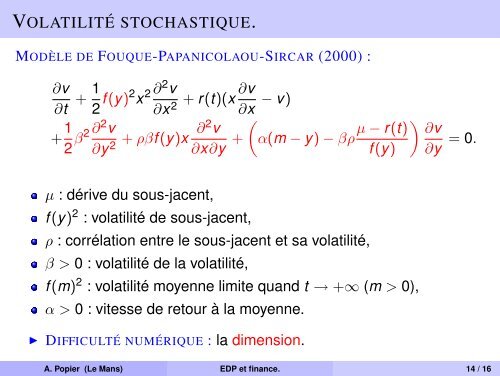

VOLATILITÉ STOCHASTIQUE.<br />

MODÈLE DE FOUQUE-PAPANICOLAOU-SIRCAR (2000) :<br />

∂v<br />

∂t + 1 2 f (y)2 x 2 ∂2 v ∂v<br />

+ r(t)(x<br />

∂x 2 ∂x − v)<br />

+ 1 (<br />

2 β2 ∂2 v<br />

∂y 2 + ρβf (y)x ∂2 v<br />

∂x∂y + α(m − y) − βρ µ − r(t) ) ∂v<br />

f (y) ∂y = 0.<br />

µ : dérive <strong>du</strong> sous-jacent,<br />

f (y) 2 : volatilité de sous-jacent,<br />

ρ : corrélation entre le sous-jacent <strong>et</strong> sa volatilité,<br />

β > 0 : volatilité de la volatilité,<br />

f (m) 2 : volatilité moyenne limite quand t → +∞ (m > 0),<br />

α > 0 : vitesse de r<strong>et</strong>our à la moyenne.<br />

◮ DIFFICULTÉ NUMÉRIQUE : la dimension.<br />

A. Popier (Le Mans) <strong>EDP</strong> <strong>et</strong> <strong>finance</strong>. 14 / 16