Introduction : EDP et finance. - Université du Maine

Introduction : EDP et finance. - Université du Maine

Introduction : EDP et finance. - Université du Maine

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

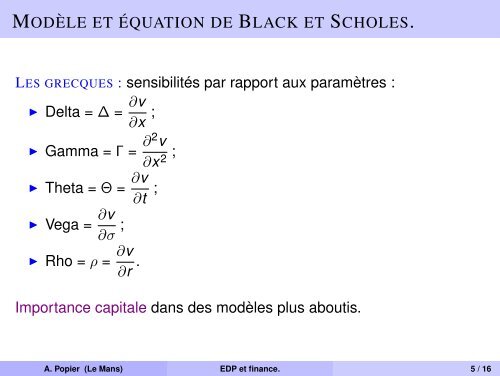

MODÈLE ET ÉQUATION DE BLACK ET SCHOLES.<br />

LES GRECQUES : sensibilités par rapport aux paramètres :<br />

◮ Delta = ∆ = ∂v<br />

∂x ;<br />

◮ Gamma = Γ = ∂2 v<br />

∂x 2 ;<br />

◮ Th<strong>et</strong>a = Θ = ∂v<br />

∂t ;<br />

◮ Vega = ∂v<br />

∂σ ;<br />

◮ Rho = ρ = ∂v<br />

∂r .<br />

Importance capitale dans des modèles plus aboutis.<br />

A. Popier (Le Mans) <strong>EDP</strong> <strong>et</strong> <strong>finance</strong>. 5 / 16