3433-vol. 6 issue 2-3.pmd - iarfc

3433-vol. 6 issue 2-3.pmd - iarfc

3433-vol. 6 issue 2-3.pmd - iarfc

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Volume 6, Issue 2 & 3 115<br />

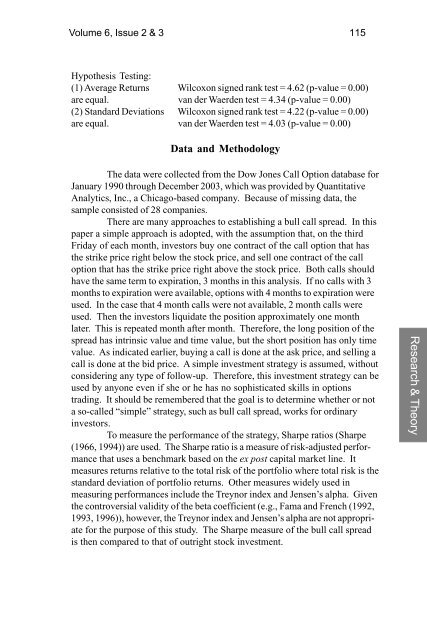

Hypothesis Testing:<br />

(1) Average Returns Wilcoxon signed rank test = 4.62 (p-value = 0.00)<br />

are equal. van der Waerden test = 4.34 (p-value = 0.00)<br />

(2) Standard Deviations Wilcoxon signed rank test = 4.22 (p-value = 0.00)<br />

are equal. van der Waerden test = 4.03 (p-value = 0.00)<br />

Data and Methodology<br />

The data were collected from the Dow Jones Call Option database for<br />

January 1990 through December 2003, which was provided by Quantitative<br />

Analytics, Inc., a Chicago-based company. Because of missing data, the<br />

sample consisted of 28 companies.<br />

There are many approaches to establishing a bull call spread. In this<br />

paper a simple approach is adopted, with the assumption that, on the third<br />

Friday of each month, investors buy one contract of the call option that has<br />

the strike price right below the stock price, and sell one contract of the call<br />

option that has the strike price right above the stock price. Both calls should<br />

have the same term to expiration, 3 months in this analysis. If no calls with 3<br />

months to expiration were available, options with 4 months to expiration were<br />

used. In the case that 4 month calls were not available, 2 month calls were<br />

used. Then the investors liquidate the position approximately one month<br />

later. This is repeated month after month. Therefore, the long position of the<br />

spread has intrinsic value and time value, but the short position has only time<br />

value. As indicated earlier, buying a call is done at the ask price, and selling a<br />

call is done at the bid price. A simple investment strategy is assumed, without<br />

considering any type of follow-up. Therefore, this investment strategy can be<br />

used by anyone even if she or he has no sophisticated skills in options<br />

trading. It should be remembered that the goal is to determine whether or not<br />

a so-called “simple” strategy, such as bull call spread, works for ordinary<br />

investors.<br />

To measure the performance of the strategy, Sharpe ratios (Sharpe<br />

(1966, 1994)) are used. The Sharpe ratio is a measure of risk-adjusted performance<br />

that uses a benchmark based on the ex post capital market line. It<br />

measures returns relative to the total risk of the portfolio where total risk is the<br />

standard deviation of portfolio returns. Other measures widely used in<br />

measuring performances include the Treynor index and Jensen’s alpha. Given<br />

the controversial validity of the beta coefficient (e.g., Fama and French (1992,<br />

1993, 1996)), however, the Treynor index and Jensen’s alpha are not appropriate<br />

for the purpose of this study. The Sharpe measure of the bull call spread<br />

is then compared to that of outright stock investment.<br />

Research & Theory