3433-vol. 6 issue 2-3.pmd - iarfc

3433-vol. 6 issue 2-3.pmd - iarfc

3433-vol. 6 issue 2-3.pmd - iarfc

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

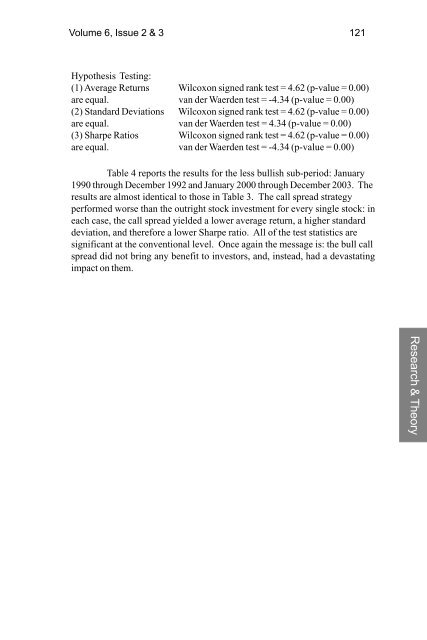

Volume 6, Issue 2 & 3 121<br />

Hypothesis Testing:<br />

(1) Average Returns Wilcoxon signed rank test = 4.62 (p-value = 0.00)<br />

are equal. van der Waerden test = -4.34 (p-value = 0.00)<br />

(2) Standard Deviations Wilcoxon signed rank test = 4.62 (p-value = 0.00)<br />

are equal. van der Waerden test = 4.34 (p-value = 0.00)<br />

(3) Sharpe Ratios Wilcoxon signed rank test = 4.62 (p-value = 0.00)<br />

are equal. van der Waerden test = -4.34 (p-value = 0.00)<br />

Table 4 reports the results for the less bullish sub-period: January<br />

1990 through December 1992 and January 2000 through December 2003. The<br />

results are almost identical to those in Table 3. The call spread strategy<br />

performed worse than the outright stock investment for every single stock: in<br />

each case, the call spread yielded a lower average return, a higher standard<br />

deviation, and therefore a lower Sharpe ratio. All of the test statistics are<br />

significant at the conventional level. Once again the message is: the bull call<br />

spread did not bring any benefit to investors, and, instead, had a devastating<br />

impact on them.<br />

Research & Theory