Albrecht 19.pdf - Marriott School

Albrecht 19.pdf - Marriott School

Albrecht 19.pdf - Marriott School

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

76154_23_ch19_p942-1006.qxd 3/1/07 3:35 PM Page 981<br />

EOC | Controlling Cost, Profit, and Investment Centers Chapter 19 981<br />

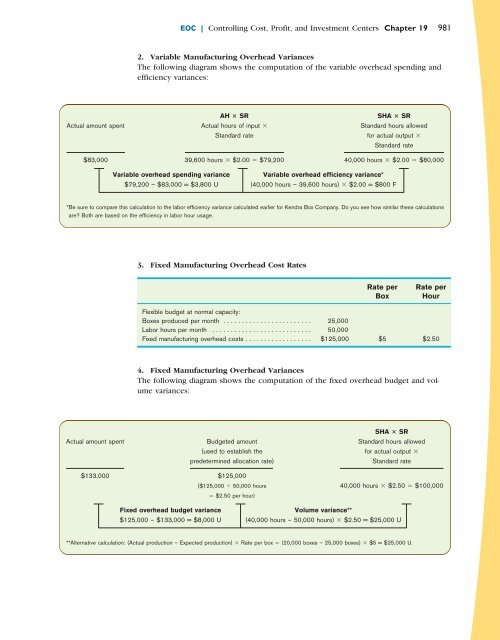

2. Variable Manufacturing Overhead Variances<br />

The following diagram shows the computation of the variable overhead spending and<br />

efficiency variances:<br />

AH SR<br />

SHA SR<br />

Actual amount spent Actual hours of input Standard hours allowed<br />

Standard rate<br />

for actual output <br />

Standard rate<br />

$83,000 39,600 hours $2.00 $79,200 40,000 hours $2.00 $80,000<br />

Variable overhead spending variance<br />

Variable overhead efficiency variance*<br />

$79,200 – $83,000 = $3,800 U (40,000 hours – 39,600 hours) $2.00 = $800 F<br />

*Be sure to compare this calculation to the labor efficiency variance calculated earlier for Kendra Box Company. Do you see how similar these calculations<br />

are Both are based on the efficiency in labor hour usage.<br />

3. Fixed Manufacturing Overhead Cost Rates<br />

Rate per<br />

Box<br />

Rate per<br />

Hour<br />

Flexible budget at normal capacity:<br />

Boxes produced per month . . . . . . . . . . . . . . . . . . . . . . . . 25,000<br />

Labor hours per month . . . . . . . . . . . . . . . . . . . . . . . . . . . 50,000<br />

Fixed manufacturing overhead costs . . . . . . . . . . . . . . . . . . $125,000 $5 $2.50<br />

4. Fixed Manufacturing Overhead Variances<br />

The following diagram shows the computation of the fixed overhead budget and volume<br />

variances:<br />

SHA SR<br />

Actual amount spent Budgeted amount Standard hours allowed<br />

(used to establish the<br />

for actual output <br />

predetermined allocation rate)<br />

Standard rate<br />

$133,000 $125,000<br />

($125,000 50,000 hours 40,000 hours $2.50 $100,000<br />

$2.50 per hour)<br />

Fixed overhead budget variance<br />

Volume variance**<br />

$125,000 – $133,000 = $8,000 U (40,000 hours – 50,000 hours) $2.50 = $25,000 U<br />

**Alternative calculation: (Actual production – Expected production) Rate per box (20,000 boxes – 25,000 boxes) $5 = $25,000 U.