Global Economic Outlook and Strategy - Kadin Indonesia

Global Economic Outlook and Strategy - Kadin Indonesia

Global Economic Outlook and Strategy - Kadin Indonesia

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

February 28, 2008<br />

<strong>Global</strong> <strong>Economic</strong> <strong>Outlook</strong> <strong>and</strong> <strong>Strategy</strong><br />

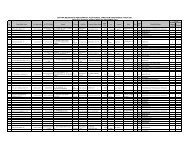

Figure 3. Forecast Highlights <strong>and</strong> Changes from Last Month<br />

G3<br />

• United States • With tight financial conditions reinforcing economic weakness, the<br />

Fed has taken a more aggressive tack, with only limited impact<br />

thus far. We look for cuts in the funds rate to 2% by midyear,<br />

barring a sharp recovery in risk appetite <strong>and</strong> housing leads.<br />

• Euro Area • Growth has slowed to a subtrend pace, where it probably will stay<br />

until late this year. Inflation remains high but should moderate<br />

quickly. We expect the ECB to ease policy modestly later this year.<br />

• Japan • <strong>Economic</strong> growth likely will remain near trend in 2008. The next<br />

BoJ rate hike probably will be delayed until around yearend, as<br />

uncertainties surrounding the global outlook have increased.<br />

Others<br />

• United Kingdom • The MPC will likely cut rates a lot more, but any easing will be<br />

gradual in order to grind down inflation expectations.<br />

• Canada • Moderating inflation <strong>and</strong> lingering downside risks likely will prompt<br />

an additional 100 basis points of BoC easing before summer.<br />

• Australia • The RBA is set to tighten policy again in March <strong>and</strong> May, with the<br />

risk of further tightening beyond that, as the Bank attempts to drive<br />

inflation back down toward the 2%-3% target range.<br />

• China • Rising inflation <strong>and</strong> weakening exports could lead to a period of<br />

tight monetary policy <strong>and</strong> loose fiscal policy.<br />

• Other Emerging Markets • Inflation worries are probably overblown, but they will reduce<br />

the scope for monetary loosening in the short run <strong>and</strong> dampen<br />

growth.<br />

3