National Horticultural Research Network - Horticulture Industry ...

National Horticultural Research Network - Horticulture Industry ...

National Horticultural Research Network - Horticulture Industry ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>National</strong> <strong>Horticultural</strong> <strong>Research</strong> <strong>Network</strong><br />

Vegetable Sector RD&E Framework September 2010<br />

___________________________________________________________________<br />

2.1.5.2 <strong>Industry</strong> Outlook and Drivers - Sweet corn, Asparagus, Beans and Peas<br />

Production is in decline for all these crops, with reduced local processing due to strong competition<br />

from lower cost imported processed products. Despite this, processing production for sweet corn,<br />

beans and peas, and export of asparagus, dominate the figures.<br />

Sweet corn: The outlook as a fresh vegetable is good due to consumer interest in phyto-nutrients and<br />

the potential for export by overcoming pest problems (NIR technology exists for detection of<br />

Heliocoverpa in silks) but would be further improved by more favourable exchange rates (the AUD at<br />

USD 0.70). The outlook as a processed vegetable is poor. Imports of frozen product doubled in 2008<br />

to $27 million. In common with most vegetable industries, profitability and the need for reduced costs<br />

of production are overarching issues for sweet corn to maintain international competitiveness.<br />

Opportunities include variety improvement (more than one cob/plant,) to increase yields and to<br />

improve competitiveness against imports. There are also opportunities for product development with<br />

white and bi-colour corn appropriately marketed.<br />

Asparagus. Emphasis is shifting from export to domestic markets because of the reduced water<br />

availability in northern Victoria. Future expansion will depend upon a return to non-drought<br />

conditions and issues remain with weed, pest and disease control and with post harvest quality.<br />

Potential exists for mechanical harvesting to reduce labour costs. Export market opportunities exist<br />

under favourable Australian dollar exchange rate conditions and domestic consumer demand is<br />

increasing. The asparagus industry has no compulsory national levy arrangements and relies on<br />

voluntary contributions from industry.<br />

Peas and Beans - Processing. Production for Tasmanian processing dominates the national figures.<br />

For processing, the main issue has been competition from low cost overseas imports supported by a<br />

high AUD$.<br />

Peas and Beans - Fresh. ABS commentary notes consolidation has occurred in supply chains in an<br />

attempt to access large customers. These efficiencies have allowed Qld to maintain production at<br />

about the same level for the last 5 years. Bean production in NSW has more than doubled, possibly<br />

due to development of a processing market niche. In all other states production has dropped.<br />

For these crops to compete against imports, productivity needs to increase significantly. As with other<br />

mature vegetable industries peas and beans need product innovation and productivity increases to be<br />

world competitive.<br />

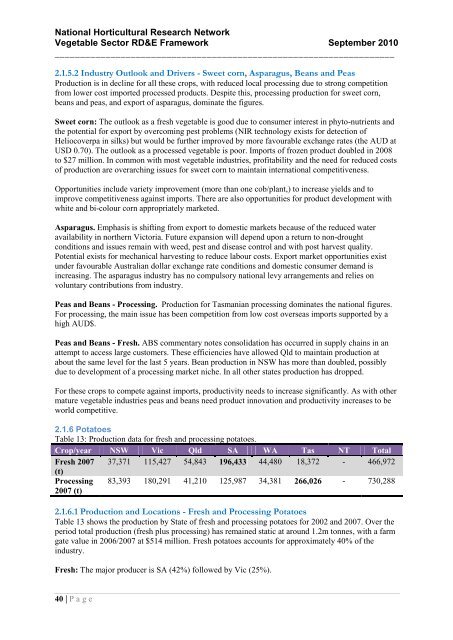

2.1.6 Potatoes<br />

Table 13: Production data for fresh and processing potatoes.<br />

Crop/year NSW Vic Qld SA WA Tas NT Total<br />

Fresh 2007 37,371 115,427 54,843 196,433 44,480 18,372 - 466,972<br />

(t)<br />

Processing<br />

2007 (t)<br />

83,393 180,291 41,210 125,987 34,381 266,026 - 730,288<br />

2.1.6.1 Production and Locations - Fresh and Processing Potatoes<br />

Table 13 shows the production by State of fresh and processing potatoes for 2002 and 2007. Over the<br />

period total production (fresh plus processing) has remained static at around 1.2m tonnes, with a farm<br />

gate value in 2006/2007 at $514 million. Fresh potatoes accounts for approximately 40% of the<br />

industry.<br />

Fresh: The major producer is SA (42%) followed by Vic (25%).<br />

40 | P a g e