Latvia

Latvia

Latvia

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Health systems in transition<br />

<strong>Latvia</strong><br />

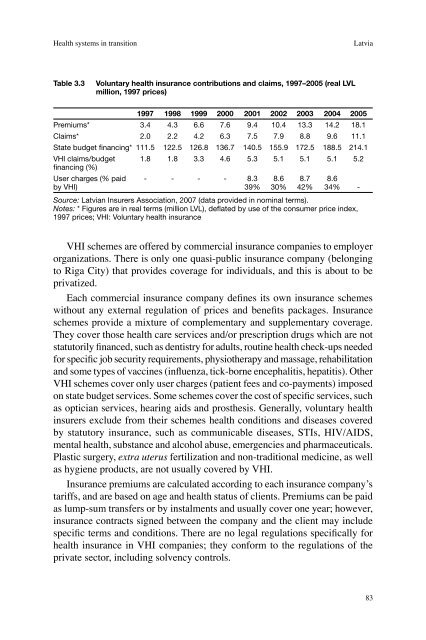

Table 3.3<br />

Voluntary health insurance contributions and claims, 1997–2005 (real LVL<br />

million, 1997 prices)<br />

1997 1998 1999 2000 2001 2002 2003 2004 2005<br />

Premiums* 3.4 4.3 6.6 7.6 9.4 10.4 13.3 14.2 18.1<br />

Claims* 2.0 2.2 4.2 6.3 7.5 7.9 8.8 9.6 11.1<br />

State budget financing* 111.5 122.5 126.8 136.7 140.5 155.9 172.5 188.5 214.1<br />

VHI claims/budget 1.8 1.8 3.3 4.6 5.3 5.1 5.1 5.1 5.2<br />

financing (%)<br />

User charges (% paid - - - - 8.3 8.6 8.7 8.6<br />

by VHI) 39% 30% 42% 34% -<br />

Source: <strong>Latvia</strong>n Insurers Association, 2007 (data provided in nominal terms).<br />

Notes: * Figures are in real terms (million LVL), deflated by use of the consumer price index,<br />

1997 prices; VHI: Voluntary health insurance<br />

VHI schemes are offered by commercial insurance companies to employer<br />

organizations. There is only one quasi-public insurance company (belonging<br />

to Riga City) that provides coverage for individuals, and this is about to be<br />

privatized.<br />

Each commercial insurance company defines its own insurance schemes<br />

without any external regulation of prices and benefits packages. Insurance<br />

schemes provide a mixture of complementary and supplementary coverage.<br />

They cover those health care services and/or prescription drugs which are not<br />

statutorily financed, such as dentistry for adults, routine health check-ups needed<br />

for specific job security requirements, physiotherapy and massage, rehabilitation<br />

and some types of vaccines (influenza, tick-borne encephalitis, hepatitis). Other<br />

VHI schemes cover only user charges (patient fees and co-payments) imposed<br />

on state budget services. Some schemes cover the cost of specific services, such<br />

as optician services, hearing aids and prosthesis. Generally, voluntary health<br />

insurers exclude from their schemes health conditions and diseases covered<br />

by statutory insurance, such as communicable diseases, STIs, HIV/AIDS,<br />

mental health, substance and alcohol abuse, emergencies and pharmaceuticals.<br />

Plastic surgery, extra uterus fertilization and non-traditional medicine, as well<br />

as hygiene products, are not usually covered by VHI.<br />

Insurance premiums are calculated according to each insurance company’s<br />

tariffs, and are based on age and health status of clients. Premiums can be paid<br />

as lump-sum transfers or by instalments and usually cover one year; however,<br />

insurance contracts signed between the company and the client may include<br />

specific terms and conditions. There are no legal regulations specifically for<br />

health insurance in VHI companies; they conform to the regulations of the<br />

private sector, including solvency controls.<br />

83