Market Economics | Interest Rate Strategy - BNP PARIBAS ...

Market Economics | Interest Rate Strategy - BNP PARIBAS ...

Market Economics | Interest Rate Strategy - BNP PARIBAS ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Inflation: High BEs Ahead of Supply<br />

• GLOBAL: Back at the top for commodities.<br />

• EUR: 4bp premium for the Bundei20.<br />

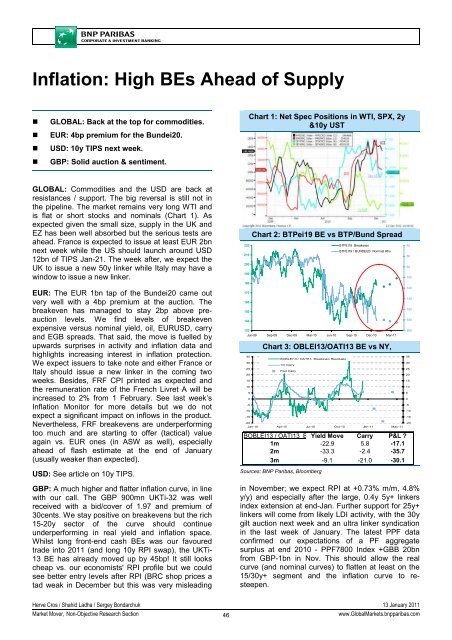

Chart 1: Net Spec Positions in WTI, SPX, 2y<br />

&10y UST<br />

• USD: 10y TIPS next week.<br />

• GBP: Solid auction & sentiment.<br />

GLOBAL: Commodities and the USD are back at<br />

resistances / support. The big reversal is still not in<br />

the pipeline. The market remains very long WTI and<br />

is flat or short stocks and nominals (Chart 1). As<br />

expected given the small size, supply in the UK and<br />

EZ has been well absorbed but the serious tests are<br />

ahead. France is expected to issue at least EUR 2bn<br />

next week while the US should launch around USD<br />

12bn of TIPS Jan-21. The week after, we expect the<br />

UK to issue a new 50y linker while Italy may have a<br />

window to issue a new linker.<br />

EUR: The EUR 1bn tap of the Bundei20 came out<br />

very well with a 4bp premium at the auction. The<br />

breakeven has managed to stay 2bp above preauction<br />

levels. We find levels of breakeven<br />

expensive versus nominal yield, oil, EURUSD, carry<br />

and EGB spreads. That said, the move is fuelled by<br />

upwards surprises in activity and inflation data and<br />

highlights increasing interest in inflation protection.<br />

We expect issuers to take note and either France or<br />

Italy should issue a new linker in the coming two<br />

weeks. Besides, FRF CPI printed as expected and<br />

the remuneration rate of the French Livret A will be<br />

increased to 2% from 1 February. See last week’s<br />

Inflation Monitor for more details but we do not<br />

expect a significant impact on inflows in the product.<br />

Nevertheless, FRF breakevens are underperforming<br />

too much and are starting to offer (tactical) value<br />

again vs. EUR ones (in ASW as well), especially<br />

ahead of flash estimate at the end of January<br />

(usually weaker than expected).<br />

USD: See article on 10y TIPS.<br />

GBP: A much higher and flatter inflation curve, in line<br />

with our call. The GBP 900mn UKTi-32 was well<br />

received with a bid/cover of 1.97 and premium of<br />

30cents. We stay positive on breakevens but the rich<br />

15-20y sector of the curve should continue<br />

underperforming in real yield and inflation space.<br />

Whilst long front-end cash BEs was our favoured<br />

trade into 2011 (and long 10y RPI swap), the UKTi-<br />

13 BE has already moved up by 45bp! It still looks<br />

cheap vs. our economists' RPI profile but we could<br />

see better entry levels after RPI (BRC shop prices a<br />

tad weak in December but this was very misleading<br />

220<br />

210<br />

200<br />

190<br />

180<br />

170<br />

160<br />

150<br />

140<br />

Chart 2: BTPei19 BE vs BTP/Bund Spread<br />

130<br />

Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11<br />

35<br />

30<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

-5<br />

-10<br />

-15<br />

-20<br />

BTPEI19 Breakeven<br />

BTPEI19 / BUNDEI20 Nominal Rhs<br />

Chart 3: OBLEI13/OATI13 BE vs NY,<br />

BOBLEI13 / OATI13 Breakeven Residuals<br />

1m Carry<br />

Fwd Carry<br />

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 May-11<br />

BOBLEI13 / OATI13 B Yield Move Carry P&L ?<br />

1m -22.9 5.8 -17.1<br />

2m -33.3 -2.4 -35.7<br />

3m -9.1 -21.0 -30.1<br />

Sources: <strong>BNP</strong> Paribas, Bloomberg<br />

in November; we expect RPI at +0.73% m/m, 4.8%<br />

y/y) and especially after the large, 0.4y 5y+ linkers<br />

index extension at end-Jan. Further support for 25y+<br />

linkers will come from likely LDI activity, with the 30y<br />

gilt auction next week and an ultra linker syndication<br />

in the last week of January. The latest PPF data<br />

confirmed our expectations of a PF aggregate<br />

surplus at end 2010 - PPF7800 Index +GBB 20bn<br />

from GBP-1bn in Nov. This should allow the real<br />

curve (and nominal curves) to flatten at least on the<br />

15/30y+ segment and the inflation curve to resteepen.<br />

40<br />

60<br />

80<br />

100<br />

120<br />

140<br />

160<br />

180<br />

200<br />

35<br />

30<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

-5<br />

-10<br />

-15<br />

-20<br />

Herve Cros / Shahid Ladha / Sergey Bondarchuk 13 January 2011<br />

<strong>Market</strong> Mover, Non-Objective Research Section<br />

46<br />

www.Global<strong>Market</strong>s.bnpparibas.com