AWB Limited - 2003 Annual Report

AWB Limited - 2003 Annual Report

AWB Limited - 2003 Annual Report

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

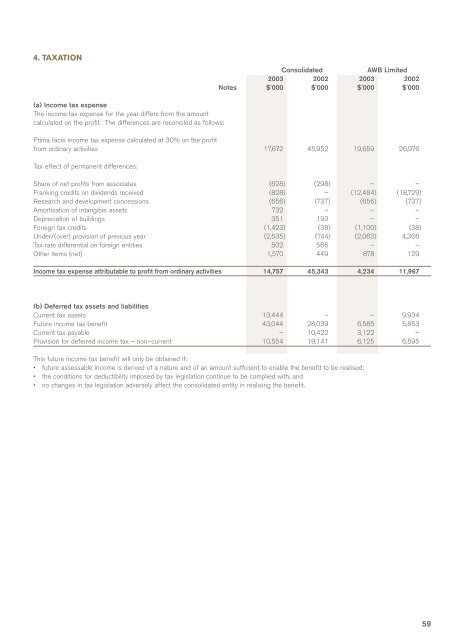

4. TAXATION<br />

Consolidated<br />

<strong>AWB</strong> <strong>Limited</strong><br />

<strong>2003</strong> 2002 <strong>2003</strong> 2002<br />

Notes $'000 $'000 $'000 $'000<br />

(a) Income tax expense<br />

The income tax expense for the year differs from the amount<br />

calculated on the profit. The differences are reconciled as follows:<br />

Prima facie income tax expense calculated at 30% on the profit<br />

from ordinary activities 17,672 45,952 19,659 26,976<br />

Tax effect of permanent differences:<br />

Share of net profits from associates (628) (298) – –<br />

Franking credits on dividends received (828) – (12,484) (18,729)<br />

Research and development concessions (656) (737) (656) (737)<br />

Amortisation of intangible assets 732 – – –<br />

Depreciation of buildings 351 193 – –<br />

Foreign tax credits (1,423) (38) (1,100) (38)<br />

Under/(over) provision of previous year (2,535) (744) (2,063) 4,366<br />

Tax rate differential on foreign entities 502 566 – –<br />

Other items (net) 1,570 449 878 129<br />

Income tax expense attributable to profit from ordinary activities 14,757 45,343 4,234 11,967<br />

(b) Deferred tax assets and liabilities<br />

Current tax assets 13,444 – – 9,934<br />

Future income tax benefit 43,044 28,039 6,585 5,853<br />

Current tax payable – 10,422 3,122 –<br />

Provision for deferred income tax – non–current 10,554 19,141 6,125 6,595<br />

This future income tax benefit will only be obtained if:<br />

• future assessable income is derived of a nature and of an amount sufficient to enable the benefit to be realised;<br />

• the conditions for deductibility imposed by tax legislation continue to be complied with; and<br />

• no changes in tax legislation adversely affect the consolidated entity in realising the benefit.<br />

59